ADM 2341 Chapter Notes - Chapter 8: Direct Labor Cost, Variable Cost, Total Absorption Costing

27 Jan 2016

School

Department

Course

Professor

Document Summary

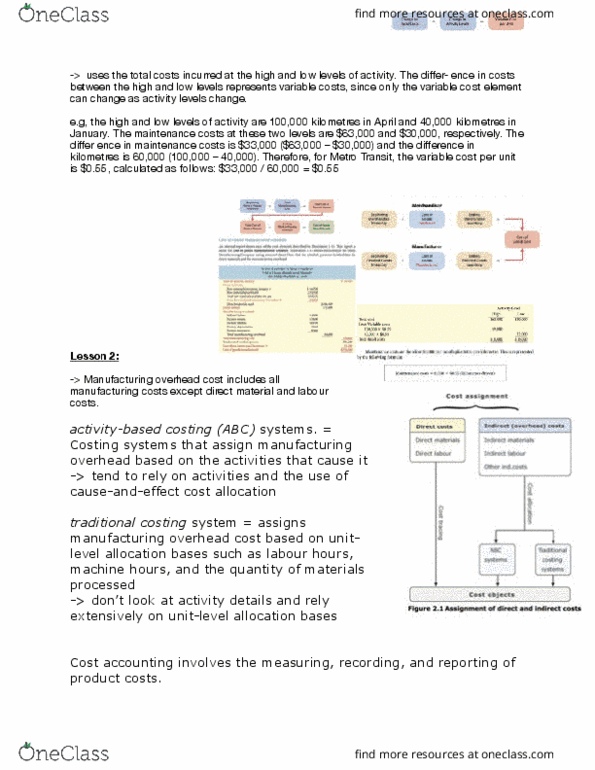

Absorption costing (full cost method) treats all costs of production as product costs, regardless of whether they are variable or fixed. Not suited for cvp computation since no distinction between variable and fixed costs. Cost of a unit of product: direct materials, direct labour, and both variable and fixed. Variable/fixed selling & admin expenses treated as period & deducted from revenue as overhead. incurred. *product cost: variable direct material cost + variable direct labor cost + direct variable mfg overhead + fixed overhead/number units sold. Variable costing (direct/marginal costing) treats only those costs of production that vary with output as product costs. Close to contribution approach income statement and supports cvp analysis because. Cost of a unit of product consists of direct materials, direct labour, and variable. Fixed manufacturing overhead, and both variable and fixed selling and administrative of its emphasis on separating variable and fixed costs. overhead. expenses are treated as period costs and deducted from revenue as incurred.