ACCT1501 Chapter Notes - Chapter 15: Inventory Turnover, Gross Margin, Profit Margin

24 May 2018

School

Department

Course

Professor

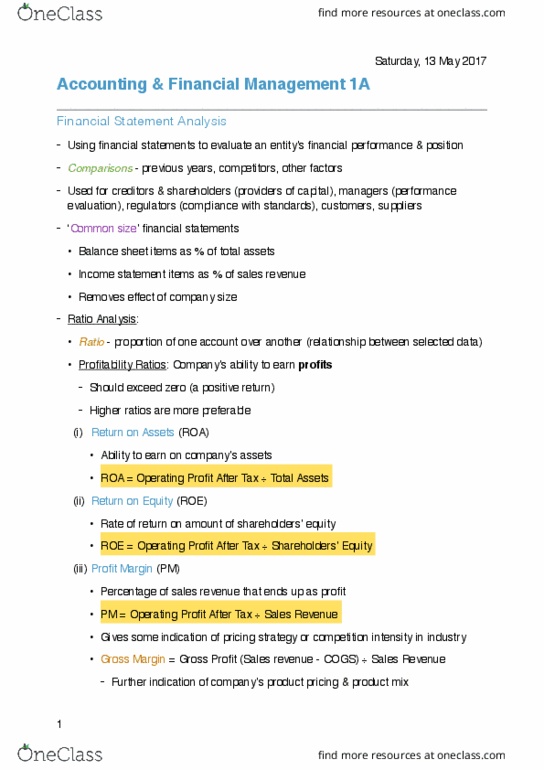

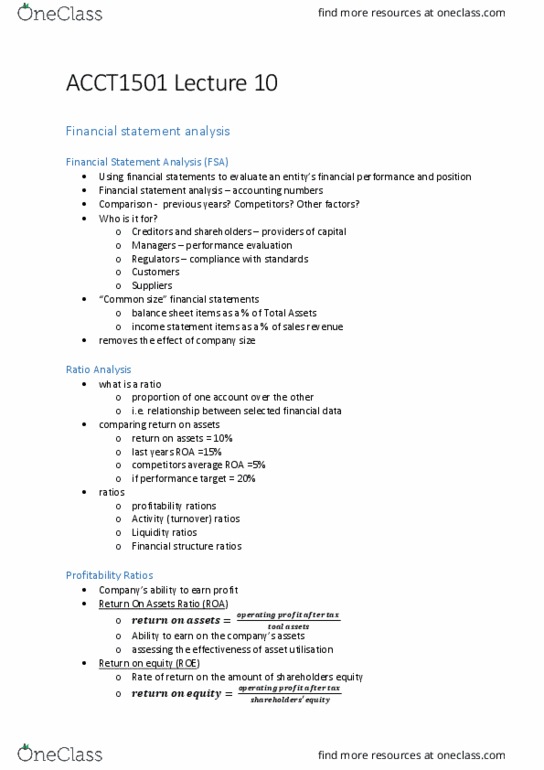

Financial Statement Analysis

- Evaluate a etits fiaial perforae ad positio

- Comparison: previous years, competitors, other factors (look at business strategies, financial

condition, to interpret figures more accurately)

➢ Creditors & Shareholders – providers of capital

➢ Managers – performance evaluation

➢ Regulators – Compliance with standards

➢ Customers

➢ Suppliers

➢ Financial institutions – need to know the level of debt the company has influence not

only the level of loans, but also interest rates they will charge

Ratio Analysis: Proportion of one account over the other

- Profitability ratios – generate earnings compared to expenses

➢ ROA (return on assets) – OPAT/ TA

➢ ROE (return on equity) – OPAT/ SE

➢ PM (profit margin) – OPAT/ Sales Revenue

Gives some indication of pricing strategy or competition intensity in the industry

• Gross argi: further idiatio of the opas produt priig ad produt i

Measure profitability in buying/selling goods before other expensed are covered

Useful for managers – influences no. of products they sell and price they should sell at.

➢ EPS (earnings per share) – OPAT – Div/ WA no. of ord shares outstanding (av no. of

shares company sells

(!!!) Ratios SHOULD exceed 0 (positive return)

- Activities (turnover) ratios – convert assets/liabilities into cash

➢ Assets turnover – Sales / TA

➢ Inventory turnover – COGS / Inventory (closing)

E.g. poor inventory = stock obsoletes

Want turnover inventory as many x as possible (hold inventory as short as possible

➢ Debtors Turnover – Credit Sales / AR

Efficiency of the company (covert AR to cash)

• R/S between ratios: ROA may be affected by changes in profit margin &/ in assets

turover opas leverage

ROE = ROA x LEVERAGE

OPAT/ SE = OPAT/TA x TA/SE

- Liquidity – ability to pay short term financial obligations

➢ Current ratio – CA/CL

➢ Quick ratio (Acid test) – Cash + AR + Short term Investment / CL

Look at emergency cash

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Comparison: previous years, competitors, other factors (look at business strategies, financial condition, to interpret figures more accurately) Creditors & shareholders providers of capital. Financial institutions need to know the level of debt the company has influence not only the level of loans, but also interest rates they will charge. Ratio analysis: proportion of one account over the other. Profitability ratios generate earnings compared to expenses. Roa (return on assets) opat/ ta. Roe (return on equity) opat/ se. Pm (profit margin) opat/ sales revenue. Gives some indication of pricing strategy or competition intensity in the industry: gross (cid:373)argi(cid:374): further i(cid:374)di(cid:272)atio(cid:374) of the (cid:272)o(cid:373)pa(cid:374)(cid:455)(cid:859)s produ(cid:272)t pri(cid:272)i(cid:374)g a(cid:374)d produ(cid:272)t (cid:373)i(cid:454) Measure profitability in buying/selling goods before other expensed are covered. Useful for managers influences no. of products they sell and price they should sell at. Eps (earnings per share) opat div/ wa no. of ord shares outstanding (av no. of shares company sells. Activities (turnover) ratios convert assets/liabilities into cash.