ACCT20100 Chapter 7: Chapter 7.2- FIFO and LIFO

Document Summary

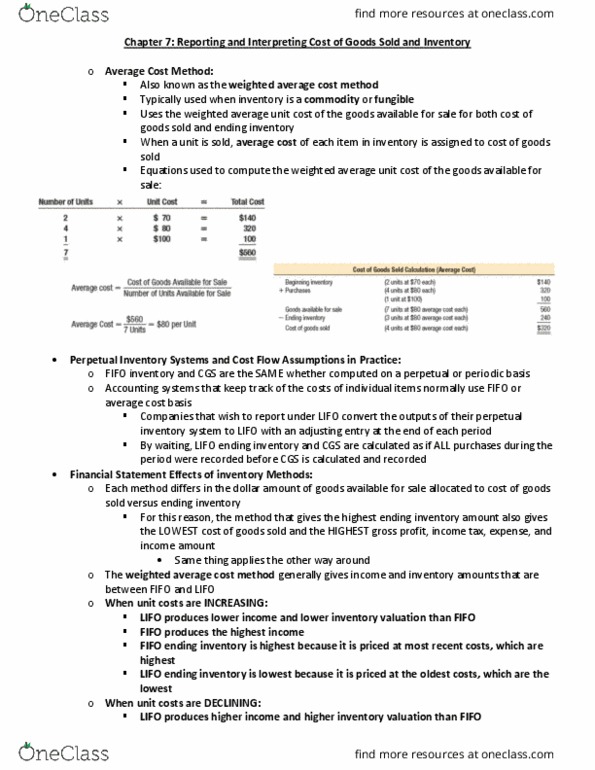

Chapter 7: reporting and interpreting cost of goods sold and inventory. Cost flow assumptions: the choice of an inventory costing method is not based on the physical flow of goods on and off the shelves this is why they are called cost flow assumptions. Similar to flows of inventory in and out of the bin: first-in, first-out method (fifo): Assumes that the earliest goods purchased (the first ones in) are the first goods sold, ad the last goods purchased are left in ending inventory. Assign the older costs to the units sold, which leaves the more recent costs to be used to value ending inventory. Under fifo, cost of goods sold and ending inventory are computed as if the flows in and out of the fifo inventory bin. Each good sold is then removed from the bottom in sequence bottom to top. The first costs into inventory are the first costs out to cost of goods sold.