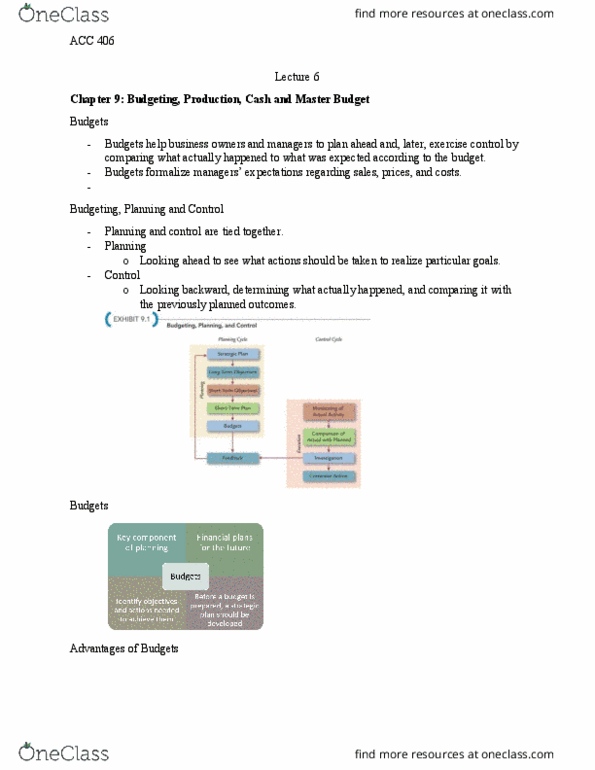

Static Budget vs. Flexible Budget

The production supervisor of the Machining Department forRodriguez Company agreed to the following monthly static budget forthe upcoming year:

Rodriguez Company

Machining Department Monthly Production Budget

Wages $384,000

Utilities 36,000

Depreciation 60,000

Total $480,000

The actual amount spent and the actual units produced in thefirst three months of 2016 in the Machining Department were asfollows:

Amount Spent Units Produced

January $400,000 90,000

February 440,000 100,000

March 470,000 110,000

The Machining Department supervisor has been very pleased withthis performance because actual expenditures for JanuaryâMarch havebeen less than the monthly static budget of $480,000. However, theplant manager believes that the budget should not remain fixed forevery month but should âflexâ or adjust to the volume of work thatis produced in the Machining Department. Additional budgetinformation for the Machining Department is as follows:

Wages per hour $16.00

Utility cost per direct labor hour $1.50

Direct labor hours per unit 0.20

Planned monthly unit production 120,000

Static Budget vs. Flexible Budget

The production supervisor of the Machining Department forRodriguez Company agreed to the following monthly static budget forthe upcoming year:

Rodriguez Company

Machining Department

Monthly Production Budget Wages $384,000 Utilities 36,000 Depreciation 60,000 Total $480,000

The actual amount spent and the actual units produced in thefirst three months of 2016 in the Machining Department were asfollows:

Amount Spent Units Produced January $400,000 90,000 February 440,000 100,000 March 470,000 110,000

The Machining Department supervisor has been very pleased withthis performance because actual expenditures for JanuaryâMarch havebeen less than the monthly static budget of $480,000. However, theplant manager believes that the budget should not remain fixed forevery month but should âflexâ or adjust to the volume of work thatis produced in the Machining Department. Additional budgetinformation for the Machining Department is as follows:

Wages per hour $16.00 Utility cost per direct labor hour $1.50 Direct labor hours per unit 0.20 Planned monthly unit production 120,000

