FINE 2000 Lecture Notes - Lecture 6: Investment, Tax Shield, Payback Period

14 Jun 2016

School

Department

Course

Professor

Document Summary

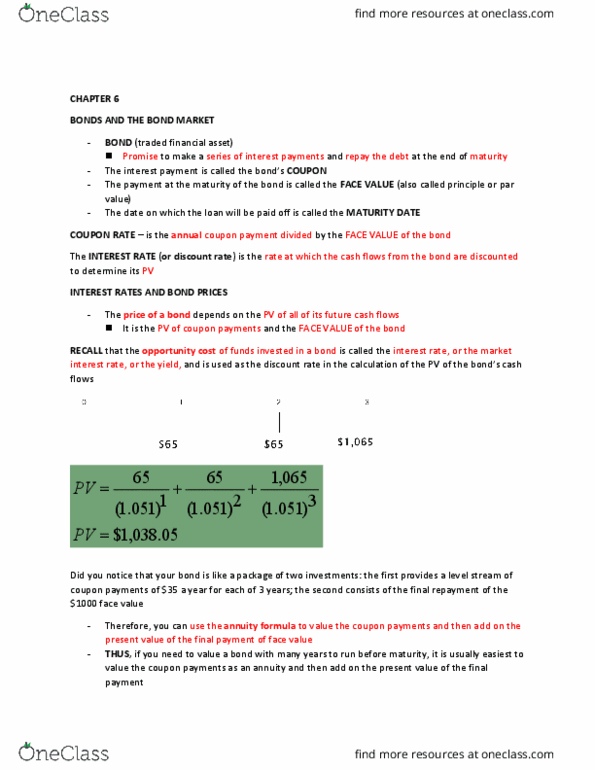

Brealey 5ce - solutions to suggested problems chapters 6-10. Note: unless otherwise stated, assume all bonds have ,000 face (par) value: a. The coupon payments are fixed at per year. Coupon rate = coupon payment/par value = 60/1000 = 6%, which remains unchanged: when the market yield increases, the bond price will fall. The cash flows are discounted at a higher rate. (cid:272). At a lo(cid:449)e(cid:396) p(cid:396)i(cid:272)e, the (cid:271)o(cid:374)d"s (cid:455)ield to (cid:373)atu(cid:396)it(cid:455) (cid:449)ill (cid:271)e highe(cid:396). The highe(cid:396) (cid:455)ield to (cid:373)atu(cid:396)it(cid:455) o(cid:374) the (cid:271)o(cid:374)d is commensurate with the higher yields available in the rest of the bond market: current yield = coupon payment/bond price. As coupon payment remains the same and the bond price decreases, the current yield increases: when the bond is selling at a discount, in this case, the yield to maturity is greater than 8%. We know that if the discount rate were 8%, the bond would sell at par.