AFM101 Lecture Notes - Lecture 6: Operating Expense, Financial Statement, Fiscal Year

Document Summary

Get access

Related Documents

Related Questions

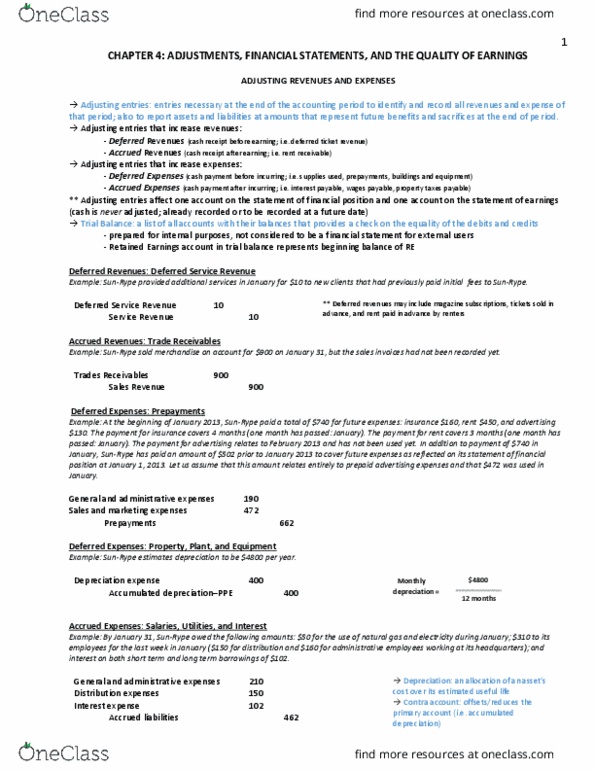

Complex Balance Sheet

Presented below is the unaudited balance sheet as of December31, 2016, prepared by Zeus Manufacturing Corporationâsbookkeeper.

| Zeus Manufacturing Corporation Balance Sheet for the Year Ended December 31, 2016 | ||||

| Assets | Liabilities and Shareholders' Equity | |||

| Cash | $225,000 | Accounts payable | $133,800 | |

| Accounts receivable (net) | 345,700 | Mortgage payable | 900,000 | |

| Inventories | 560,000 | Notes payable | 500,000 | |

| Prepaid income taxes | 40,000 | Lawsuit liability | 80,000 | |

| Investments | 57,700 | Income taxes payable | 61,200 | |

| Land | 450,000 | Deferred tax liability | 28,000 | |

| Building | 1,750,000 | Accumulated depreciation | 420,000 | |

| Machinery and equipment | 1,964,000 | Total Liabilities | $2,123,000 | |

| Goodwill | 37,000 | Common stock, $50 par; 40,000 shares issued | $2,231,000 | |

| Total Assets | $5,429,400 | Retained earnings | 1,075,400 | |

| Total Shareholders' Equity | $3,306,400 | |||

| Total Liabilities and Shareholders' Equity | $5,429,400 | |||

Your company has been engaged to perform an audit, during whichyou discover the following information:

Checks totaling $14,000 in payment of accounts payable weremailed on December 31, 2016, but were not recorded until 2017. Latein December 2016, the bank returned a customerâs $2,000 checkmarked "NSF," but no entry was made. Cash includes $100,000restricted for building purposes.

Included in accounts receivable is a $30,000 note due onDecember 31, 2019, from Zeusâs president.

During 2016, Zeus purchased 500 shares of common stock of amajor corporation that supplies Zeus with raw materials. Total costof this stock was $51,300, and fair value on December 31, 2016, was$47,000. The decline in fair value is considered temporary. Zeusplans to hold these shares indefinitely.

Treasury stock was recorded at cost when Zeus purchased 200 ofits own shares for $32 per share in May 2016. This amount isincluded in investments.

On December 31, 2016, Zeus borrowed $500,000 from a bank inexchange for a 10% note payable, maturing December 31, 2021. Equalprincipal payments are due December 31 of each year beginning in2017. This note is collateralized by a $250,000 tract of landacquired as a potential future building site, which is included inland.

