ACC 151 Chapter Notes - Chapter 3: Deferral, Income Statement, Fiscal Year

101 views4 pages

26 Sep 2016

School

Department

Course

Professor

Document Summary

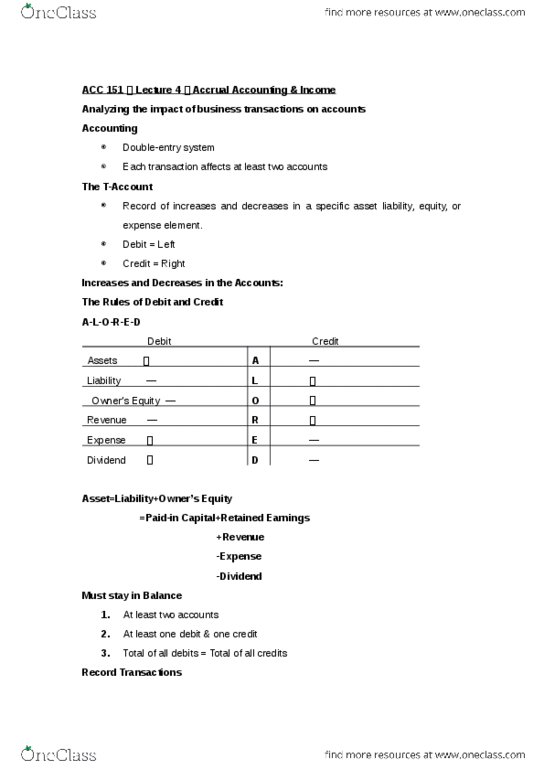

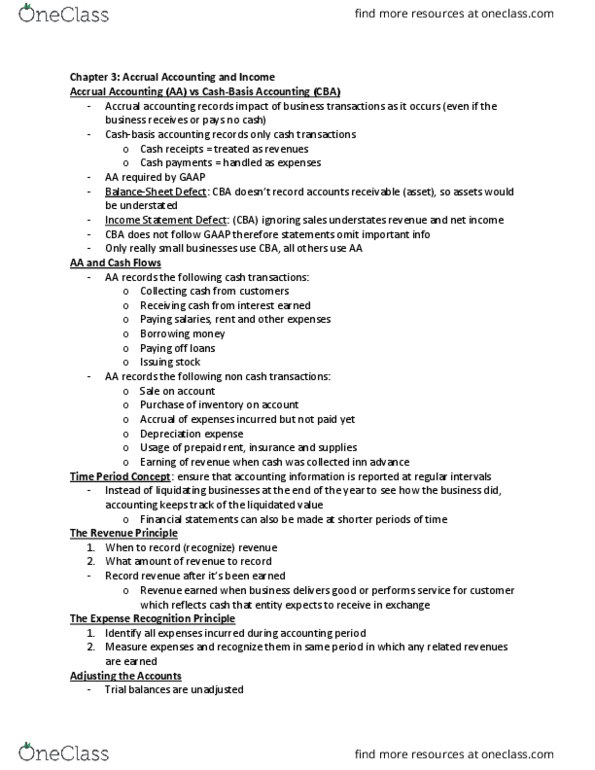

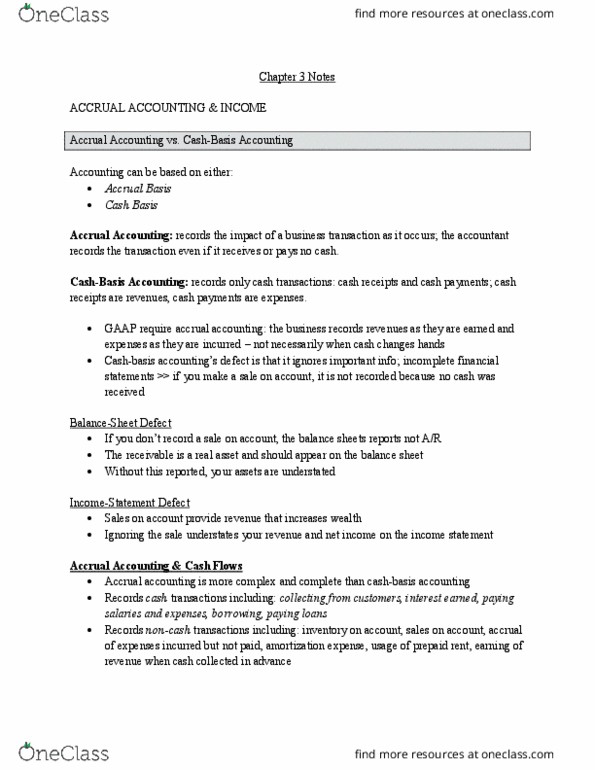

Accrual accounting: records the impact of business transactions as it occurs. Even if the business receives or pays no cash. Cash-basis accounting: records only cash transactions- cash receipts and cash payments. Do not follow gaap- financial statements omit important information. Making sale, not collecting cash, increases your wealth. Balance-sheet defect: if we fail to record a sale on account, balance sheet reports no account receivable. Receivable represents a claim to receive cash in the future, which is a real asset, and so it should appear on balance sheet. Income statement defect: a sale on account provides revenue that increases the company"s wealth. Ignoring the sale understates revenue and net income on the income statement. Accrual of expenses incurred but not yet paid. Usage of prepaid rent, insurance and supplies. Earning of revenue when cash was collected in advance. Liquidation: to shut down, sell the assets, pay for liabilities, and return any leftover cash to the owners.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers