Watch this video on Porter's Five Forces:

Link: https://hbr.org/video/3590615226001/ the-explainer-porters-five-forces

a. Discuss each of Porter's Five Forces within the context of the four types of markets discussed in class: perfect competition, monopoly, monopolistic competition, and oligopoly.

b. In the interview of Michael Porter assigned from last time, he discusses the concept of "disruptive technologies". Within the context of market competition and industry structure, what should managers be aware of in industries that are experiencing a disruptive technology?

Five Forces Summary:

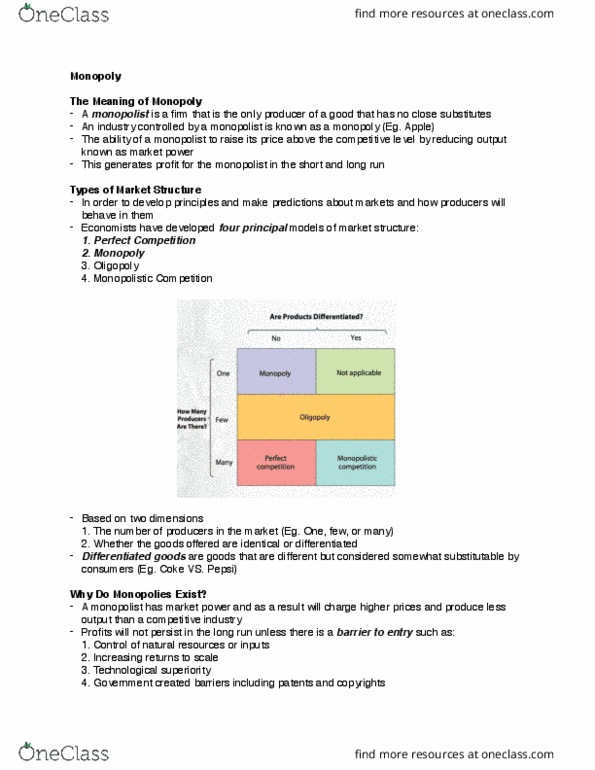

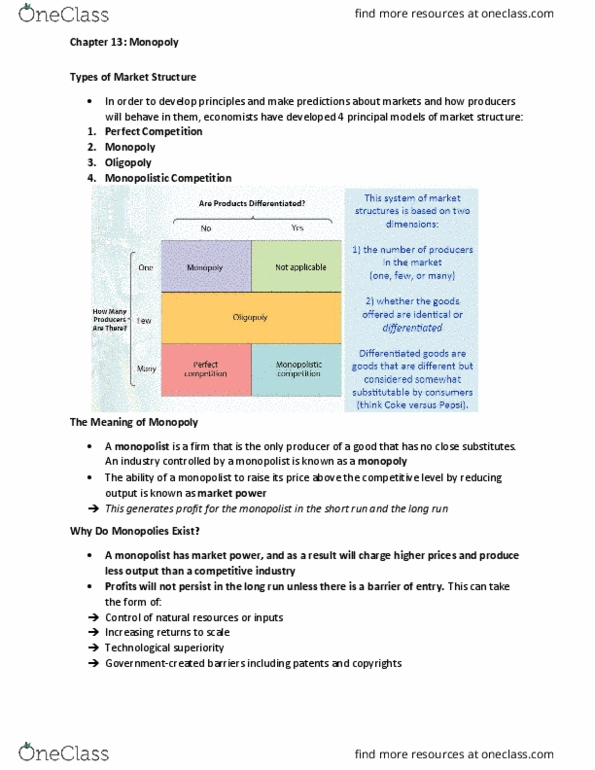

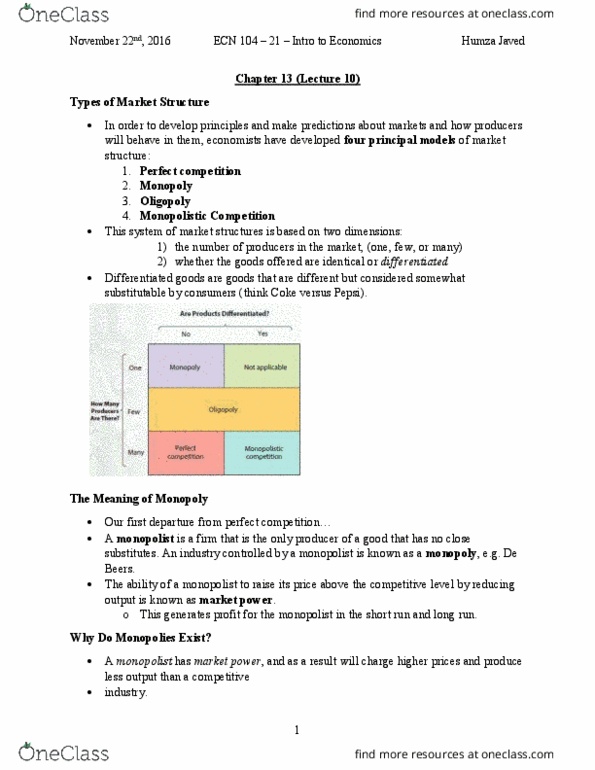

What are 'Porter's 5 Forces'

Porter's Five Forces model, named after Michael E. Porter, identifies and analyzes five competitive forces that shape every industry, and helps determine an industry's weaknesses and strengths. These forces are:

1. Competition in the industry;

2. Potential of new entrants into the industry;

3. Power of suppliers;

4. Power of customers;

5. Threat of substitute products.

Frequently used to identify an industry's structure to determine corporate strategy, Porter's model can be applied to any segment of the economy to search for profitability and attractiveness.

Breaking down 'Porter's 5 Forces'

Porter's Five Forces is a model of analysis that helps to explain why different industries are able to sustain different levels of profitability. This model was originally published in Porter's book, "Competitive Strategy: Techniques for Analyzing Industries and Competitors" in 1980. The model is widely used, worldwide, to analyze the industry structure of a company as well as its corporate strategy. Porter identified five undeniable forces that play a part in shaping every market and industry in the world. The forces are frequently used to measure competition intensity, attractiveness, and profitability of an industry or market.

Competition in the industry

The importance of this force is the number of competitors and their ability to threaten a company. The larger the number of competitors, along with the number of equivalent products and services they offer, dictates the power of a company. Suppliers and buyers seek out a company's competition if they are unable to receive a suitable deal.

Potential of new entrants into an industry

A company's power is also affected by the force of new entrants into its market. The less money and time it costs for a competitor to enter a company's market and be an effective competitor, the more a company's position may be significantly weakened.

Power of suppliers

This force addresses how easily suppliers can drive up the price of goods and services. It is affected by the number of suppliers of key aspects of a good or service, how unique these aspects are, and how much it would cost a company to switch from one supplier to another. The fewer number of suppliers and the more a company depends upon a supplier, the more power a supplier holds.

Power of customers

This specifically deals with the ability customers have to drive prices down. It is affected by how many buyers, or customers, a company has, how significant each customer is, and how much it would cost a customer to switch from one company to another. The smaller and more powerful a client base, the more power it holds.

Threat of substitutes

Competitor substitutions that can be used in place of a company's products or services pose a threat. For example, if customers rely on a company to provide a tool or service that can be substituted with another tool or service or by performing the task manually, and this substitution is fairly easy and of low cost, a company's power can be weakened.