X

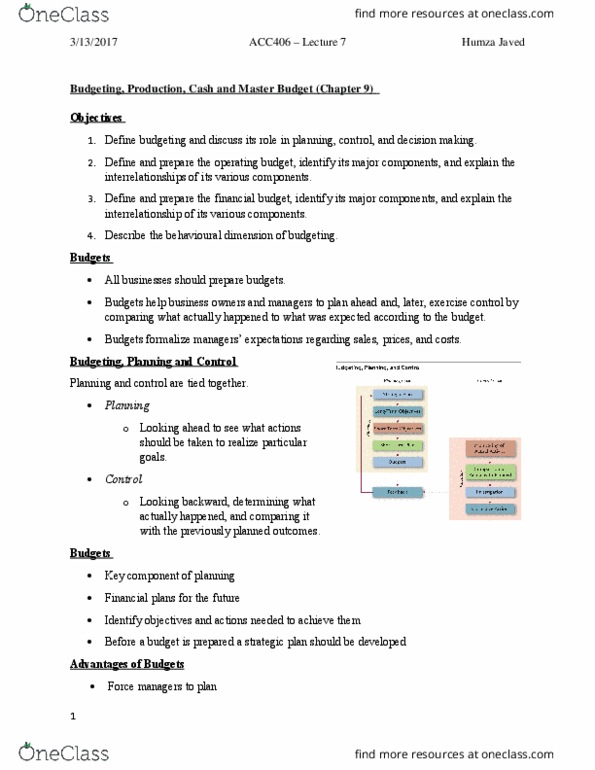

Part A: Flexible Budget

a. Prepare a flexible budget for the actualunits produced for January, February, and March in the MachiningDepartment. Assume depreciation is a fixed cost. If required, useper unit amounts carried out to two decimal places. Enter allamounts as positive numbers.

Rodriguez Company-Machining Department Flexible Production Budget Forthe Three Months Ending March 31, 2016 January February March Units of production 90,000 100,000 110,000 Wages $ $ $ Utilities Depreciation Total $ $ $ Supportingcalculations: Units of production 90,000 100,000 110,000 Hours per unit x x x Total hours ofproduction Wages per hour x $ x $ x $ Total wages $ $ $ Total hours ofproduction Utility costs perhour x $ x $ x $ Total utilities

Static Budget vs. Flexible Budget

The production supervisor of the Machining Departmentfor Rodriguez Company agreed to the following monthly static budgetfor the upcoming year:

Rodriguez Company

Machining Department

Monthly Production Budget Wages $384,000 Utilities 36,000 Depreciation 60,000 Total $480,000

The actual amount spent and the actual units produced inthe first three months of 2016 in the Machining Department were asfollows:

Amount Spent Units Produced January $400,000 90,000 February 440,000 100,000 March 470,000 110,000

The Machining Department supervisor has been verypleased with this performance because actual expenditures forJanuaryâMarch have been less than the monthly static budget of$480,000. However, the plant manager believes that the budgetshould not remain fixed for every month but should âflexâ or adjustto the volume of work that is produced in the Machining Department.Additional budget information for the Machining Department is asfollows:

Wages per hour $16.00 Utility cost per direct labor hour $1.50 Direct labor hours per unit 0.20 Planned monthly unit production 120,000

X

Part A: Flexible Budget

a. Prepare a flexible budget for the actual unitsproduced for January, February, and March in the MachiningDepartment. Assume depreciation is a fixed cost. If required, useper unit amounts carried out to two decimal places. Enter allamounts as positive numbers.

Rodriguez Company-Machining Department Flexible Production Budget Forthe Three Months Ending March 31, 2016 January February March Units of production 90,000 100,000 110,000 Wages $ $ $ Utilities Depreciation Total $ $ $ Supportingcalculations: Units of production 90,000 100,000 110,000 Hours per unit x x x Total hours ofproduction Wages per hour x $ x $ x $ Total wages $ $ $ Total hours ofproduction Utility costs perhour x $ x $ x $ Total utilities $ $ $

X

Part B: Decision Analysis

b. Compare the flexible budget with the actualexpenditures for the first three months. Enter all amounts aspositive numbers.

January February March Total flexible budget $ $ $ Actual cost Excess of actual cost over budget $ $ $

What does this comparison suggest?

The Machining Department has performed better than originallythought. The department is spending more than would be expected.

