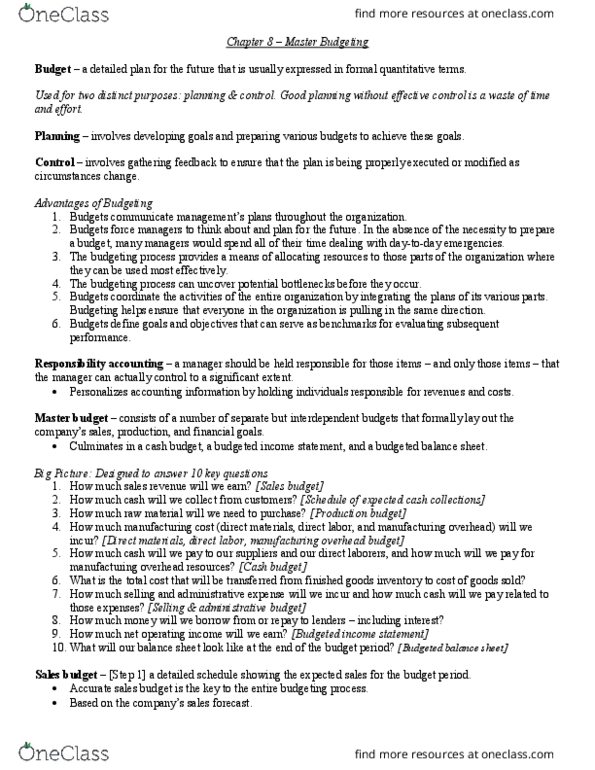

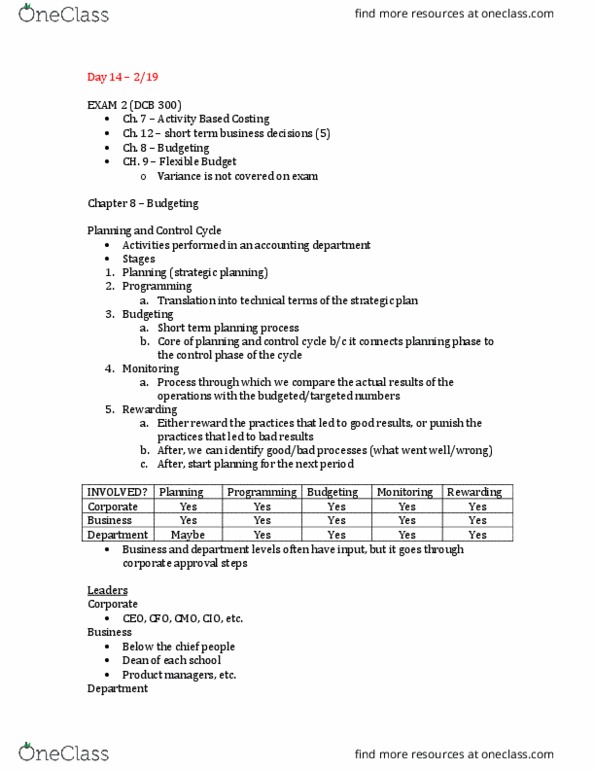

ACTG 2300 Chapter 9: Chapter 9 Textbook Notes

Get access

Related Documents

Related Questions

Several years ago, Westmont Corporation developed a comprehensive budgeting system for planning and control purposes. While departmental supervisors have been happy with the system, the factory manager has expressed considerable dissatisfaction with the information being generated by the system.

A report for the company's Assembly Department for the month of March follows:

| Assembly Department Cost Report For the Month Ended March 31 | |||||||

| Actual Results | Planning Budget | Variances | |||||

| Machine-hours | 15,000 | 20,000 | |||||

| Variable costs: | |||||||

| Supplies | $ | 10,200 | $ | 10,800 | $ | 600 | F |

| Scrap | 36,400 | 39,000 | 2,600 | F | |||

| Indirect materials | 104,600 | 124,500 | 19,900 | F | |||

| Fixed costs: | |||||||

| Wages and salaries | 81,100 | 76,000 | 5,100 | U | |||

| Equipment depreciation | 106,000 | 106,000 | â | ||||

| Total cost | $ | 338,300 | $ | 356,300 | $ | 18,000 | F |

After receiving a copy of this cost report, the supervisor of the Assembly Department stated, âThese reports are super. It makes me feel really good to see how well things are going in my department. I canât understand why those people upstairs complain so much about the reports.â

For the last several years, the companyâs marketing department has chronically failed to meet the sales goals expressed in the companyâs monthly budgets.

