BMGT 221 Chapter Notes - Chapter 2: Direct Labor Cost, Income Statement, Noodle

22 Apr 2016

School

Department

Course

Professor

Document Summary

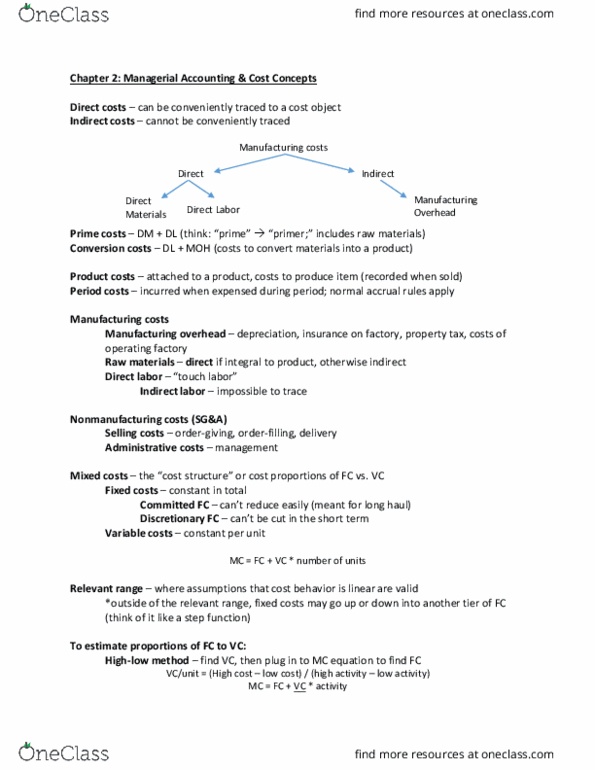

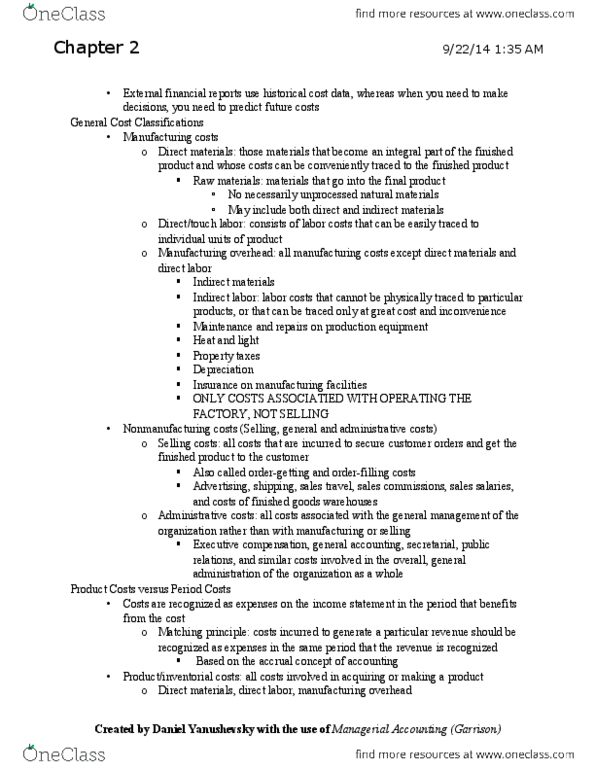

Cost classifications for assigning costs to cost objects. Cost object: anything for which cost data are desired-including products, customers, jobs and organizational subunits: direct, indirect. Direct cost: can be easily and conveniently traced to a specific cost object. Indirect cost: cannot be easily and conveniently traced to a specific cost object. Common cost: incurred to support a number of cost objects but cannot be easily traced to them individually: type of indirect cost. Need to look at what the cost object is to determine direct vs. indirect: direct: Direct cost: salary of sales managers: indirect: Indirect cost: salary of manager is an direct cost of a particular variety of soup in the campbell"s factory. Raw materials: materials that go into the final product: don"t have to be unprocessed natural resources, can include direct and indirect materials. Direct materials: materials that become an integral part of the finished product whose costs can be conveniently traced to the finished product.