ACTG 1P91 Lecture Notes - Lecture 2: Retained Earnings, Current Liability, Deferral

17 Oct 2018

School

Department

Course

Professor

ACTG 1P91 verified notes

2/26View all

Document Summary

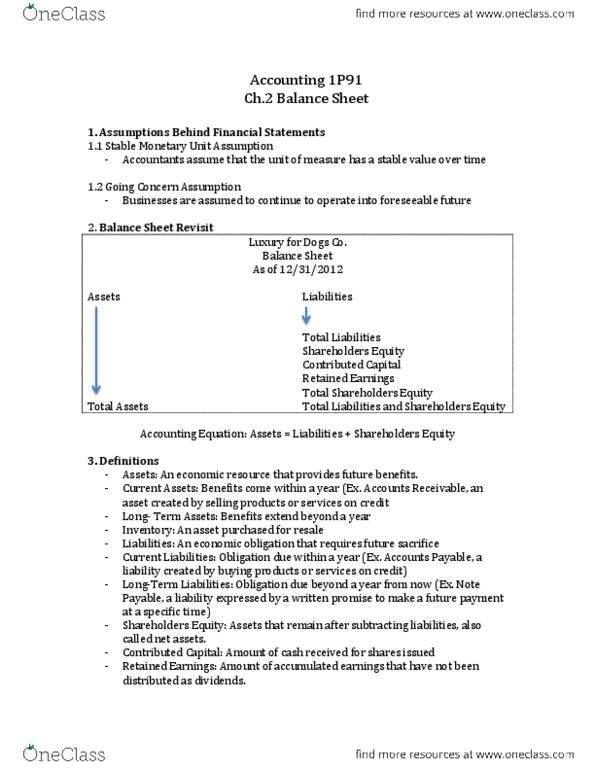

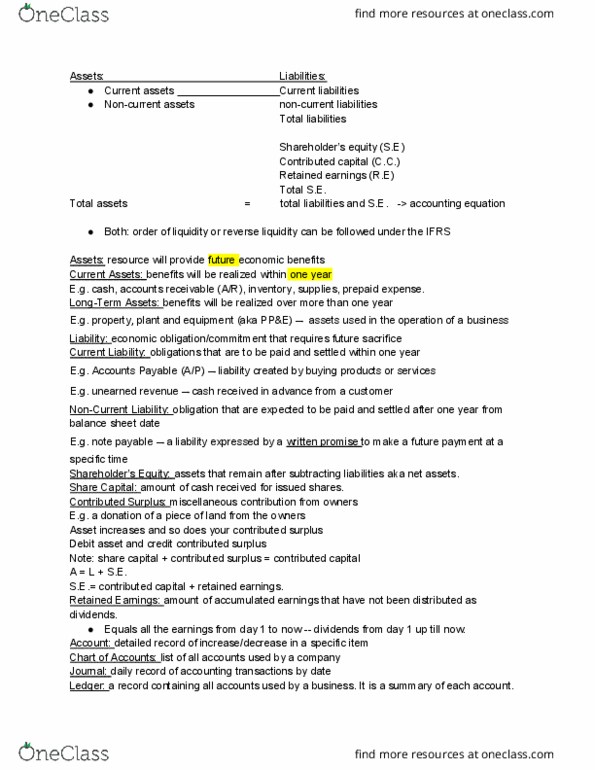

Both: order of liquidity or reverse liquidity can be followed under the ifrs. Current assets: benefits will be realized within one year. E. g. cash, accounts receivable (a/r), inventory, supplies, prepaid expense. Long-term assets: benefits will be realized over more than one year. E. g. property, plant and equipment (aka pp&e) assets used in the operation of a business. Current liability: obligations that are to be paid and settled within one year. Accounts payable (a/p) liability created by buying products or services. E. g. unearned revenue cash received in advance from a customer. Non-current liability: obligation that are expected to be paid and settled after one year from balance sheet date. E. g. note payable a liability expressed by a written promise to make a future payment at a specific time. Shareholder"s equity: assets that remain after subtracting liabilities aka net assets. Share capital: amount of cash received for issued shares. E. g. a donation of a piece of land from the owners.