Required:

1. The companyâs president is uneasy about the cost reports, identify at least two reasons.

2. What kind of reports should be used to give better insight into how well departmental supervisors are controlling costs?

3. Complete the new performance report for the quarter, based on Flexible Budget Performance approach.

4. Were costs well controlled in March?

prepare a new performance report for the quarter, (Do not round your intermediate calculations. Indicate the effect of each variance by selecting "F" for favorable, "U" for unfavorable, and "None" for no effect (i.e., zero variance). Input all amounts as positive values.)

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Required 2

Static Budget vs. Flexible Budget

The production supervisor of the Machining Department forRodriguez Company agreed to the following monthly static budget forthe upcoming year:

Rodriguez Company

Machining Department Monthly Production Budget

Wages $384,000

Utilities 36,000

Depreciation 60,000

Total $480,000

The actual amount spent and the actual units produced in thefirst three months of 2016 in the Machining Department were asfollows:

Amount Spent Units Produced

January $400,000 90,000

February 440,000 100,000

March 470,000 110,000

The Machining Department supervisor has been very pleased withthis performance because actual expenditures for JanuaryâMarch havebeen less than the monthly static budget of $480,000. However, theplant manager believes that the budget should not remain fixed forevery month but should âflexâ or adjust to the volume of work thatis produced in the Machining Department. Additional budgetinformation for the Machining Department is as follows:

Wages per hour $16.00

Utility cost per direct labor hour $1.50

Direct labor hours per unit 0.20

Planned monthly unit production 120,000

Static Budget vs. Flexible Budget

The production supervisor of the Machining Department forRodriguez Company agreed to the following monthly static budget forthe upcoming year:

| Rodriguez Company Machining Department Monthly Production Budget | |

| Wages | $384,000 |

| Utilities | 36,000 |

| Depreciation | 60,000 |

| Total | $480,000 |

The actual amount spent and the actual units produced in thefirst three months of 2016 in the Machining Department were asfollows:

| Amount Spent | Units Produced | |||

| January | $400,000 | 90,000 | ||

| February | 440,000 | 100,000 | ||

| March | 470,000 | 110,000 | ||

The Machining Department supervisor has been very pleased withthis performance because actual expenditures for JanuaryâMarch havebeen less than the monthly static budget of $480,000. However, theplant manager believes that the budget should not remain fixed forevery month but should âflexâ or adjust to the volume of work thatis produced in the Machining Department. Additional budgetinformation for the Machining Department is as follows:

| Wages per hour | $16.00 |

| Utility cost per direct labor hour | $1.50 |

| Direct labor hours per unit | 0.20 |

| Planned monthly unit production | 120,000 |

X

Part A: Flexible Budget

a. Prepare a flexible budget for the actualunits produced for January, February, and March in the MachiningDepartment. Assume depreciation is a fixed cost. If required, useper unit amounts carried out to two decimal places. Enter allamounts as positive numbers.

| Rodriguez Company-Machining Department | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Flexible Production Budget | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Forthe Three Months Ending March 31, 2016 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| January | February | March | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Units of production | 90,000 | 100,000 | 110,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wages | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utilities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Depreciation | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Supportingcalculations: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Units of production | 90,000 | 100,000 | 110,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Hours per unit | x | x | x | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total hours ofproduction | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wages per hour | x $ | x $ | x $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total wages | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total hours ofproduction | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utility costs perhour | x $ | x $ | x $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total utilities Static Budget vs. Flexible Budget The production supervisor of the Machining Departmentfor Rodriguez Company agreed to the following monthly static budgetfor the upcoming year:

The actual amount spent and the actual units produced inthe first three months of 2016 in the Machining Department were asfollows:

The Machining Department supervisor has been verypleased with this performance because actual expenditures forJanuaryâMarch have been less than the monthly static budget of$480,000. However, the plant manager believes that the budgetshould not remain fixed for every month but should âflexâ or adjustto the volume of work that is produced in the Machining Department.Additional budget information for the Machining Department is asfollows:

X Part A: Flexible Budget a. Prepare a flexible budget for the actual unitsproduced for January, February, and March in the MachiningDepartment. Assume depreciation is a fixed cost. If required, useper unit amounts carried out to two decimal places. Enter allamounts as positive numbers.

X Part B: Decision Analysis b. Compare the flexible budget with the actualexpenditures for the first three months. Enter all amounts aspositive numbers.

What does this comparison suggest?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||