ACCTG 211 Lecture 14: Chapter 20 Cost-Volume-Profit Analysis

Chapter 20 Cost-Volume-Profit Analysis

How Do Costs Behave When There Is a Change in Volume?

•Some costs change as the volume of sales increases or decreases. Other costs are

not affected by changes in volume.

•Different types of costs are:

•Variable costs

•Fixed costs

•Mixed costs

Variable Costs

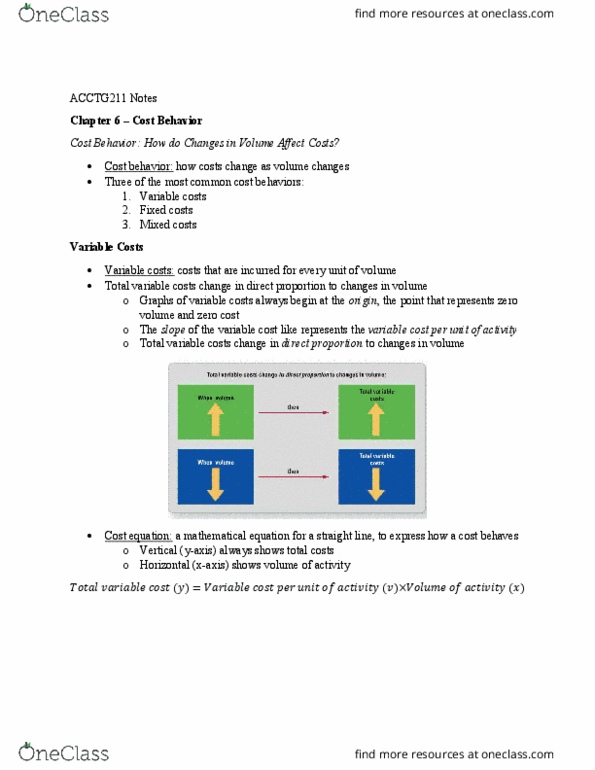

•Total costs that change in direct proportion to changes in productive output

•Unit-level activities: the cost is incurred each time a unit is produced or a service is

delivered

•Ex: DM, DL, operating supplies,!

•Total variable costs changes in proportional to volume changes

•Per unit variable cost remains unchanged

•Total variable cost = unit variable cost x units produced

Fixed Costs

•Total costs that remain constant within a relevant range of volume or activity

•fixed costs changes in a step-like manner when activity exceeds the relevant range

→ step costs

•Facility level activities

•Relevant range: the span of activity in which a company expects to operate

•Ex: rent, salaries

•Per unit fixed cost decreases as volume of activity increases (within relevant range)

•Total fixed cost = Fixed cost in relevant range

Estimating Cost Structure

•Estimating cost structure:!

•Estimate variable and fixed costs

•Use historical data

•Formulate a model to project future costs!

•The scatter diagram method:!

•The first step

•Use historical data and find a pattern

•Be aware of outliers from the analysis

High-Low Method

•A method to separate mixed costs into variable and fixed components is the high-low

method.

•Use three steps to separate the variable and fixed costs.!

•Step 1: Identify the highest and lowest levels of activity and calculate the variable

cost per unit.!

•Now that we have calculated the variable costs per unit, we can calculate the portion

of the mixed costs that relates to the fixed costs.!

•Step 2: Calculate the total fixed costs.

•Using the variable costs per unit and the fixed costs per unit, we can determine the

total mixed costs at various levels of productivity.!

•Step 3: Create and use an equation to show the behavior of a mixed cost.!

Document Summary

How do costs behave when there is a change in volume: some costs change as the volume of sales increases or decreases. Other costs are not affected by changes in volume: different types of costs are, variable costs, fixed costs, mixed costs. Fixed costs: total costs that remain constant within a relevant range of volume or activity, xed costs changes in a step-like manner when activity exceeds the relevant range. Contribution margin / unit contribution margin: the difference between net sales revenue and variable costs is the contribution margin, it is called contribution margin because it is the amount that contributes to covering. Xed costs: the contribution margin can be expressed as a unit amount, note: the terms unit contribution margin and contribution margin per unit are used interchangeably. Contribution margin ratio: a third way to express contribution margin is as a ratio, contribution margin ratio is the ratio of contribution margin to net sales revenue.