EC223 Chapter Notes - Chapter 6: Dbrs, Credit Rating Agency, Liquidity Premium

Document Summary

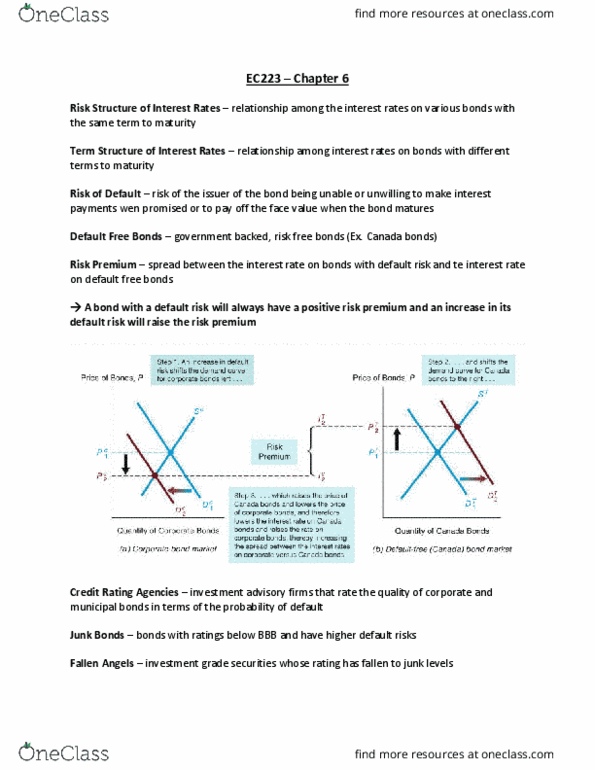

The risk and term structure of interest rates p. 113-168. Risk structure of interest rates: default risk, liquidity. Term structure of interest rates: expectations theory, segmented markets theory, liquidity premium theory. Corporate, provincial and canada: same maturity but different interest rate level. Bonds with identical risk, liquidity characteristics may have different interest rates because the time remaining to maturity is different. Significant observation: wide gap during recession between government bonds vs corporations. Fitch: bonds with relatively low risk default are called investment-grade securities and have a rating of. Bbb and above: bonds with rating below bbb have higher default risk are called speculative-grade or junk bond, because the bonds always have higher interest rates than investment-grade securities, they are also referred to as high-yield bonds. Inverted: long term rates are below short term rates. Facts that the theory of the term structure of interest rates must explain. 2 i t i nt i t i e t.