The mortgage payable requires $50,000 principal payments, plusinterest, at the end of each month. Payments were made on January31 and February 28, 2017. The balance of this mortgage was due June30, 2017. On March 1, 2017, prior to issuance of the auditedfinancial statements, Zeus consummated a noncancelable agreementwith the lender to refinance this mortgage. The new terms require$100,000 annual principal payments, plus interest, on February 28of each year, beginning in 2018. The final payment is due February28, 2025.

The lawsuit liability will be paid in 2017.

Of the total deferred tax liability, $5,000 is considered acurrent liability.

The current income tax expense reported in Zeusâs 2016 incomestatement was $61,200.

The company was authorized to issue 100,000 shares of $50 parvalue common stock.

Required:

Prepare a corrected classified balance sheet as of December 31,2016.

| Zeus Manufacturing Corporation Balance Sheet December 31, 2016 | |||

| Assets | |||

| Current Assets: | |||

| Cash | $ | ||

| Accounts receivable (net) | |||

| Inventories | |||

| Total current assets | $ | ||

| Long-Term investment, at fair value | |||

| Property, Plant, and Equipment (at cost): | |||

| Land | $ | ||

| Building | $ | ||

| Machinery and equipment | |||

| Total | |||

| Less: Accumulated depreciation | |||

| Total property, plant, and equipment | |||

| Intangible Asset: | |||

| Goodwill | |||

| Other Assets: | |||

| Cash restricted for building purposes | $ | ||

| Officer's note receivable | |||

| Land held for future building site | |||

| Total Assets | $ | ||

| Liabilities | |||

| Current Liabilities: | |||

| Accounts payable | $ | ||

| Current installments of long-term debt | |||

| Lawsuit liability | |||

| Income taxes payable | |||

| Deferred tax liability | |||

| Total current liabilities | $ | ||

| Long-Term Debt: | |||

| Mortgage payable | $ | ||

| Notes payable | |||

| Deferred tax liability | |||

| Total long-term debt | |||

| Total Liabilities | $ | ||

| Shareholders' Equity | |||

| Contributed Capital: | |||

| Common stock, $50 par value | $ | ||

| Additional paid-in capital | |||

| Total paid-in capital | $ | ||

| Retained earnings | |||

| Accumulated Other Comprehensive Loss: | |||

| Unrealized decrease in value of long-term investment | |||

| Total | $ | ||

| Less: Cost of treasury stock | |||

| Total Shareholders' Equity | |||

| Total Liabilities and Shareholders' Equity | $ | ||

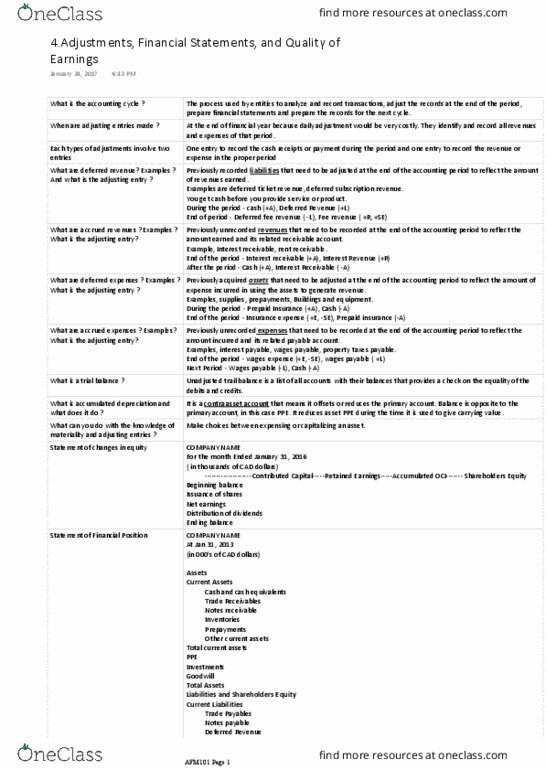

Problems: For partial credit, work must be shown in an orderlyfashion. Answers will be graded based on their ability tocommunicate the problem solvingprocess. 30 points

Required: Prepare a multiple-step income statement in good form.