Static Budget vs. Flexible Budget

The production supervisor of the Machining Department forRodriguez Company agreed to the following monthly static budget forthe upcoming year:

Rodriguez Company

Machining Department Monthly Production Budget

Wages $384,000

Utilities 36,000

Depreciation 60,000

Total $480,000

The actual amount spent and the actual units produced in thefirst three months of 2016 in the Machining Department were asfollows:

Amount Spent Units Produced

January $400,000 90,000

February 440,000 100,000

March 470,000 110,000

The Machining Department supervisor has been very pleased withthis performance because actual expenditures for JanuaryâMarch havebeen less than the monthly static budget of $480,000. However, theplant manager believes that the budget should not remain fixed forevery month but should âflexâ or adjust to the volume of work thatis produced in the Machining Department. Additional budgetinformation for the Machining Department is as follows:

Wages per hour $16.00

Utility cost per direct labor hour $1.50

Direct labor hours per unit 0.20

Planned monthly unit production 120,000

Static Budget vs. Flexible Budget

The production supervisor of the Machining Department forRodriguez Company agreed to the following monthly static budget forthe upcoming year:

| Rodriguez Company Machining Department Monthly Production Budget | |

| Wages | $384,000 |

| Utilities | 36,000 |

| Depreciation | 60,000 |

| Total | $480,000 |

The actual amount spent and the actual units produced in thefirst three months of 2016 in the Machining Department were asfollows:

| Amount Spent | Units Produced | |||

| January | $400,000 | 90,000 | ||

| February | 440,000 | 100,000 | ||

| March | 470,000 | 110,000 | ||

The Machining Department supervisor has been very pleased withthis performance because actual expenditures for JanuaryâMarch havebeen less than the monthly static budget of $480,000. However, theplant manager believes that the budget should not remain fixed forevery month but should âflexâ or adjust to the volume of work thatis produced in the Machining Department. Additional budgetinformation for the Machining Department is as follows:

| Wages per hour | $16.00 |

| Utility cost per direct labor hour | $1.50 |

| Direct labor hours per unit | 0.20 |

| Planned monthly unit production | 120,000 |

X

Part A: Flexible Budget

a. Prepare a flexible budget for the actualunits produced for January, February, and March in the MachiningDepartment. Assume depreciation is a fixed cost. If required, useper unit amounts carried out to two decimal places. Enter allamounts as positive numbers.

| Rodriguez Company-Machining Department | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Flexible Production Budget | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Forthe Three Months Ending March 31, 2016 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| January | February | March | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Units of production | 90,000 | 100,000 | 110,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wages | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utilities | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Depreciation | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Supportingcalculations: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Units of production | 90,000 | 100,000 | 110,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Hours per unit | x | x | x | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total hours ofproduction | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wages per hour | x $ | x $ | x $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total wages | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total hours ofproduction | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utility costs perhour | x $ | x $ | x $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total utilities Static Budget vs. Flexible Budget The production supervisor of the Machining Departmentfor Rodriguez Company agreed to the following monthly static budgetfor the upcoming year:

The actual amount spent and the actual units produced inthe first three months of 2016 in the Machining Department were asfollows:

The Machining Department supervisor has been verypleased with this performance because actual expenditures forJanuaryâMarch have been less than the monthly static budget of$480,000. However, the plant manager believes that the budgetshould not remain fixed for every month but should âflexâ or adjustto the volume of work that is produced in the Machining Department.Additional budget information for the Machining Department is asfollows:

X Part A: Flexible Budget a. Prepare a flexible budget for the actual unitsproduced for January, February, and March in the MachiningDepartment. Assume depreciation is a fixed cost. If required, useper unit amounts carried out to two decimal places. Enter allamounts as positive numbers.

X Part B: Decision Analysis b. Compare the flexible budget with the actualexpenditures for the first three months. Enter all amounts aspositive numbers.

What does this comparison suggest?

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||