ACC 703 Chapter 2: Chapter 2 - Investments in Equity Securities.pdf

30 Nov 2014

School

Department

Course

Professor

Document Summary

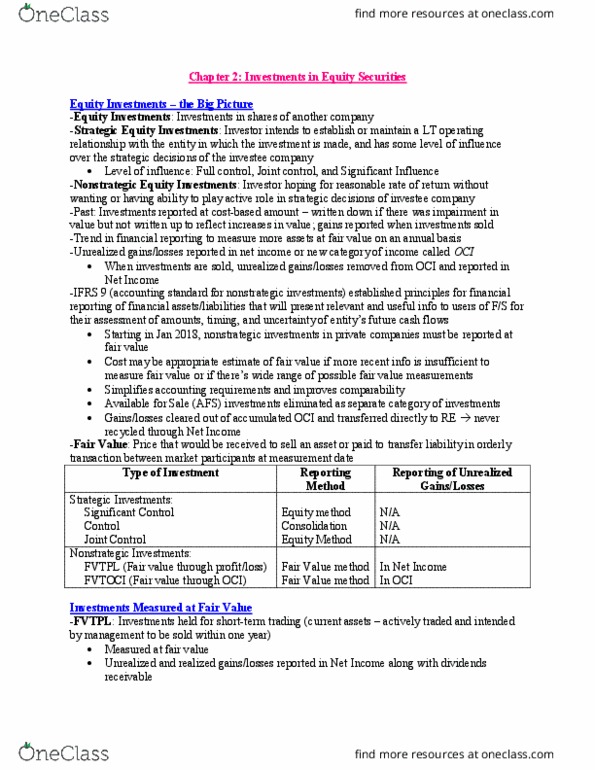

Ias 39: unrealized gains/losses were reported in net income of other. Comprehensive income (oci) and unrealized gains/losses were recycled through net income when investment was sold. Never go through net income anymore. Joint control through joint venture. Fvtpl (fair value through profit or. Other elect fvtoci (fair value. Reporting method reporting of. Ifrs 11: joint arrangements: owners must have made a contractual arrangement that establishes joint control over the venture. No single venturer is able to unilaterally control the venture. Ifrs 8: disaggregation into operating segments and disclosures about products, geographical areas and major customer is required over a joint venture. Section for profit and loss. Ias 36: impairment of assets. Ias 38: intangible assets acquired during business combinations. Ifric 16: hedges of a net investment in a foreign operation. Include investments held for short- term trading. Initially measured at fv and subsequently remeasured at fv every reporting date: adjusted for acquisition differential. Investments measured at fair value.