COMMERCE 2AB3 Chapter 2: 2AB3 Chapter 2 Textbook Notes

18 Jan 2018

School

Department

Course

Professor

Document Summary

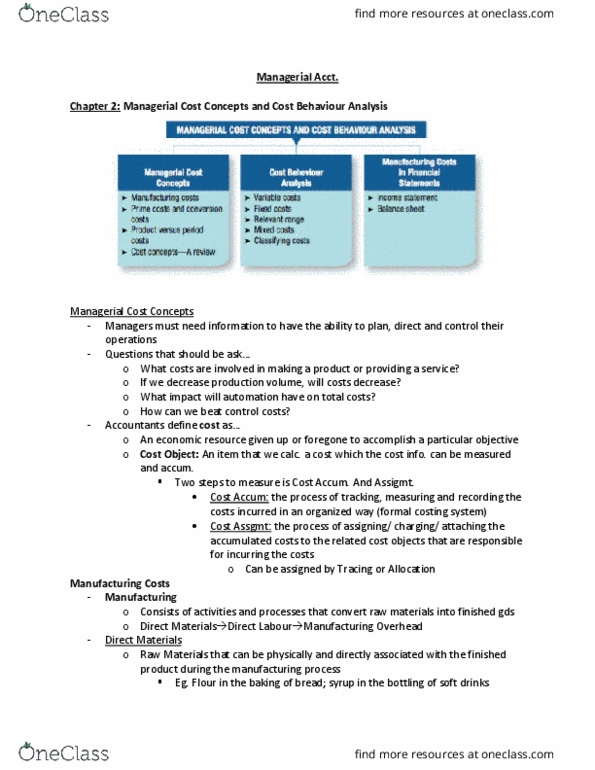

Chapter two: managerial cost concepts and cost behaviour analysis. Three subsections of this chapter: managerial cost concepts, cost behaviour analysis, manufacturing costs in financial statements. Three classes of manufacturing costs: direct materials, raw materials are purchased to be converted into the finished product, these are directly associated with creating the product, i. e. flour for making bread, rubber for making tires. Indirect materials are not physically associated with the finished product (such as lubricants or polishing compounds) or cannot be easily traced to the finished product such as sandpaper or glue. Indirect materials are part of the manufacturing overhead: direct labour, the work of factory employees that is physically and directly associated with converting raw materials into finished goods. Indirect labour on the other hand, is the work of employees who either have no physical association with the physical product or cannot be practically traced to it. Wages of maintenance people, timekeepers and supervisors are examples of indirect labour.