FINA 385 Lecture Notes - Lecture 12: Callable Bond, Investment, Sinking Fund

6 Dec 2016

School

Department

Course

Professor

Document Summary

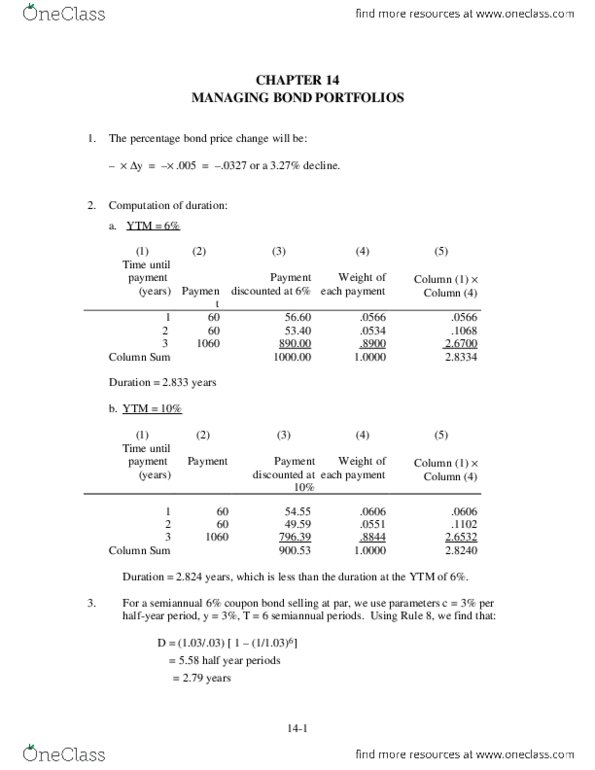

1. 10 . 005 = . 0327 or a 3. 27 percent decline. Computation of duration: ytm = 6% (1) (2) (3) (4) (5) Duration = 2. 833 years: ytm = 10% Duration = 2. 824 years, which is less than the duration at the ytm of 6%. For a semiannual 6% coupon bond selling at par, we use parameters c = 3% per half-year period, y = 3%, t = 6 semiannual periods. If the bond"s yield is 10 percent, use rule 7, setting the semiannual yield to 5 percent, and semiannual coupon to 3 percent: = 21 15. 448 = 5. 552 half-year periods = 2. 776 years. Bond b has a higher yield to maturity than bond a, since its coupon payments and maturity are equal to those of a while its price is lower. (perhaps the yield is higher because of differences in credit risk. )