BUS 251 Lecture Notes - Lecture 3: Accounts Payable, Template Method Pattern, Accrual

15 Apr 2021

School

Department

Course

Professor

Document Summary

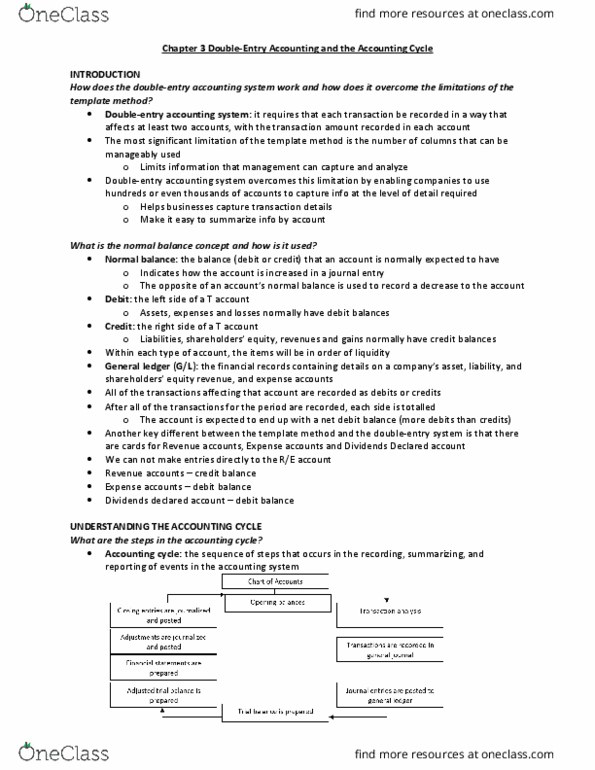

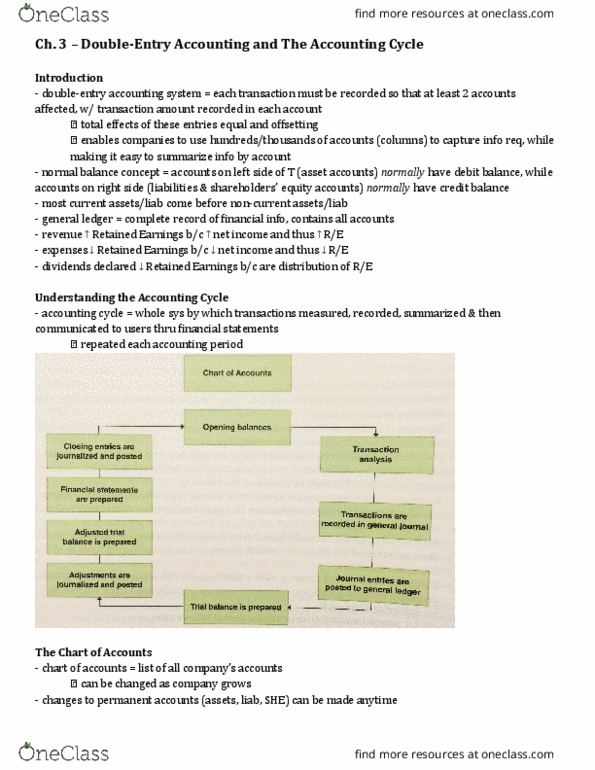

Chapter 3: double entry accounting and the accounting cycle. How does the double-entry accounting system work and how does it overcome the. Double-entry accounting system requires that each transaction be recorded in a way that affects at least two accounts, with the transaction amount recorded in each account. The total effects of these entries will be equal and offsetting. The most significant limitation of the template is the number of columns that can be manageably used. This significantly limits the information that management can capture and analyze in managing the business. The double-entry accounting system overcomes this limitation by enabling companies to use hundreds or even thousands of accounts to capture information at the level of detail require to manage the business effectively. It enables businesses to capture transaction details while making it easy to summarize information by account. To record a decrease, we would do the opposite, we would credit it.