BUS 251 Chapter Notes - Chapter 3: Retained Earnings, Accounting Information System, T29 Heavy Tank

17 Aug 2012

School

Department

Course

Professor

Document Summary

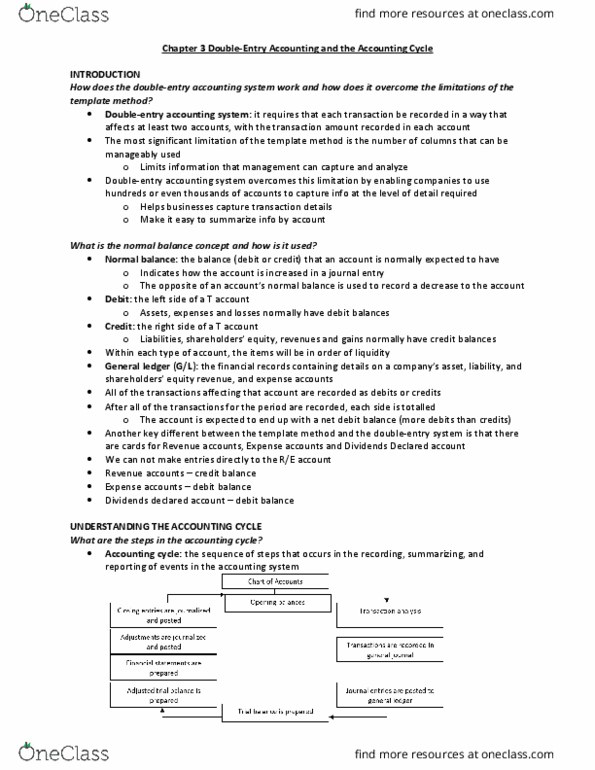

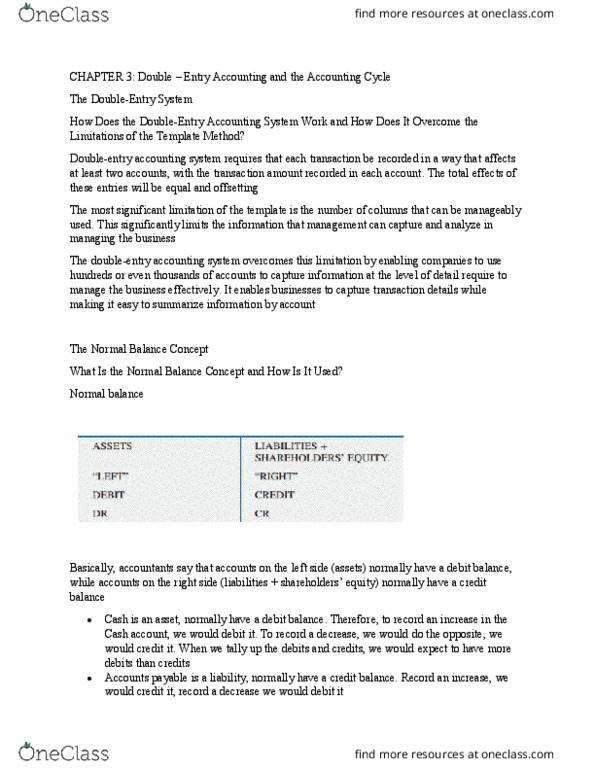

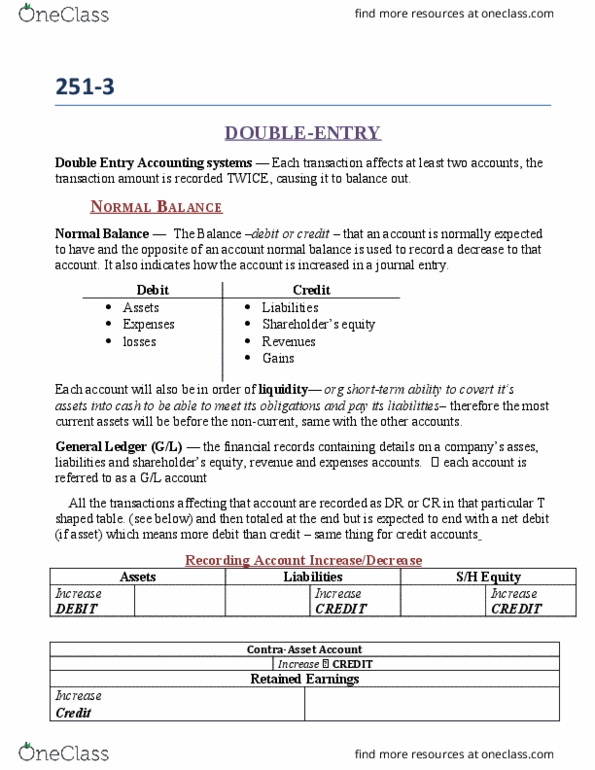

We need to understand how to store and analyze accounting data because they shows the financial statement of the company. Synoptic journal: recording of simple transactions by columns on spreadsheet to reflect the basic accounting equation. Double-entry accounting system: using debits and credits to record the effects of transactions in accounts rather than columns. Assets accounts have debit balances, increase in asset accounts are recorded as debits, and decreases in assets are recorded as credits. Liabilities and shareholder"s equity have credit balances, increase in these accounts is recorded as credits, and decrease is recorded as debits. Example: retained earnings: temporary accounts are used to keep track of sub accounts of permanent accounts. Revenues increases retained earnings (se) = debit. Accounting cycle: the system which transactions are measured, recorded and summarized and communicate to users through financial statements. The opening balances: amounts are carried forward from the previous accumulated accounting accounts, temporary accounts have zero balance for opening balances.