Calculate retained earnings as of December 31.

Prepare a classified balance sheet ingood form.

Calculate the providedratios 20 points

Additional Information:

Assume that all taxes are at 30% unless otherwise indicated. Theincome tax expense on continuing operations and the income taxliability have not yet been recorded.

Line Item 1 refers to a loss of $70,000 on uninsured damagedfrom a meteor that crashed into a plant facility in New Mexico. Themeteor is considered BOTH UNUSUAL AND INFREQUENT. The applicabletax rate was 35%.

Line Item 2 is income from the publishing division of the firmprior to May 1, 2016. On May 1, management decided to spin-off[discontinue] the operations.

Line Item 3 is also related to the publishing division mentionedin âcâ above. Actual losses on the divisions operations after May 1totaled $50,000. Management further expected additional losses of$30,000 on operations and a loss of $220,000 on the sale of thedivisionâs assets.

Line Item 4 arose from the sale of long-term investments. Theportfolio that originally cost $250,000 was sold for $284,000.

Line Item 5 arose from discovery of equipment, costing $600,000that had been written off in 2014 as an operating expense. As ofthe beginning of the 2016 the accumulated depreciation was$100,000. The book value of the equipment was $500,000.

Line Item 6 refers to restructuring costs.

Line Item 7 refers to inventory that was on Hand on December 31,and was discovered to be obsolete during the year-end count onJanuary 15, 2017.

The investment account represents two portfolios. The firstportfolio cost $200,000 and is worth $215,000. These stocks andbonds are available currently for sale to raise cash resources. Theother investment, costing $1,000,000 and worth $1,000,000, will beheld indefinitely [long-term] by management.

Included in goodwill is an amount equal to $100,000 thatmanagement âcreatedâ after a successful advertising campaign. Theoffsetting credit was to paid-in capital in excess of par value:common.

During 2016, management decided that the usefulness of thefranchise would only last four of the remaining five years.Consequently, management increased the amortization by $100,000 or25 percent in 2016. The new estimate was used in 2016 and would becontinued for the remaining three years.

Inventory on December 31, 2016 was $200,000 after consideringthe decline from line item 7.

The state authorized 100,000 shares of 8 % preferred stock witha par value of $100 of which 8,000 shares have been issued.

The state also authorized 2,000,000 shares of common stock, witha par value of $10 par value. There are no shares in treasury.

The bonds will be refinanced when they are due in 2017.

Foreign currency translation losses were $ 3,000.

