MLC301 Lecture Notes - Lecture 2: Embezzlement, Gambling, Ordinary Income

Document Summary

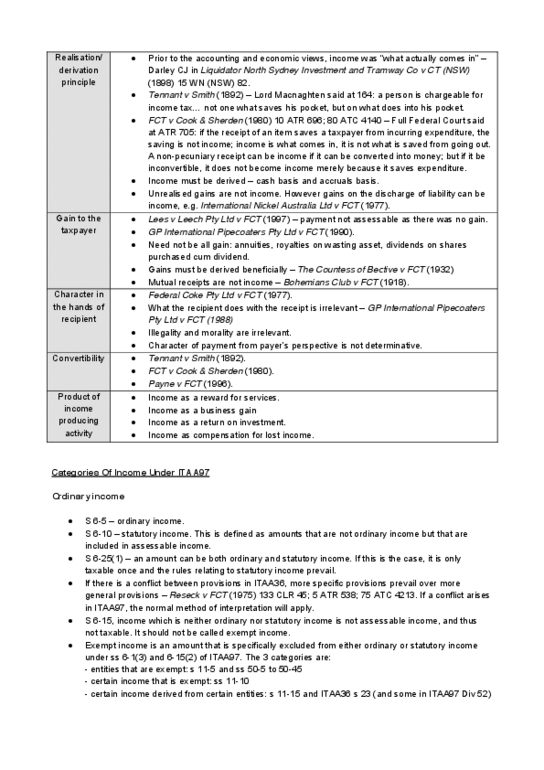

Assessable income = (ordinary income + statutory income) non-exempt income. Whether the payment received is income depends on the close examination of all relevant. Payne (1996) ff points and free flights as a result were not oi (non cash benefit) A gain that is regular/periodic rather than a lump sum is more likely to be ordinary income. Unrealised amounts (not received in that particular income year) cannot be classified as oi for. If something flows it is more likely to be oi that particular year. Compensation payments whether it constitutes assessable income will depend on the nature of the compensation. Mutual receipts are not income must be derived from an outside source, not come from the taxpayer/org. themselves. Constructive receipts the amount characterised as oi in the hand of the person who derived it. It is not determined by the character of the expenditure that produced the item.