BLAW20001 Lecture Notes - Lecture 9: Extraordinary Resolution, Share Capital, Oppression Remedy

19 Jun 2018

School

Department

Course

Professor

CORPORATE LAW WEEK 9

Shares and capital maintenance

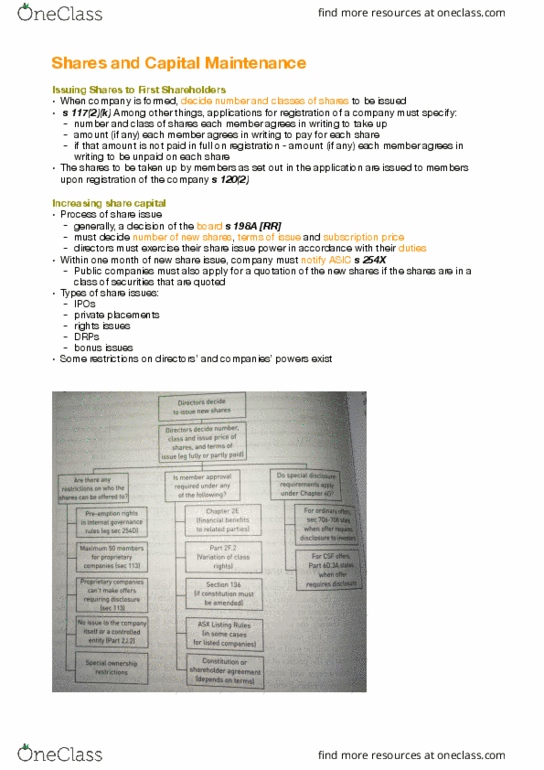

Increasing Share Capital: Process of share issue:

s 198(A): a decision of the board of directors

Directors must exercise their share issue power for a proper purpose. The types of share issues may include: IPO’s,

private placements, rights issues, DRP’s and bond issues. Some restrictions on directors; and company’s powers exist.

Member approval required: Member approval may be required in special circumstances.

s 246B: Variation of class rights

Ch 2E: Related party transaction

s 136(2): Change to constitution

s 254A(2): Issuing preference shares

Figure 19.4

Disclosure under Chapter 6D: Unless exclusion in s 708 applies, a product disclosure statement (PDS) (prospectus

or Offer Information Statement) must be prepared and lodged with ASIC. The PDS must include mandatory

disclosure about the company, the offer and the shares. There are some exemptions under s 708.

s 708(1): Personal offers to <20 investors and <$2 million in 12 months

s 708(8): Sophisticated investors $500k

s 708(11): Rich investors- controlling >$10m

These offers can be made to potential shareholders of Pty ltd companies.

Share Issue restrictions for Pty ltd companies:

s 254D [RR]:pre-emption clauses for Pty ltd companies. Shares of a class must be offered to existing shareholders in

that class first.

s 113(1): Pty ltd companies don’t exceed the maximum 50 non-employee shareholders.

s 113(3): Proprietary companies cannot offer shares in circumstances requiring Ch 6D disclosure.

Maintenance of Capital: General principle a company must maintain its paid up share capital. Trevor v Whitworth

s 254T: When a company must not pay a dividend.

Ch 2J CA: Financial assistance; Permitted share buy-backs; self-acquisition; reductions of capital.

Financial assistance for the acquisition of shares:

2J.3: only allows a company to “financially assist” the acquisition of shares in the company or its holding company if:

-It does not materially prejudice the interests of the company or its shareholders or its ability to pay its

creditors; or

-It is approved by shareholders s 260B; or

-It is exempt.

This only applies to financial assistance to buy shares.

s 206B:

Examples of financial assistance include giving a loan or giving a guarantee. Material prejudice- question of fact to be

determined in light of the circumstance. ASIC v Adler (company is impoverished overall by the transaction. Shares

were purchased in holding company (s 46 definition)- covered by s 260A.

Consequences of financial assistance breach.

s 260D:

Contravention by company but no penalty for company and transaction is still valid because …

Persons involves are liable for civil penalty…

Criminal consequences if dishonesty…

Permitted buy-backs: s 257A-257J

s 257B: Company can buy-back its own shares in certain circumstances see table.

Each shareholder has the choice of either accepting or rejecting the offer. ALL buybacks must not materially prejudice

the company’s ability to pay its creditors, AND the Acts procedures must be followed, depending on the type of

buyback. Certain buy-backs (in particular large buy-backs and selective buy-backs) must be approved by members’

resolution.

Buy back approval rules

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Increasing share capital: process of share issue: s 198(a): a decision of the board of directors. Directors must exercise their share issue power for a proper purpose. The types of share issues may include: ipo"s, private placements, rights issues, drp"s and bond issues. Some restrictions on directors; and company"s powers exist. Member approval required: member approval may be required in special circumstances. s 246b: variation of class rights. Ch 2e: related party transaction s 136(2): change to constitution s 254a(2): issuing preference shares. Disclosure under chapter 6d: unless exclusion in s 708 applies, a product disclosure statement (pds) (prospectus or offer information statement) must be prepared and lodged with asic. The pds must include mandatory disclosure about the company, the offer and the shares. There are some exemptions under s 708. s 708(1): personal offers to <20 investors and < million in 12 months s 708(8): sophisticated investors k s 708(11): rich investors- controlling >m.