AFM291 Chapter Notes - Chapter 6: Total Absorption Costing, Consignee, Consignor

23 Oct 2018

School

Department

Course

Professor

Document Summary

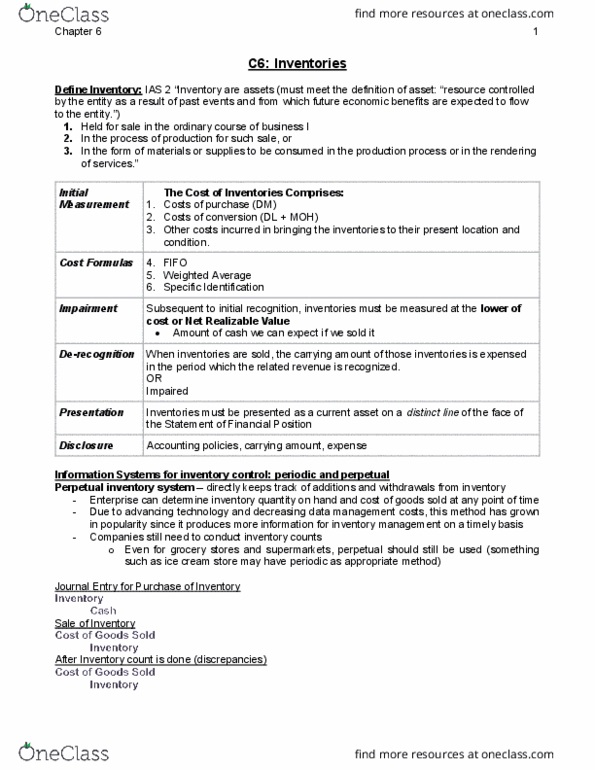

Increasing popularity due to technology: can identify shrinkages: inventory losses from theft or damage. Periodic system: relies on periodic inventory counts to infer the accounts withdrawn from inventory: determine ending inventory quantity and applies product costs to determine cost of ending inventory, can only determine actual amount of cogs. Cost of inventories include all costs of purchase, costs of conversion and other costs incurred in bringing the inventories to their present location and condition. F. o. b. origin (shipping point): buyer takes possession when the goods leave the supplier"s premises. F. o. b. destination: buyer takes possession when the goods reach the buyer"s premises. Later expensing these costs through cogs when the products are sold matches costs to the revenues generated. Fixed overhead capitalization when production is above normal: under absorption costing, an enterprise can lower cogs by increasing production volume. Important to distinguish increasing gross margins due to improved cost management from the portion to changes in production levels.