SMG FE 449 Chapter Notes - Chapter 21: Valuation Of Options, Put Option, Call Option

18 Feb 2017

School

Department

Course

Professor

Document Summary

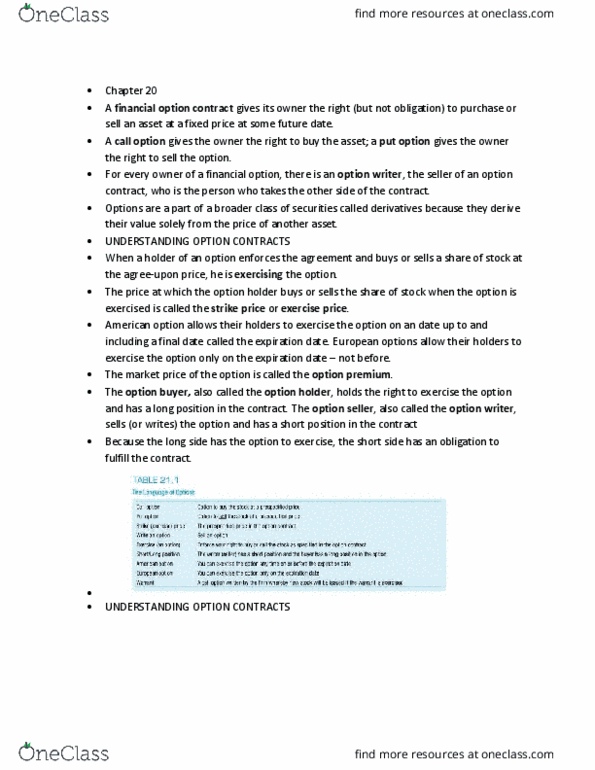

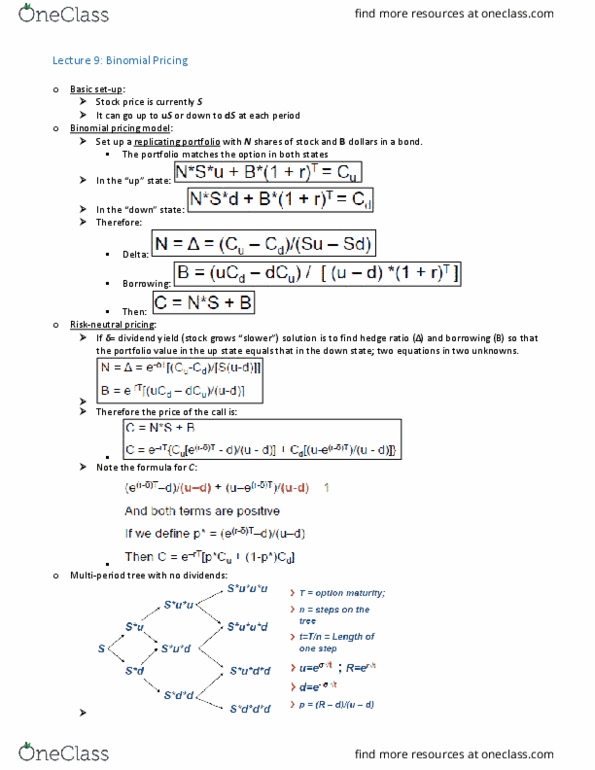

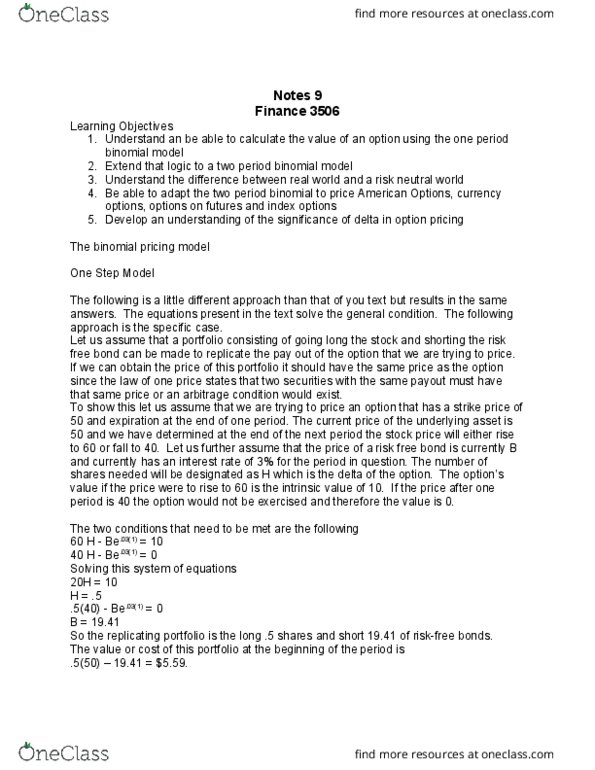

Binomial option pricing model - the model prices options by making the simplifying assumption that at the end of the next period, the stock price has only two possible values. A two-state single-period model: we will value the option by first constructing a replicating portfolio, a portfolio of other securities that has exactly the same value in one period as the option. Today, this kind of replication strategy is called a dynamic trading strategy. The black-scholes option pricing model: black-scholes option pricing model can be derived from the binomial option pricing. Model by making the length of each period, and the movement of the stock price per period, shrink to zero and letting the number of periods grow infinitely large. P = pv(k )[1 - n(d2)] - s[1 - n(d1)] Implied volatility: of the five required inputs in the black-scholes formula, four are directly observable: s, The replicating portfolio: black-scholes replicating portfolio of a call option.