ECN 104 Chapter Notes - Chapter 13: Average Cost, Monopolistic Competition, Monopoly Price

102 views6 pages

14 Nov 2016

School

Department

Course

Professor

Document Summary

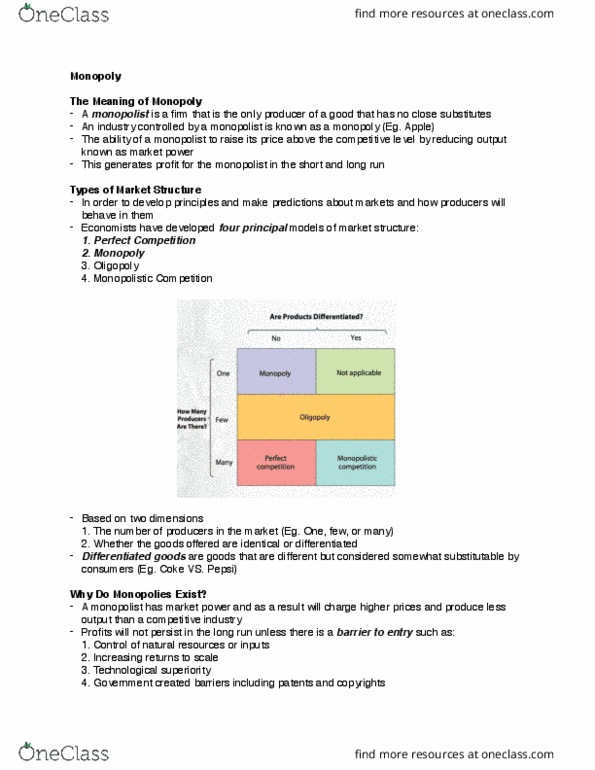

In order to develop principles and make predictions about markets and how producers will behave in them, economists have developed 4 principal models of market structure: perfect competition, monopoly, oligopoly, monopolistic competition. A monopolist is a firm that is the only producer of a good that has no close substitutes. An industry controlled by a monopolist is known as a monopoly. The ability of a monopolist to raise its price above the competitive level by reducing output is known as market power. This generates profit for the monopolist in the short run and the long run. A monopolist has market power, and as a result will charge higher prices and produce less output than a competitive industry. Profits will not persist in the long run unless there is a barrier of entry. A natural monopoly exists when increasing returns to scale provide a large cost adva(cid:374)tage to a si(cid:374)gle fir(cid:373) that produces all of a(cid:374) i(cid:374)dustry"s output.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers