BUS 251 Lecture Notes - Lecture 3: General Ledger, Retained Earnings, Net Income

25 Aug 2016

School

Department

Course

Professor

Document Summary

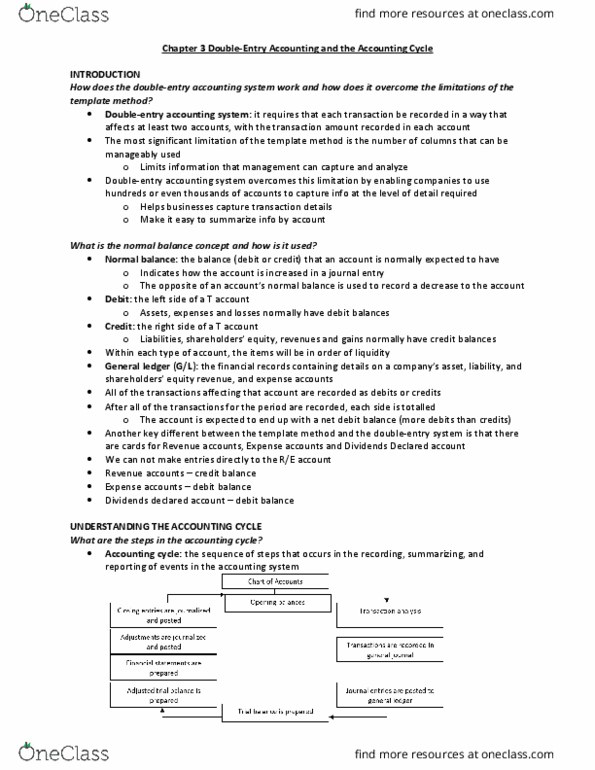

Double entry accounting systems each transaction affects at least two accounts, the transaction amount is recorded twice, causing it to balance out. Normal balance the balance debit or credit that an account is normally expected to have and the opposite of an account normal balance is used to record a decrease to that account. It also indicates how the account is increased in a journal entry. General ledger (g/l) the financial records containing details on a company"s asses, liabilities and shareholder"s equity, revenue and expenses accounts. Each account is referred to as a g/l account. Revenues increase r/e because they increase net income credit. Dividend declared decrease r/e because they distribute r/e debit. Accounting cycle a sequence of steps that occurs in the recording, summarizing and reporting of events in the accounting system: chart of accounts. A list of all the company"s accounts is coa. Establishing the coa is the starting point in an initial account cycle.