AFM101 Lecture Notes - Lecture 7: Deferred Income, Accrual, Deferral

15 Oct 2015

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

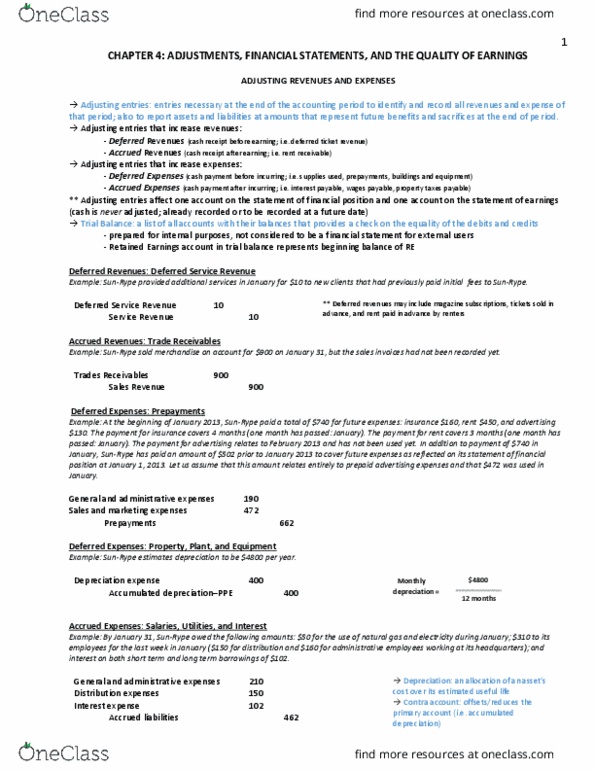

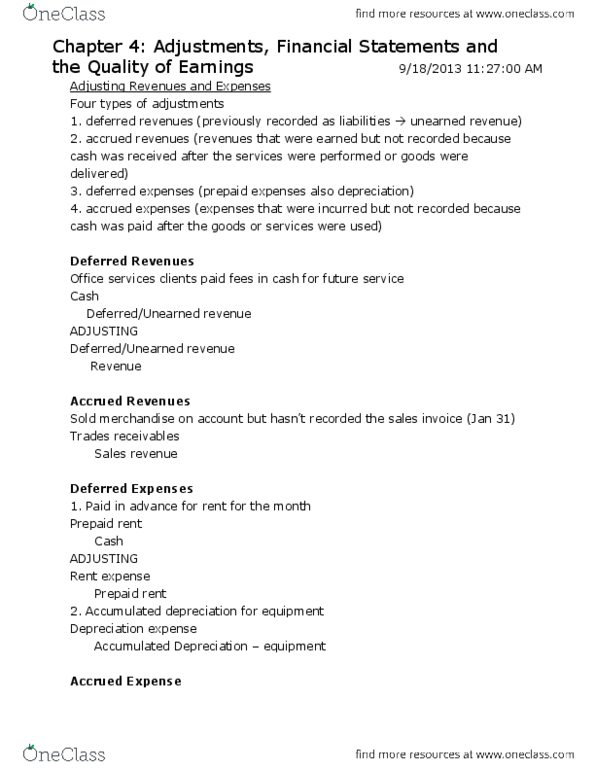

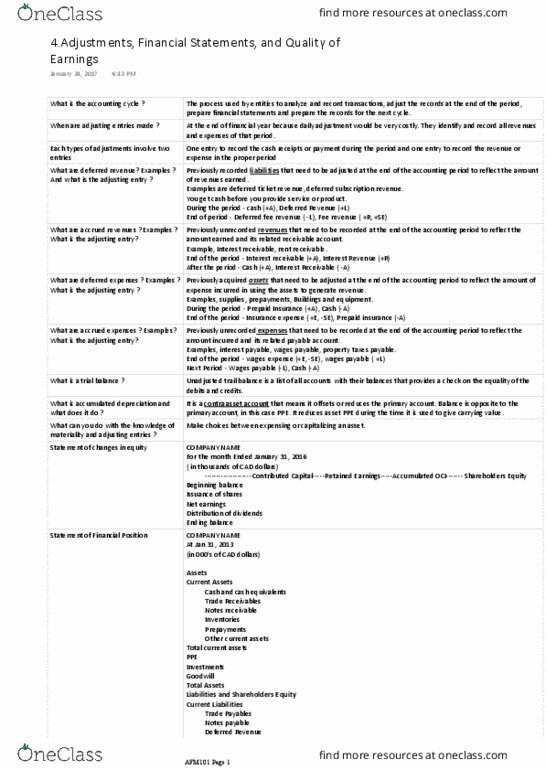

Deferred revenue: cash is received before the company performs (earns revenues) Accrued revenue: cash is received after the company performs (earns revenue) Accrued expense: cash is paid after the company incurs an expense. Deferred expense: cash is paid before the company incurs an expense. Pp&e represents deferred expenses that will be consumed over years. Under cost principle , pp&e is recorded at historical cost on balance sheet. Pp&e decreases, as it is consumed over time to generate revenue. Pp&e depreciates over time as it is used. An allocation of asset"s historical cost over its useful life. Depreciation amount is not subtracted directly from the asset account. Depreciation is accumulated in a new account called accumulated depreciation account. Book value of asset = historical cost - accumulated depreciation. Contra account- an account that is an offset to or reduction of, the primary account. Contra means opposite -> has the opposite balance account. Pp&e is an asset account -> debit balance account.