ECO101H1 Chapter Notes - Chapter 13: Average Cost, Average Variable Cost, Marginal Cost

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

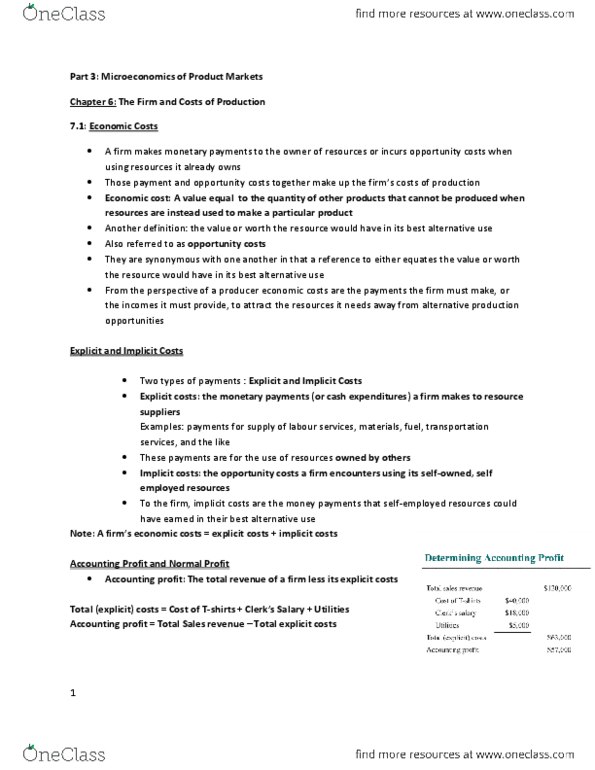

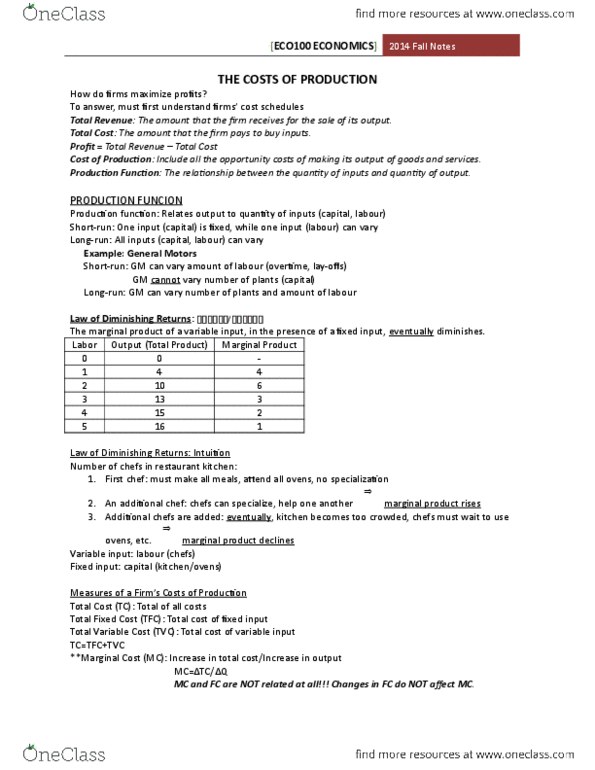

Total revenue (for a firm) the amount a firm receives for the sale of its output. Total cost the market value of the inputs a firm uses in production. Total profit total revenue total cost. Explicit costs input costs that require an outlay of money by the firm. Implicit costs input costs that do not require an outlay of money by the firm. Economic profit total revenue total cost, including both explicit and implicit cost. Accounting profit total revenue explicit cost. Production function the relationship between quantity of inputs used to make a good and the quantity of output of that good. Marginal product the increase in output that arises from an additional unit of input. Diminishing marginal product the property whereby the marginal product of an input declines as the quantity of the input increases. Fixed costs costs that do not vary with the quantity of output produced.