ADM 2341 Lecture Notes - Lecture 8: Decision-Making, Cash Flow, Lean Manufacturing

9 May 2016

School

Department

Course

Professor

Document Summary

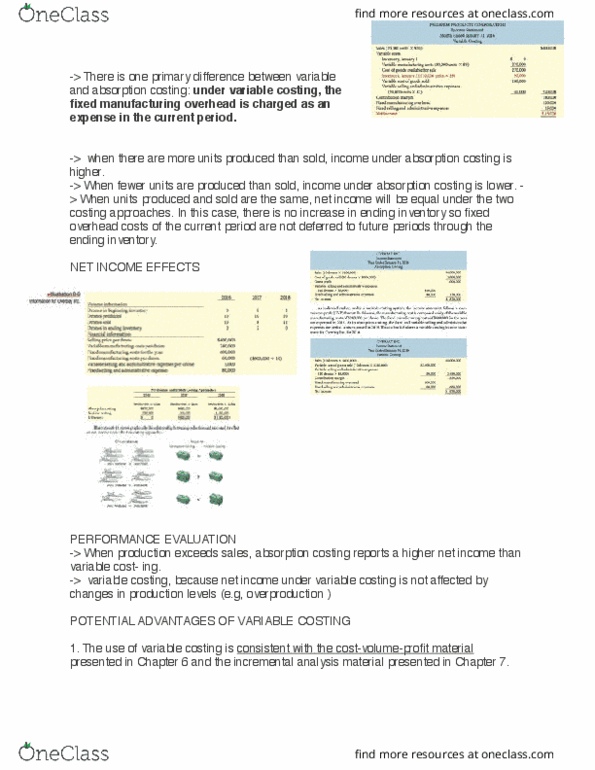

Direct materials, direct labour, manufacturing overhead (product cost) Net operating income of absorption is higher than variable (1st year) Net operating income of absorption is lower than variable (2nd year) Relation between product and sales: production > sales, production < sales, production = sales. Effect on inventory: inventory increases, inventory decreases, no change. Relation between variable and absorption income: absorption > variable, absorption < variable, absorption = variable. Variable costing income only affected by changes in unit sales. Not affected by the number of units produced. When sales go up, go up net operating income goes up and vice versa. Absorption costing income is influenced by changes in unit sales and units of production. Net operating income increased simply by producing more units even if those units are not sold. Opponents of absorption costing argue that shifting b/w fixed manufacturing overhead costs b/w periods can lead to faulty decisions.