COMMERCE 2AB3 Chapter Notes - Chapter 2: Finished Good, Behaviorism, Variable Cost

29 Jan 2017

School

Department

Course

Professor

Document Summary

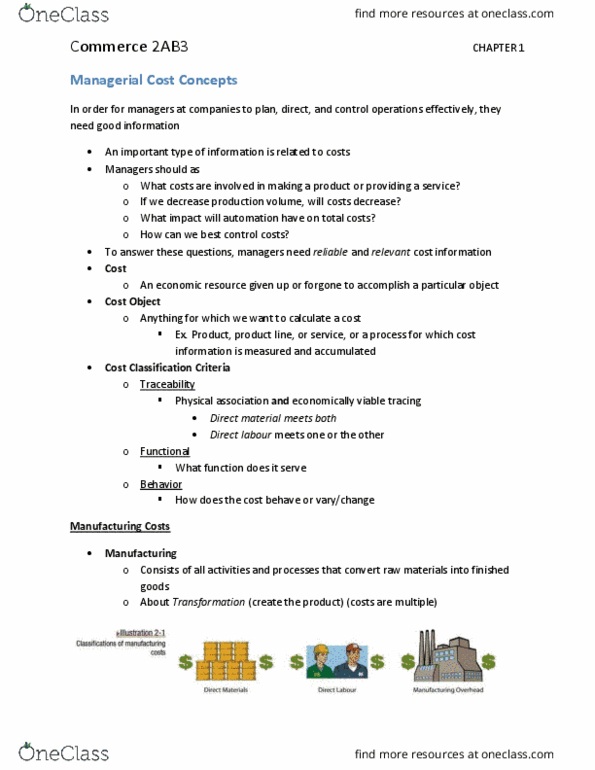

Chapter 2: managerial cost concepts and cost behaviour analysis. Cost: an economic resource given up or forgone to accomplish a particular objective. Cost-objective: anything for which we want to calculate a cost. Manufacturing: consist s of activities and processes that convert raw materials into finished goods. In contrast, merchandising sells goods in the same form in which they are purchased. Manufacturing costs are typically direct materials, direct labour, manufacturing overhead. Raw materials are basic materials and parts used in manufacturing. Raw materials that can be physically and directly associated with the finished product are called direct materials: eg. Flour in the baking of bread, syrup in the bottling of soft drinks, steel sued in making automobiles. Work of factory employees that can be physically and directly associated with converting raw materials into finished goods is direct labour: eg. Bottlers at coca-cola, bankers at sara lee, typesetters at a newspaper. Costs that are indirectly associated with manufacturing of finished goods.