FINE 2000 Lecture Notes - Lecture 6: Yield Curve, Premium Bond, Interest Rate Risk

Document Summary

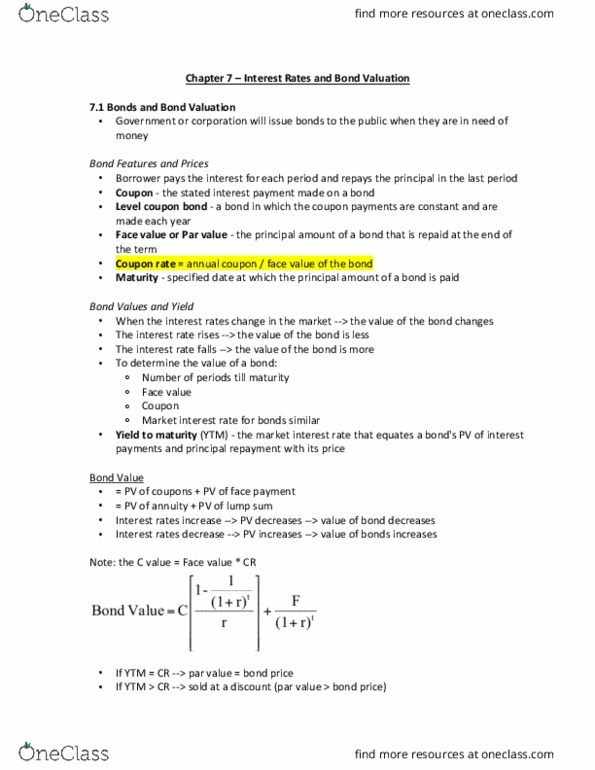

Promise to make a series of interest payments and repay the debt at the end of maturity. The i(cid:374)te(cid:396)est pay(cid:373)e(cid:374)t is (cid:272)alled the (cid:271)o(cid:374)d"s coupon. The payment at the maturity of the bond is called the face value (also called principle or par value) The date on which the loan will be paid off is called the maturity date. Coupon rate is the annual coupon payment divided by the face value of the bond. The interest rate (or discount rate) is the rate at which the cash flows from the bond are discounted to determine its pv. The price of a bond depends on the pv of all of its future cash flows. It is the pv of coupon payments and the face value of the bond. Therefore, you can use the annuity formula to value the coupon payments and then add on the present value of the final payment of face value.