BLAW20001 : Corporate Law Notes – Related Party Transactions

30 Jul 2015

School

Department

Course

Professor

Document Summary

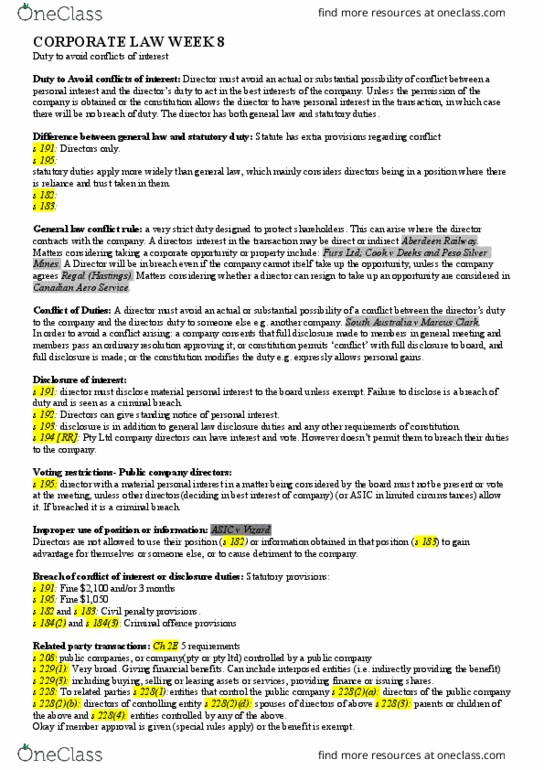

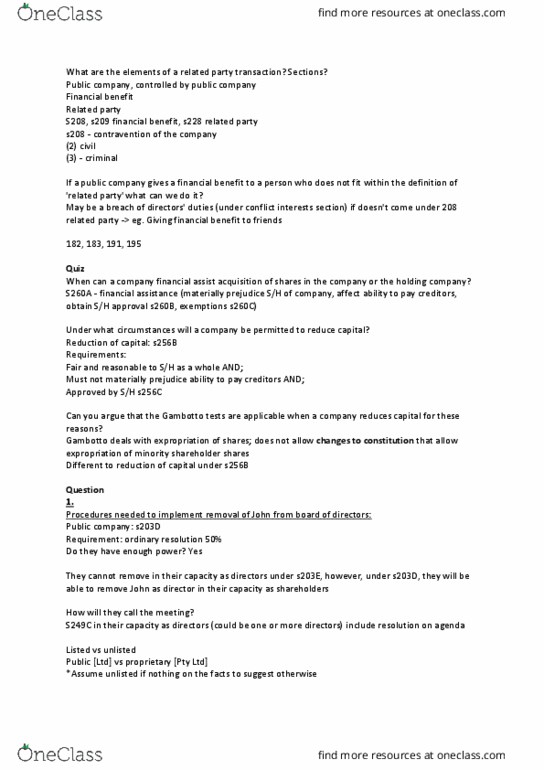

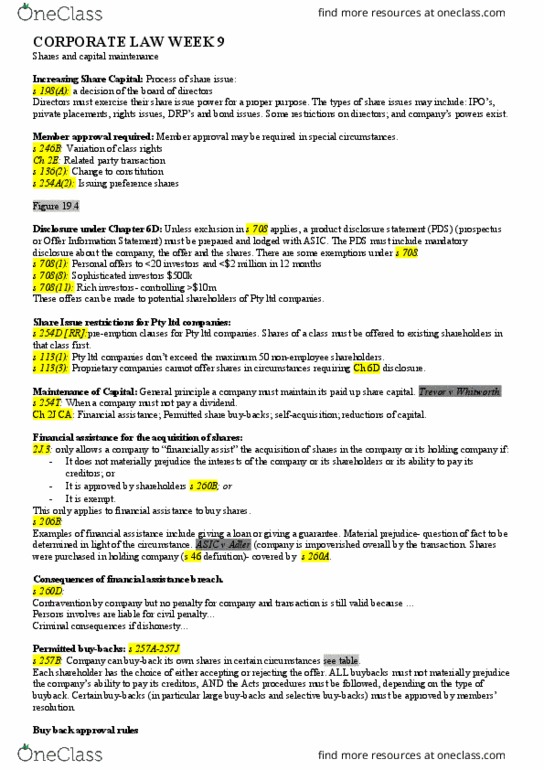

S 228 related parties: (1) controlling entities (2) directors and their spouses (3) relatives of directors and spouses (4) entities controlled by other related parties (ie. companies controlled by directors) (5) related parties in previous 6 months (6) entities that have reasonable grounds to believe they will be a related party in the future (7) entities acting in concert with related parties on the understanding that the related party will receive a financial benefit indirectly through the entity. S 229(3) : examples of giving a financial benefit to a related party: a. giving or providing the related party finance or property: buying an asset from or selling an asset to the related party; c. d. e. f. leasing an asset from or to the related party; supplying services to or receiving services from the related party; issuing securities or granting an option to the related party (shares); taking up or releasing an obligation of the related party.