BUS 320 Lecture Notes - Lecture 5: Operating Leverage, Break Even, Fixed Cost

17 Nov 2017

School

Department

Course

Professor

Document Summary

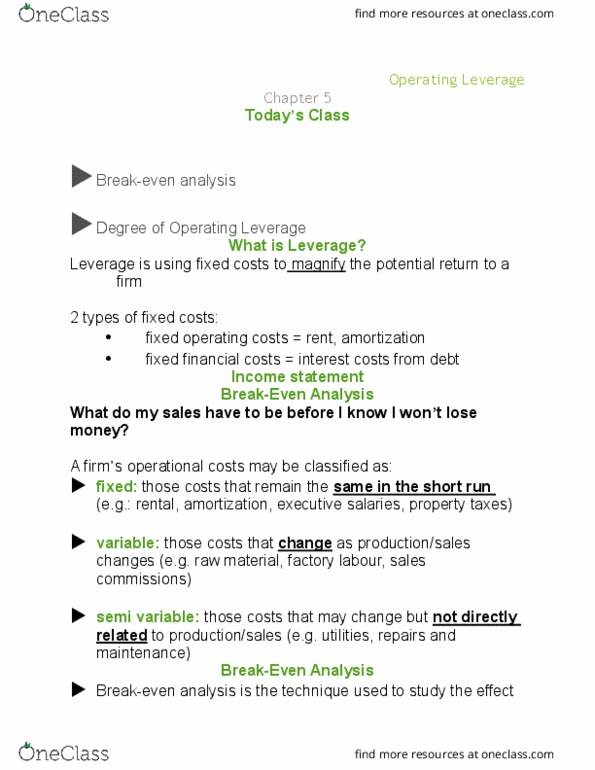

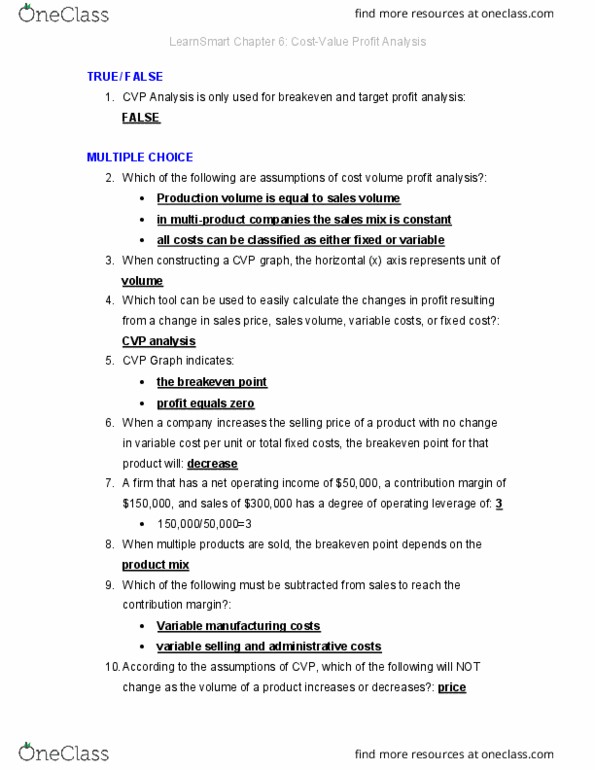

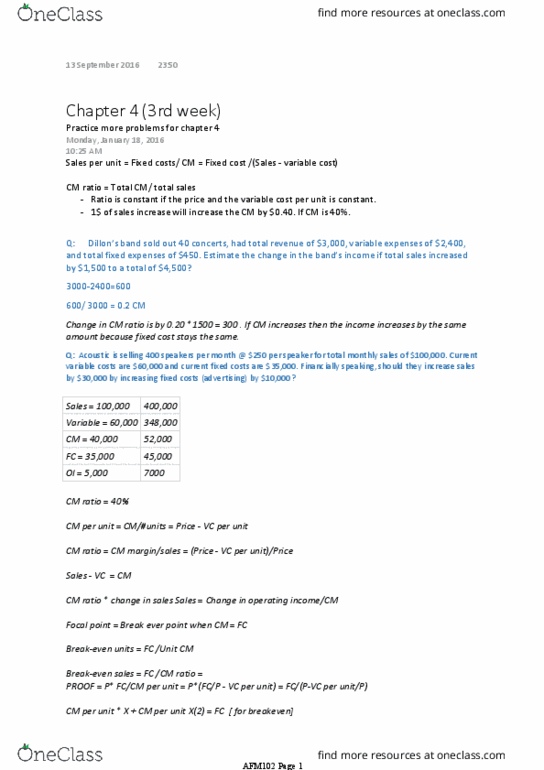

Use of fixed costs to magnify the level of profit or loss. Can produce beneficial results in favorable conditions. Can produce highly negative results in unfavorable conditions. Lessens opportunity for profit but reduces risk exposure. Interest must be paid, even when the firm loses money. Debt can increase the return on equity. Reduces potential profits but minimize risk exposure. Extent to which fixed assets and associated fixed costs are utilized in a business. The break-even point is at 50,000 units, where the total costs and total revenue lines intersect. Total variable fixed costs total costs total revenue operating income. Costs (tvc) (fc) (tc) (tr) (loss) (50,000 x sh. 80) (50,000 x ) Contribution margin price variable cost per unit p vc i. e. ,000 = ,000 = 50,000 units. The break-even point (be) can also be calculated by: Contribution margin price variable cost per unit p vc. Occurs as a result of a percentage change in units sold.