ACCT20100 Chapter Notes - Chapter 7: Income Statement, Inventory Turnover

Document Summary

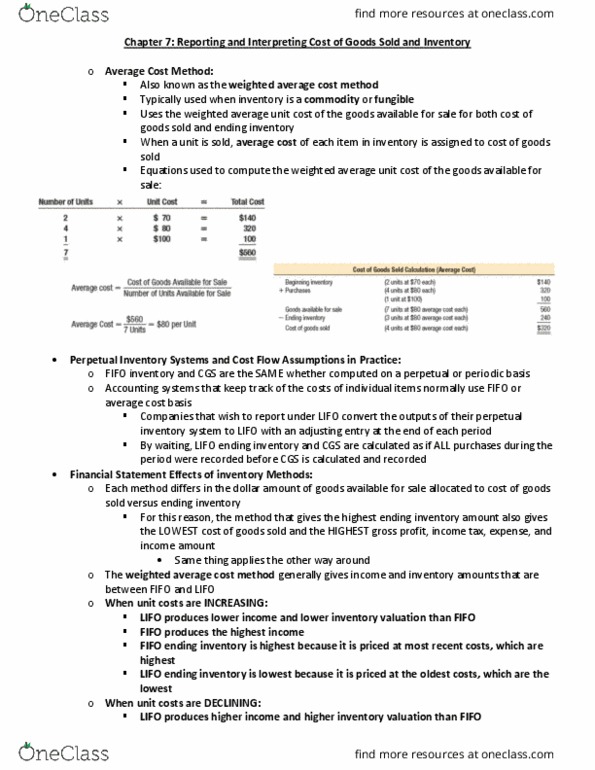

Chapter 7: reporting and interpreting cost of goods sold and inventory. Inventory methods and financial statement analysis: remember: cost flow assumptions affect how goods available for sale are allocated to ending inventory and cgs does not affect the recording of purchases. Ending inventory differs under different cost flow assumption methods, and as a result, so is beginning inventory: converting the income statement to fifo: If (cid:449)e k(cid:374)o(cid:449) the differe(cid:374)(cid:272)es (cid:271)et(cid:449)ee(cid:374) a (cid:272)o(cid:373)pa(cid:374)y"s i(cid:374)(cid:448)e(cid:374)tory valued at. Lifo and fifo for both beginning and ending inventory, we can compute the difference in cgs. Lifo reserve: also known as excess of fifo over lifo disclosed by. Lifo users in their inventory footnotes so that differences between lifo and fifo cgs can be reported. Example: converting inventory on the balance sheet to fifo: Can achieve this by substituting the fifo values in note for the lifo values on the balance sheet.