ELECTRN 6 Lecture Notes - Lecture 8: Matching Principle, Uptodate, Deferral

Document Summary

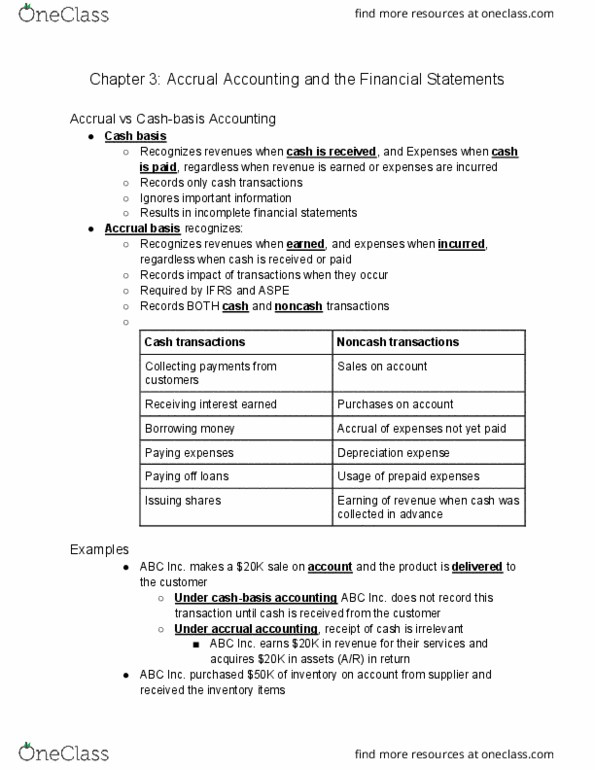

Task 6: explain accrual accounting, the revenue recognition principle, matching concepts. Issuing shares: noncash transactions, sales on account, purchases of inventory on account, accrual of expenses incurred but not yet paid, depreciation expense, usage of prepaid rent, insurance, supplies, earning of revenue when cash was collected in advance. It is probable that the economic benefits associated with the transaction will flow to the entity: the costs incurred or to be incurred can be measured reliably. Matching concepts: used to explain relationship between expenses and revenues, two steps, identify decreases in assets or increases in liabilities that result in a reduction in equity (excluding transactions with owners). These are expenses: measure these expenses and subtract expenses from revenue to compute profit or loss, expenses have to be paid, not only incurred (otherwise it"s a liability) Liabilities and shareholders" equity: shows whether total debits equal total credits.