BU487 Chapter Notes - Chapter 2: Historical Cost, Liquidating Distribution, Financial Statement

Document Summary

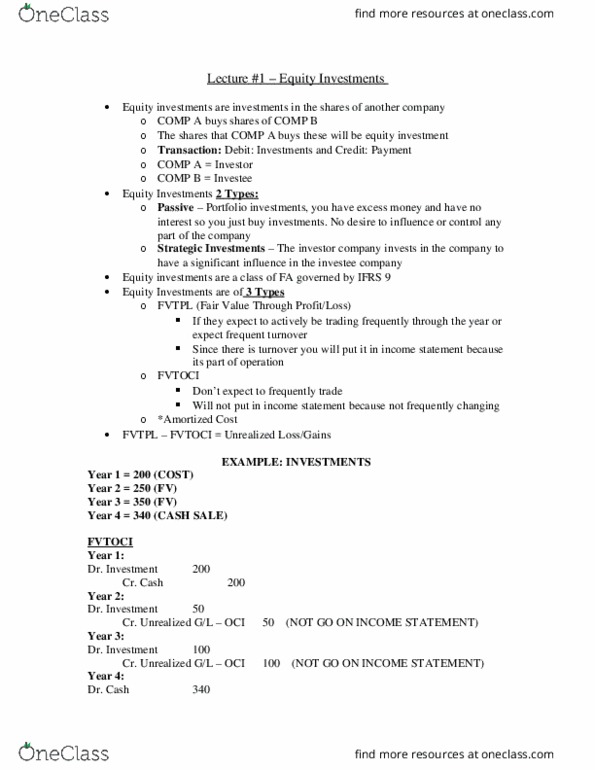

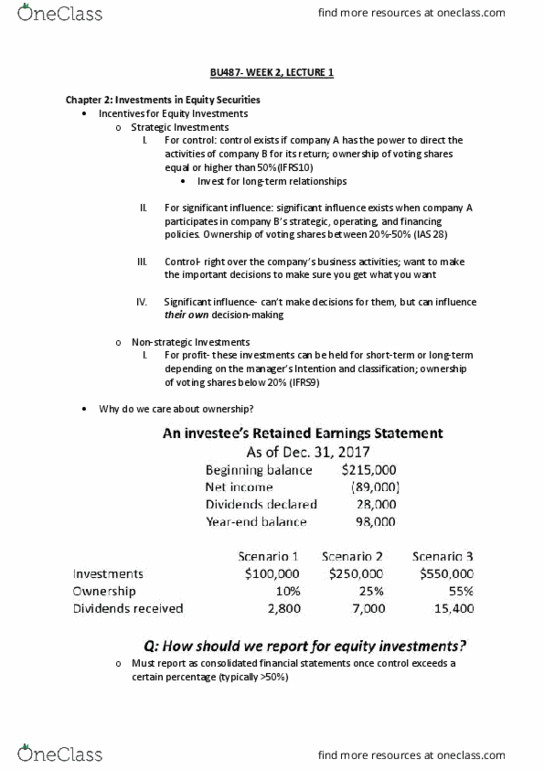

Equity investments: investments in shares of another company. Strategic equity investments: investor intends to establish or maintain a lt operating relationship with the entity in which the investment is made, and has some level of influence over the strategic decisions of the investee company. Level of influence: full control, joint control, and significant influence. Nonstrategic equity investments: investor hoping for reasonable rate of return without wanting or having ability to play active role in strategic decisions of investee company. Past: investments reported at cost-based amount written down if there was impairment in value but not written up to reflect increases in value; gains reported when investments sold. Trend in financial reporting to measure more assets at fair value on an annual basis. Unrealized gains/losses reported in net income or new category of income called oci. When investments are sold, unrealized gains/losses removed from oci and reported in.