ECON 322 Study Guide - Final Guide: Corporate Bond, Random Walk Hypothesis, Bond Duration

10 May 2016

School

Department

Course

Professor

Document Summary

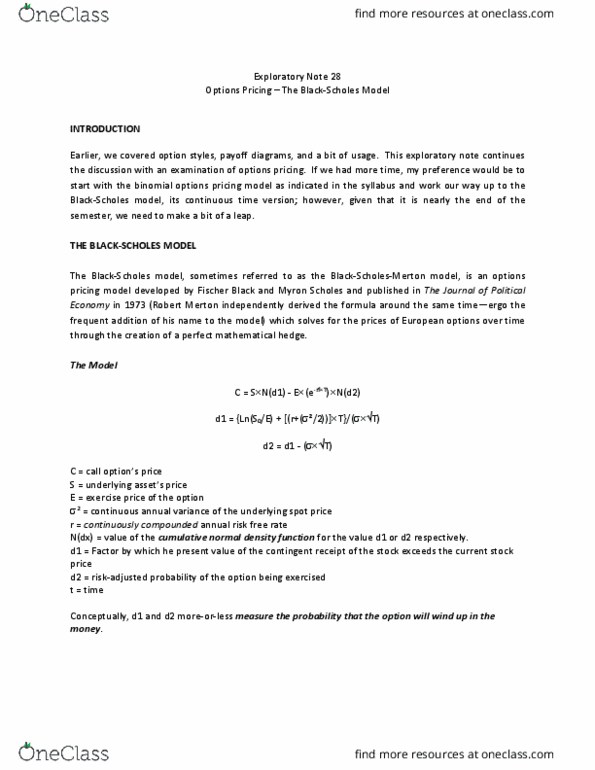

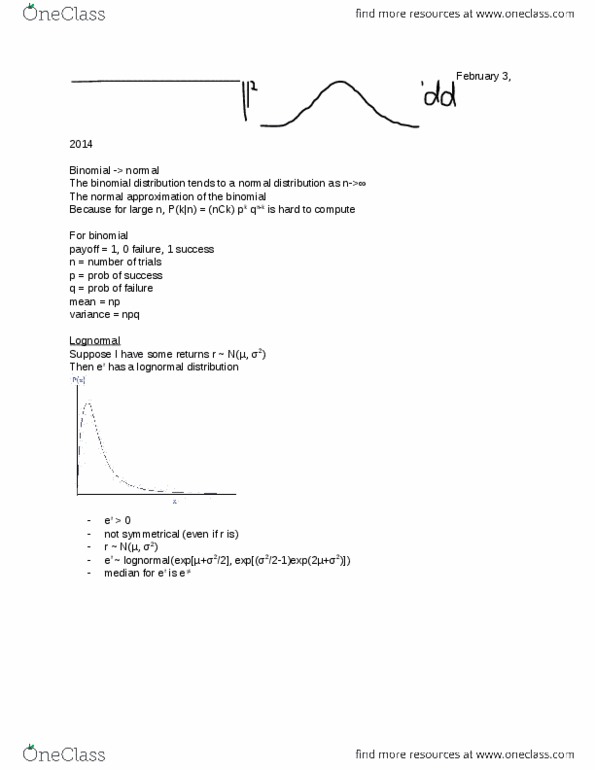

1. you should know how to derive the binomial option pricing model as in. Eg for 3 dates, t = 0, 1, 2. Understand how the binomial model approximates the black-scholes model formula as the number of trading times increases. (i am interested in intuition rather than a proof. ) The binomial option pricing model for 3 dates is easy. Remember that proof and remember speci cally that the t=2 version is. The reason that the binomial option pricing theory approximates the black scholes. Option pricing theory is the way time breaks down as t in nite. In the binomial option theory, one of two movements can occur once a period. Basically, it is a very discrete time based idea. As we have t in nite, the discrete time becomes a lot closer to continuous time. This results in both u and d being distributed normally, as opposed to previously where they were distributed binomially.