Thornhill Company | ||||

Trial Balance | ||||

as of December 31, 2016 | ||||

Account Title | Debit | Credit | ||

8 %, Preferred Stock | $ - | $ 1,000,000.00 | ||

Accounts Payable | 120,000 | |||

Accounts Receivable | 300,000 | |||

Accumulated Depreciation: building | 970,000 | |||

Accumulated Depreciation: equipment | 3,550,000 | |||

Administrative Expenses | 400,000 | |||

Bond Payable | 4,000,000 | |||

Building | 2,000,000 | |||

Cash | 100,000 | $ - | ||

Common Stock (200,000 shares outstanding) | 5,550,000 | |||

Discount on Bonds Payable | 125,000 | |||

Dividends | 300,000 | |||

Equipment | 5,000,000 | |||

Franchise | 340,000 | |||

Freight-in | 15,000 | |||

Goodwill | 785,000 | |||

Income Taxes Expenses | 88,200 | |||

Income taxes Payable | 88,200 | |||

Interest Expense | 700,000 | |||

Inventory | 170,000 | |||

Investments | 1,200,000 | |||

Land | 800,000 | |||

Long-term Notes Payable | 2,500,000 | |||

Net Sales | 5,300,000 | |||

Paid-in Capital in excess of par value: common | 300,000 | |||

Plant Facilities under Construction | 8,000,000 | |||

Prepaid Expenses | 60,000 | |||

Purchase Discounts | 65,000 | |||

Purchase Returns and Allowances | 125,000 | |||

Purchases | 2,575,000 | |||

Retained Earnings | 747,500 | |||

Selling Expenses | 650,000 | |||

Item 1 (net of taxes of $24,500) | 45,500 | |||

Item 2 (net of taxes of $6,000) | 14,000 | |||

Item 3 (net of taxes of $90,000) | 210,000 | |||

Item 4 | 34,000 | |||

Item 5 (net of taxes of $150,000) | 350,000 | |||

Item 6 | 840,000 | |||

Item 7 | 10,000 | |||

Total | $ 24,713,700 | $ 24,713,700 | ||

Financial Ratios

Current Ratio = Current Assets /Current Liabilities.

Quick Ratio = (Cash + MarketableSecurities + Receivables) / Current Liabilities.

Working Capital = Current Assets -Current Liabilities.

Total debt to total assets = Total Liabilities / TotalAssets.

Gross Profit Rate = Gross Profit/ Net Sales

Netincome as a percentage of sales = Net Income / Net Sales

Return on assets= Operating Income

[Beginning Total Assets + Ending Total Assets]/2

Assume that beginning assets were $13,720,000

Return on stockholdersâ equity=

Net Income

[BeginningTotal Stockholdersâ Equity + Ending Total StockholdersâEquity]/2

Assume that beginning stockholdersâequity was $7,947,500

Price-Earnings Ratio = MarketPrice per Commons Share

Earnings per Common Share

Assume a market price of $ 1.00

Accounts Receivable Turnover = NetSales

Assume that beginning accounts receivable were $ 300,000

Average Collection Period = 365 days/ Accounts Receivable Turnover Ratio

Inventory Turnover = Cost of Goods Sold

Average Sales Period = 365 days /Inventory Turnover Ratio

Operating Cycle = The AverageCollection Period + The Average Sales Period.

i need you to prepare a completeclassified balance sheet based on the trial balance and theadditional information. Next, I need you to prepare a multi-stepincome statement based on the same information. Then, calculate thefinancial ratios provided.

Required: Prepare a multiple-step income statement in good form.

Calculate retained earnings as of December 31.

Prepare a classified balance sheet ingood form.

Calculate the providedratios 20 points

Additional Information:

Assume that all taxes are at 30% unless otherwise indicated. Theincome tax expense on continuing operations and the income taxliability have not yet been recorded.

Line Item 1 refers to a loss of $70,000 on uninsured damagedfrom a meteor that crashed into a plant facility in New Mexico. Themeteor is considered BOTH UNUSUAL AND INFREQUENT. The applicabletax rate was 35%.

Line Item 2 is income from the publishing division of the firmprior to May 1, 2016. On May 1, management decided to spin-off[discontinue] the operations.

Line Item 3 is also related to the publishing division mentionedin âcâ above. Actual losses on the divisions operations after May 1totaled $50,000. Management further expected additional losses of$30,000 on operations and a loss of $220,000 on the sale of thedivisionâs assets.

Line Item 4 arose from the sale of long-term investments. Theportfolio that originally cost $250,000 was sold for $284,000.

Line Item 5 arose from discovery of equipment, costing $600,000that had been written off in 2014 as an operating expense. As ofthe beginning of the 2016 the accumulated depreciation was$100,000. The book value of the equipment was $500,000.

Line Item 6 refers to restructuring costs.

Line Item 7 refers to inventory that was on Hand on December 31,and was discovered to be obsolete during the year-end count onJanuary 15, 2017.

The investment account represents two portfolios. The firstportfolio cost $200,000 and is worth $215,000. These stocks andbonds are available currently for sale to raise cash resources. Theother investment, costing $1,000,000 and worth $1,000,000, will beheld indefinitely [long-term] by management.

Included in goodwill is an amount equal to $100,000 thatmanagement âcreatedâ after a successful advertising campaign. Theoffsetting credit was to paid-in capital in excess of par value:common.

