ACCT 2301 Lecture 9: Notes Chapter 9

6 Nov 2018

Department

Course

Professor

Document Summary

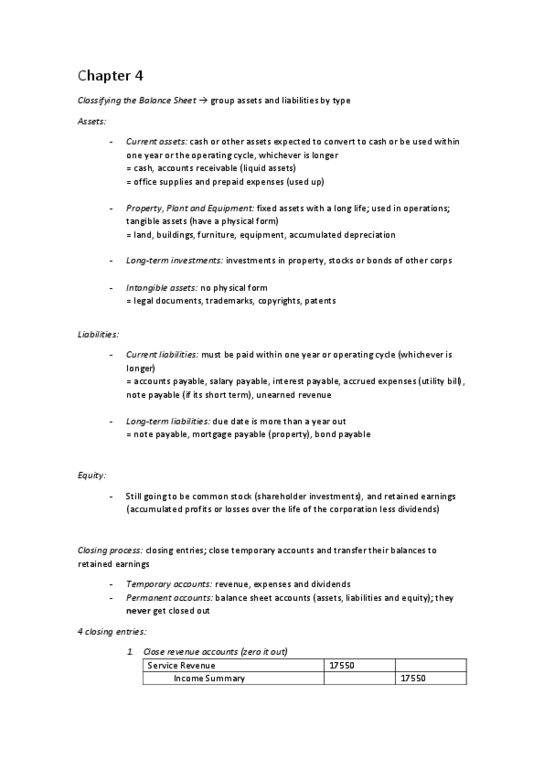

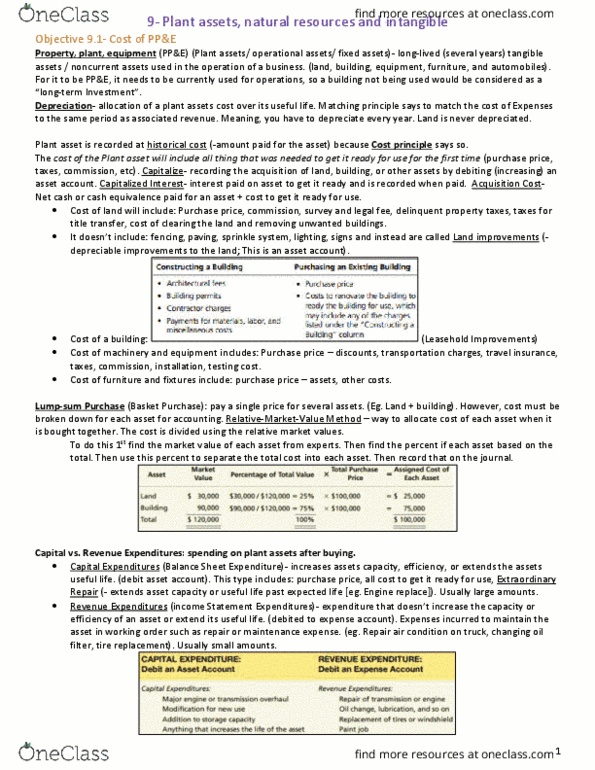

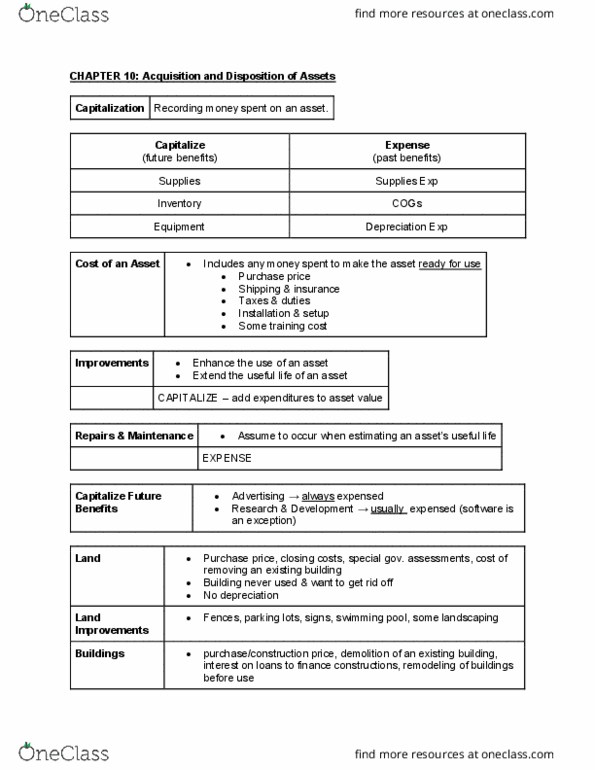

Land cost is anything paid to acquire land and get it ready for use. Anything added to land is recorded separately (land improvements) Cost is anything paid to purchase and get it ready for use. Cost it anything paid to purchase, transport and get it ready to use. Capitalize: recording the acquisition of a land, building or other assets by debiting (increasing) an asset account. Capital expenditure: repair that extends the fine of an asset; debit asset account. Revenue expenditure: does not extend life; repairs and maintenance expense. Basic journal entry: depreciation expense (income stat) Book value = cost accumulated depreciation. Over time, accumulated depreciation will increase and book value will decrease until it reaches residual value or zero. 3 basics methods to calculate depreciation: straight-line, units of production (of output, double declining balance. Example: truck; cost ,000; residual value ,000; 5 yrs. life; 100,000 miles: straight line depreciation: