ECO101H1 Lecture Notes - Lecture 6: Average Cost, Average Variable Cost, Marginal Cost

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

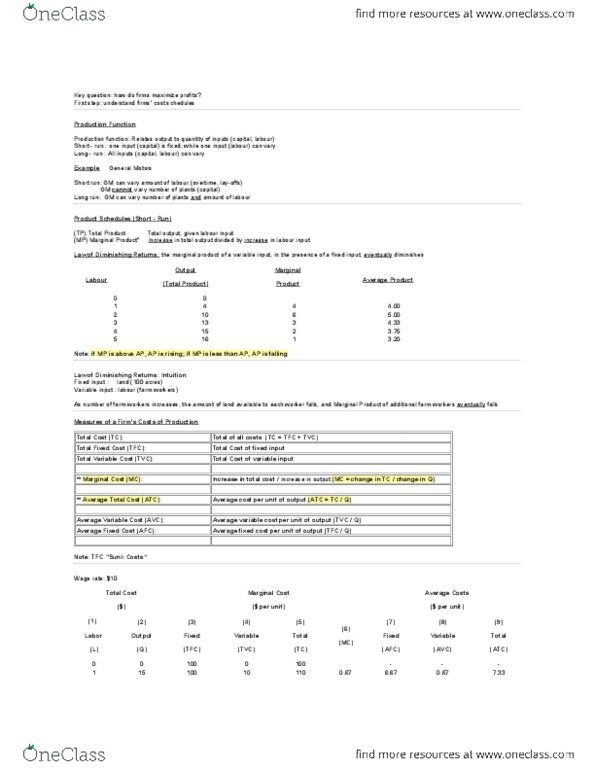

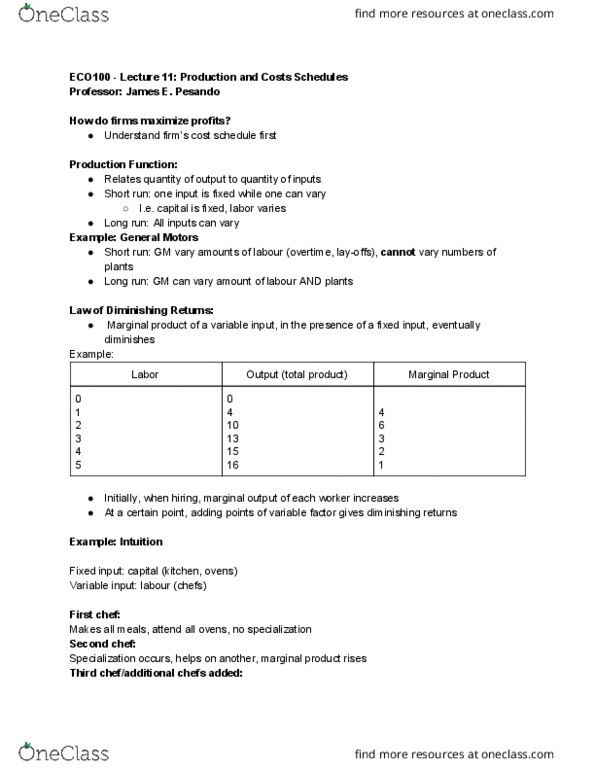

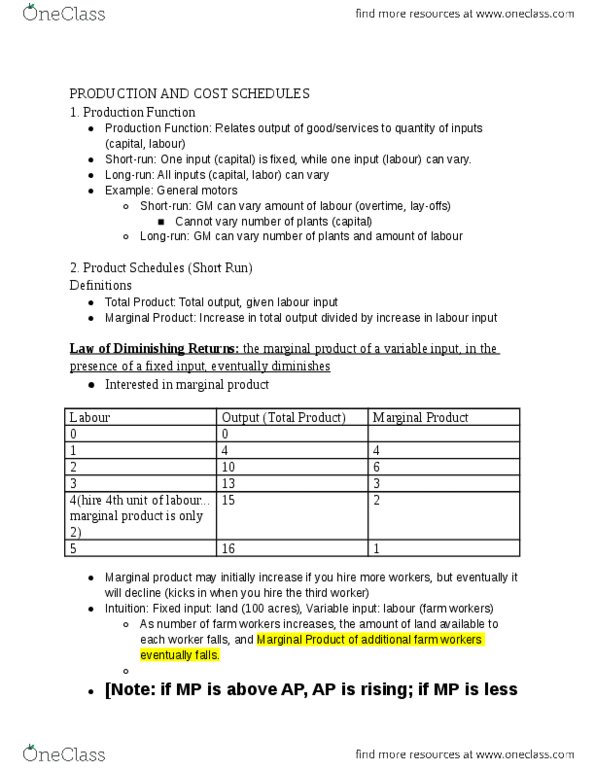

To answer, must first understand firms" cost schedules. Total revenue: the amount that the firm receives for the sale of its output. Total cost: the amount that the firm pays to buy inputs. Cost of production: include all the opportunity costs of making its output of goods and services. Production function: the relationship between the quantity of inputs and quantity of output. Production function: relates output to quantity of inputs (capital, labour) Short-run: one input (capital) is fixed, while one input (labour) can vary. Short-run: gm can vary amount of labour (overtime, lay-offs) Long-run: gm can vary number of plants and amount of labour. The marginal product of a variable input, in the presence of a fixed input, eventually diminishes. Total fixed cost (tfc): total cost of fixed input. Total variable cost (tvc): total cost of variable input. **marginal cost (mc): increase in total cost/increase in output. Mc and fc are not related at all!!!