ACCTG 231 Chapter Notes - Chapter 1: Matching Principle, Opportunity Cost, Variable Cost

152 views6 pages

Document Summary

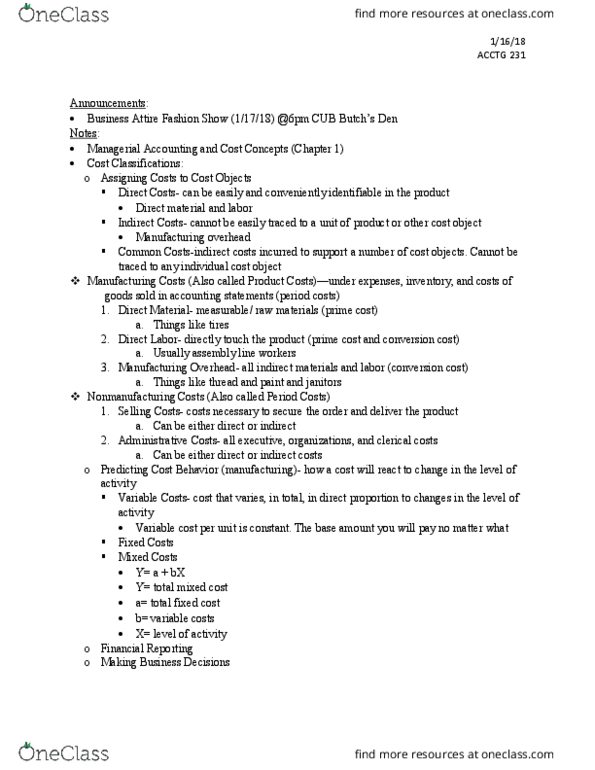

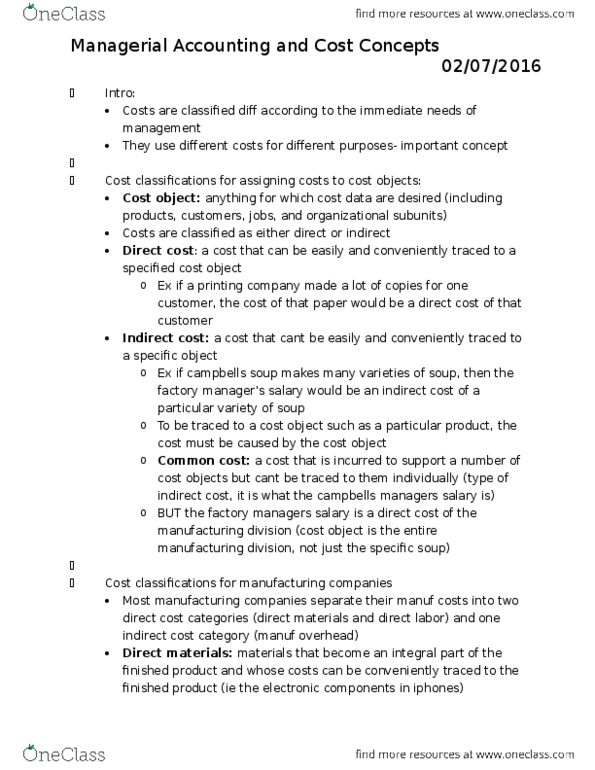

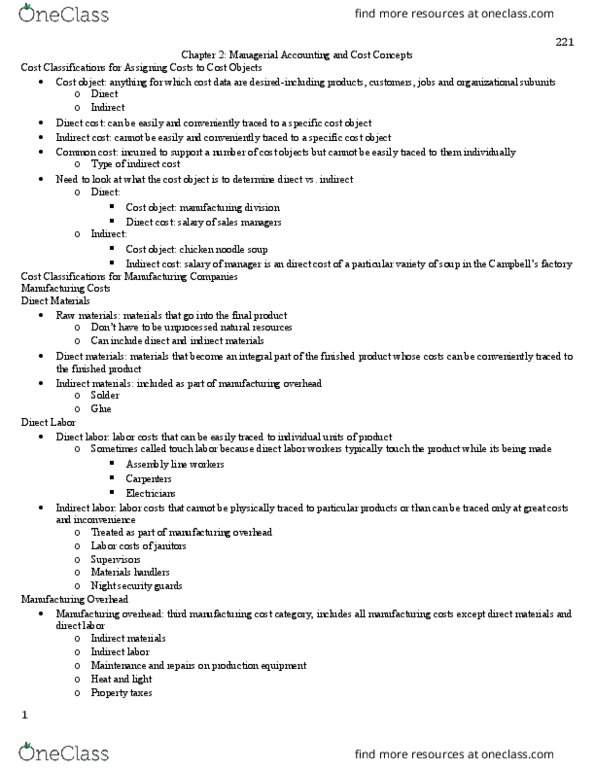

A cost object is anything for which cost data are desired: for example, products, customers, jobs, and organizational subunits. Indirect costs: direct costs can be easily and conveniently traced to a speci c cost object. For example, salaries are a direct cost of an of ce: indirect costs cannot be easily traced. For example, a soup factory manager"s salary is an indirect cost of a speci c soup. Common costs are incurred to support a number of cost objects but cannot be traced to them individually. Generally, costs are recognized as expenses on the income statement in the period that bene ts from the cost. Product vs. period costs: product costs include all costs involved in acquiring or making a product. Direct materials + direct labor + manufacturing overhead. In manufactured goods: direct materials, direct labor, and manufacturing overhead. Attach to units of product as goods are purchased/manufactured and remain attached as goods go into inventory.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Class+

$8 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

30 Verified Answers