AFM291 Chapter Notes - Chapter 6: Continuous Track, Consignor, Consignee

18 May 2018

School

Department

Course

Professor

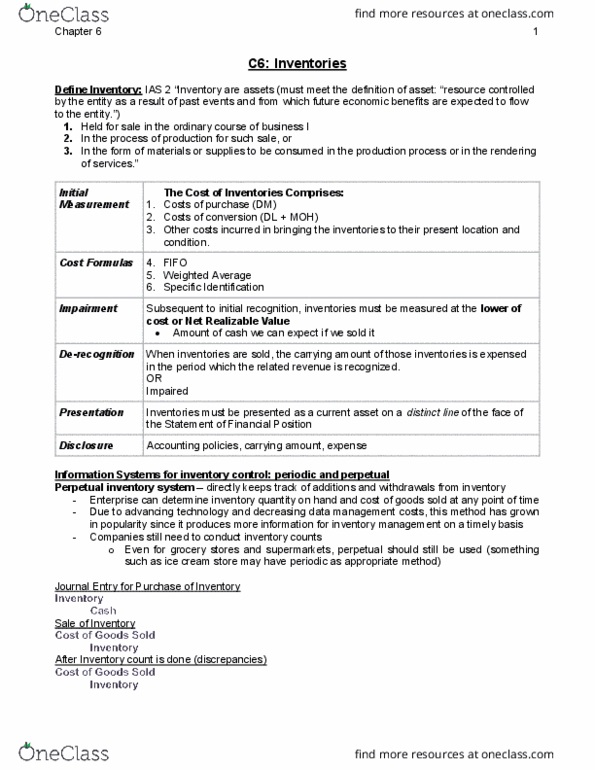

Inventories

A. Information Systems for Inventory Control

- Perpetual inventory system: directly keeps track of additions to and withdrawals from

inventory

- Enterprise can determine inventory quantity on hand and COGS from the accounting

records at any point in time

- Produces more information for management of inventory levels on a timely basis

- Companies still need to conduct an inventory count even if they use the perpetual

method since the records may not correctly represent actual inventory quantities

- Has the ability to identify both the expected and actual amount of COGS

- E. a idetif shikage ieto losses fo theft o eakage → a help

decide whether it would be worthwhile to put in place additional inventory

management practices

- Periodic inventory system: does’t keep otiuous tak of ietoies ad COG“

- On the financial statement date, the enterprise conducts an inventory count to

determine the ending inventory quantity and applies product costs to these quantities

to determine the cost of ending inventory

- Uses a tepoa aout losed at the ed of the ea → puhases, so that the

company can distinguish changes in inventory arising from purchases rather than

adjustments to the inventory balance resulting from the inventory count.

- See exhibit 6-2 on page 243

- The inventory system chosen affects the implementation of different cost flow assumptions

B. Initial Recognition and Measurement

- IA“ → the ost of ietoies shall opise all osts of puhase, osts of oesio, ad

other costs incurred in bringing the inventories to their present location and condition

1. Purchased Goods

- Ieto ost fo goods puhased fo esale → puhase pie, a taes that ae’t

recoverable from the government, shipping and handling costs, and any other costs

incurred up to the point where the product is at the desired location for sale

- Important to determine whether goods in transit from a supplier or to a customer should be

included in inventory

- Free on board: point at which the buyer takes legal possession of the goods

- FOB origin/shipping point: buyer takes possession as soon as the goods leave the

supplie’s peises

- FOB destiatio: ue takes possessio he the goods eah the ue’s peises

- At the year end, an enterprise should include in inventories goods that are on its premises,

and inbound goods in transit that are FOB origin and outbound goods in transit that are FOB

destination

- Risks and rewards of ownership do not transfer from the consignor to the consignee, and

the latter should not include consigned goods in its inventories

find more resources at oneclass.com

find more resources at oneclass.com

2. Manufactured Goods

- Product costs: all costs incurred in the acquisition of raw materials and the conversion

process

- Include: materials, production labor (including factory supervision), VOH (ex.

electricity), and FOH (ex. heating costs)

- Should be capitalized since they incurred as part of the production process

- Period costs: costs that should not be capitalized in inventory because they are not closely

related to the production process

- Ex. marketing, administration, accounting, and finance

- Expense period costs in the period incurred

- Two views to determine whether an expenditure on FOH is a product or period cost:

- Variable costing: considers fixed manufacturing OH to be a period cost because such

osts do’t a aodig to podutio leel

- Absorption costing: considers FOH as a product cost because production cannot take

place without these costs

- Managerial accounting and internal decision making favor the variable costing method

- IFRS and ASPE require the use of absorption costing for external financial reporting

- It’s osistet ith the Coeptual Faeok → etepises iu FOH costs to

produce goods that generate revenue in the future, so such costs meet the definition

of an asset

- The later expensing of these costs through COGS when the products are sold matches

costs to the revenue generated.

- The capitalization of FOH creates issues when production levels significantly deviate from

normal production levels

a. FOH capitalization when production is above normal

- See exhibit 6-4 on page 246

- Under absorption costing, an enterprise can lower COGS by increasing production volume

- Increases in production volume will result in decreases in the fixed cost per unit

- If a manager needed extra income, for example to meet an earnings target, then they

could raise production at the end of the year so the ending inventories absorbed more

FOH

- It’s ipotat to distiguish ieasig goss agis that ae due to ipoed ost

management from the portion due to changes in production levels

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Perpetual inventory system: directly keeps track of additions to and withdrawals from inventory. Enterprise can determine inventory quantity on hand and cogs from the accounting records at any point in time. Produces more information for management of inventory levels on a timely basis. Companies still need to conduct an inventory count even if they use the perpetual method since the records may not correctly represent actual inventory quantities. Has the ability to identify both the expected and actual amount of cogs. E(cid:454). (cid:272)a(cid:374) ide(cid:374)tif(cid:455) (cid:862)sh(cid:396)i(cid:374)kage(cid:863) (cid:894)i(cid:374)(cid:448)e(cid:374)to(cid:396)(cid:455) losses f(cid:396)o(cid:373) theft o(cid:396) (cid:271)(cid:396)eakage(cid:895) (cid:272)a(cid:374) help decide whether it would be worthwhile to put in place additional inventory management practices. Periodic inventory system: does(cid:374)"t keep (cid:272)o(cid:374)ti(cid:374)uous t(cid:396)a(cid:272)k of i(cid:374)(cid:448)e(cid:374)to(cid:396)ies a(cid:374)d cog . On the financial statement date, the enterprise conducts an inventory count to determine the ending inventory quantity and applies product costs to these quantities to determine the cost of ending inventory.