During 2016, management decided that the usefulness of thefranchise would only last four of the remaining five years.Consequently, management increased the amortization by $100,000 or25 percent in 2016. The new estimate was used in 2016 and would becontinued for the remaining three years.

Inventory on December 31, 2016 was $200,000 after consideringthe decline from line item 7.

The state authorized 100,000 shares of 8 % preferred stock witha par value of $100 of which 8,000 shares have been issued.

The state also authorized 2,000,000 shares of common stock, witha par value of $10 par value. There are no shares in treasury.

The bonds will be refinanced when they are due in 2017.

Foreign currency translation losses were $ 3,000.

Thornhill Company | ||||

Trial Balance | ||||

as of December 31, 2016 | ||||

Account Title | Debit | Credit | ||

8 %, Preferred Stock | $ - | $ 1,000,000.00 | ||

Accounts Payable | 120,000 | |||

Accounts Receivable | 300,000 | |||

Accumulated Depreciation: building | 970,000 | |||

Accumulated Depreciation: equipment | 3,550,000 | |||

Administrative Expenses | 400,000 | |||

Bond Payable | 4,000,000 | |||

Building | 2,000,000 | |||

Cash | 100,000 | $ - | ||

Common Stock (200,000 shares outstanding) | 5,550,000 | |||

Discount on Bonds Payable | 125,000 | |||

Dividends | 300,000 | |||

Equipment | 5,000,000 | |||

Franchise | 340,000 | |||

Freight-in | 15,000 | |||

Goodwill | 785,000 | |||

Income Taxes Expenses | 88,200 | |||

Income taxes Payable | 88,200 | |||

Interest Expense | 700,000 | |||

Inventory | 170,000 | |||

Investments | 1,200,000 | |||

Land | 800,000 | |||

Long-term Notes Payable | 2,500,000 | |||

Net Sales | 5,300,000 | |||

Paid-in Capital in excess of par value: common | 300,000 | |||

Plant Facilities under Construction | 8,000,000 | |||

Prepaid Expenses | 60,000 | |||

Purchase Discounts | 65,000 | |||

Purchase Returns and Allowances | 125,000 | |||

Purchases | 2,575,000 | |||

Retained Earnings | 747,500 | |||

Selling Expenses | 650,000 | |||

Item 1 (net of taxes of $24,500) | 45,500 | |||

Item 2 (net of taxes of $6,000) | 14,000 | |||

Item 3 (net of taxes of $90,000) | 210,000 | |||

Item 4 | 34,000 | |||

Item 5 (net of taxes of $150,000) | 350,000 | |||

Item 6 | 840,000 | |||

Item 7 | 10,000 | |||

Total | $ 24,713,700 | $ 24,713,700 | ||

Financial Ratios

Current Ratio = Current Assets /Current Liabilities.

Quick Ratio = (Cash + MarketableSecurities + Receivables) / Current Liabilities.

Working Capital = Current Assets -Current Liabilities.

Total debt to total assets = Total Liabilities / TotalAssets.

Gross Profit Rate = Gross Profit/ Net Sales

Netincome as a percentage of sales = Net Income / Net Sales

Return on assets= Operating Income

[Beginning Total Assets + Ending Total Assets]/2

Assume that beginning assets were $13,720,000

Return on stockholdersâ equity=

Net Income

[BeginningTotal Stockholdersâ Equity + Ending Total StockholdersâEquity]/2

Assume that beginning stockholdersâequity was $7,947,500

Price-Earnings Ratio = MarketPrice per Commons Share

Earnings per Common Share

Assume a market price of $ 1.00

Accounts Receivable Turnover = NetSales

Assume that beginning accounts receivable were $ 300,000

Average Collection Period = 365 days/ Accounts Receivable Turnover Ratio

Inventory Turnover = Cost of Goods Sold

Average Sales Period = 365 days /Inventory Turnover Ratio

Operating Cycle = The AverageCollection Period + The Average Sales Period.

The question Requires me to do thebalance sheet and calculate the ratios from the trial balance andthe additional informations. use the same information that is thetrial balance and the additional information to solve forMulti-step income statement.