Economics 1021A/B Lecture Notes - Lecture 3: Canada Pension Plan, Old Age Security, Life Annuity

22 Sep 2016

School

Department

Course

Professor

94

ECON 1021A/B Full Course Notes

Verified Note

94 documents

Document Summary

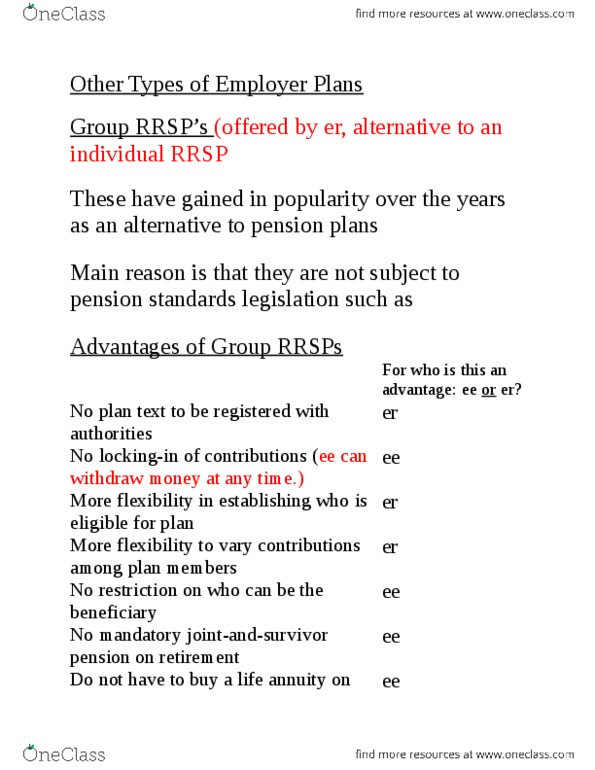

Have gained in popularity over the years as an alternative to pension plans: in some cases, an er will offer both; but mostly it is one or the other. Main reason is that they are not subject to pension standards legislation: No plan text to be registered with authorities. More flexibility in establishing who is eligible for plan. More flexibility to vary contributions among plan members. No restriction on who can be the beneficiary. They can buy any product in retirement that anyone with an rrsp can buy (life annuity; rrif; annuity certain) -> cash lump sum. Do not have to buy a life annuity on retirement. Disadvantage: er: er contributions are immediately vested, whereas for an rpp there is a maximum of 2 years for full vesting, ee: er contributions are considered salary to the ee, meaning any er contribution to the group. From the ee point of view, group rrsp"s have advantages over individual rrsps: