BA 3301 Lecture 38: business-taxation-notes (dragged)

Document Summary

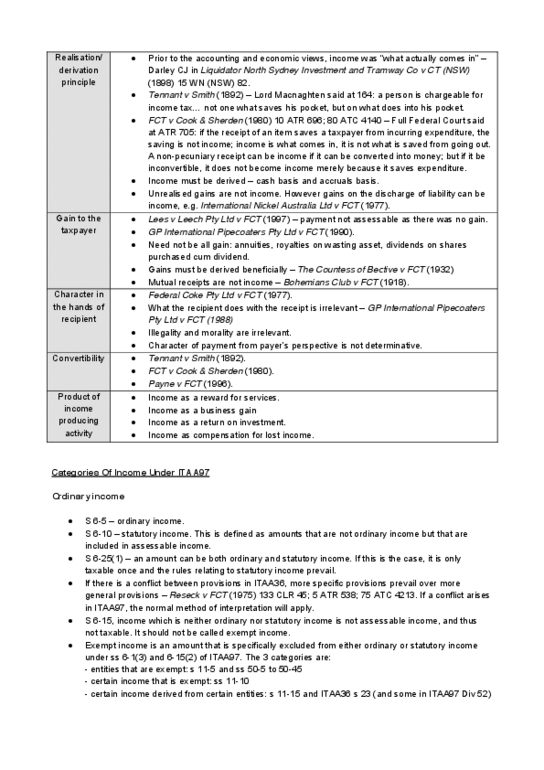

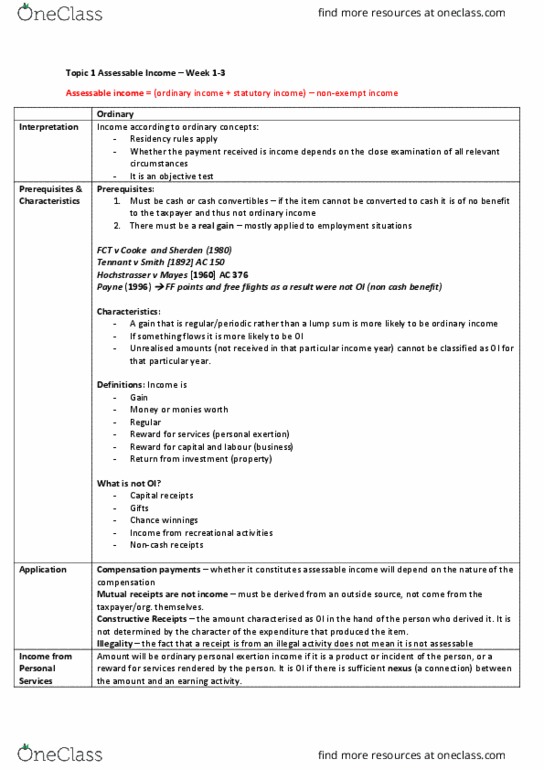

In federal coke the federal court held that: (a) (b) (c) (d) (e) The payment to federal coke was deductible to le nickle. The receipt by federal coke was a mere gift or windfall gain because there was no privity of contract between federal coke and le nickel. The receipt by federal coke was income because it would have been income if bellambi had received it. The receipt by federal coke was income to bellambi because it was constructively received by bellambi. If an amount is ordinary income to a recipient (a) It will never be foreign source income. (b) (c) (d) (e) It may also be included in the recipient"s assessable income via a statutory income provision but the rules about ordinary income will prevail. It may also be included in the recipient"s assessable income via a statutory income provision. It will always be assessable income even if it is exempt income.