ADMS 4540 Study Guide - Financial Institution, Handy Manny, Arbitrage

21 Oct 2013

School

Department

Course

Professor

Document Summary

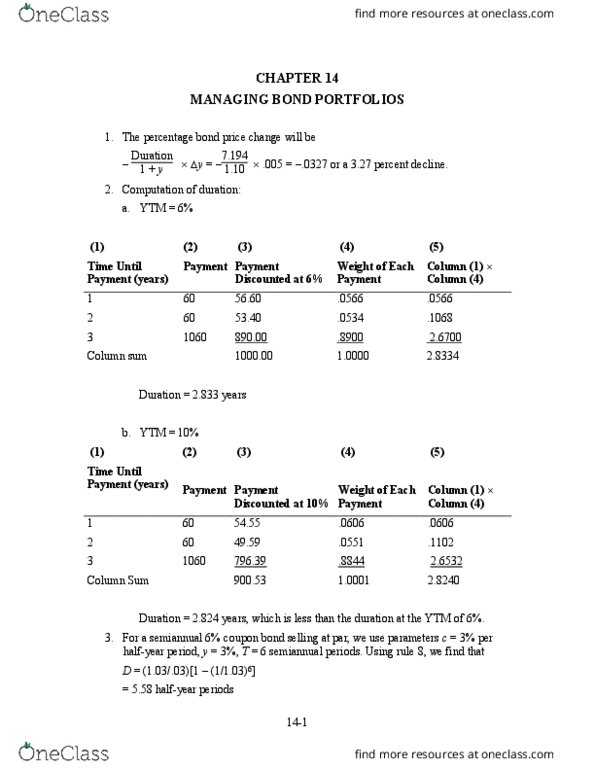

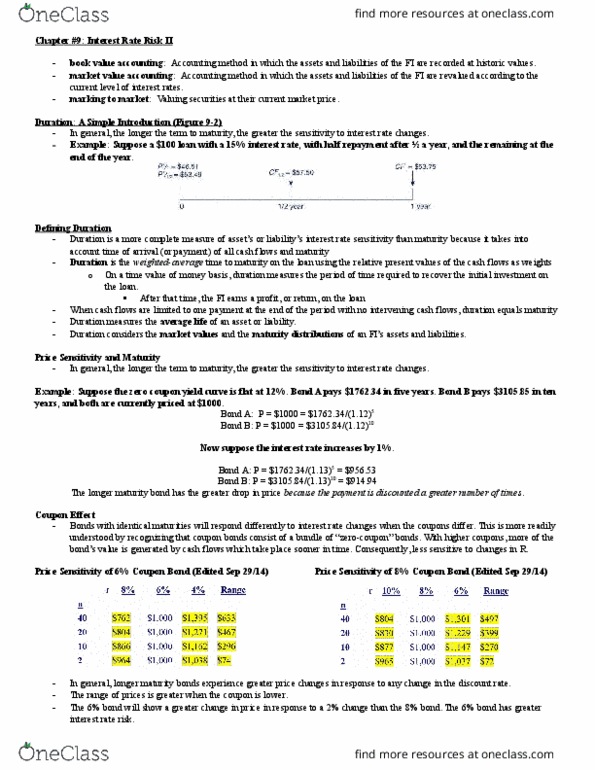

Calculate the duration and volatility of a 5-year, ,000 face value, 14 percent coupon bond yielding 15 percent with coupons paid annually. Using its duration and volatility, calculate what happens to the price of the bond when the yield to maturity falls to 14 percent. Volatility = v = -d/(1+r) = -3. 89427/1. 15 = -3. 416% When yield falls by one percent, price rises by 3. 416% or . 01. Without duration matching, say with duration of assets much longer than duration of liabilities, a financial institution"s net worth (assets less liabilities) will suffer when interest rates rise. The value of longer duration assets will fall much more than the value of shorter duration liabilities, with a resulting loss of net worth and possible insolvency. With canadian interest rates still at historical lows, mcgraw-hill-ryerson (mhr) is considering whether to take advantage of its lower cost of debt and refund its old bonds.