Actuarial Science 1021A/B Study Guide - Life Annuity, Collegehumor, Gust Co. Ltd.

16 Oct 2014

School

Department

Professor

Document Summary

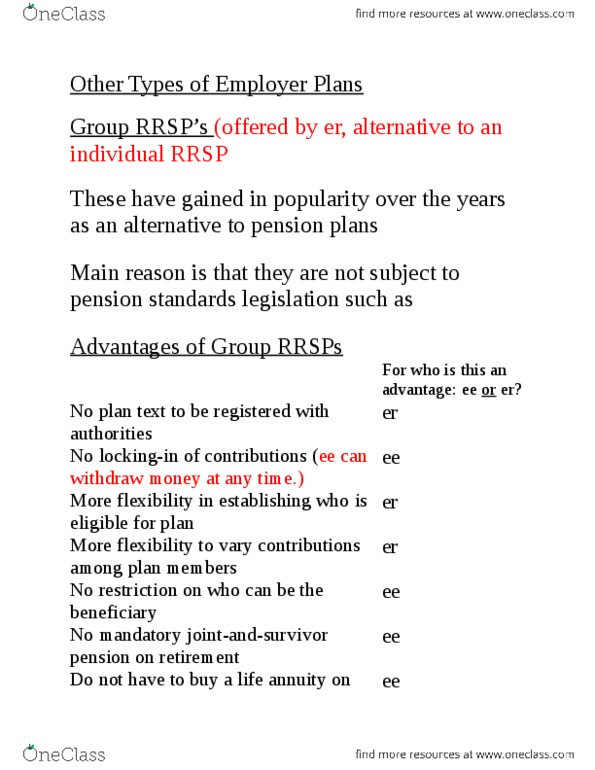

These have gained in popularity over the years as an alternative to pension plans. In some cases, an employer will offer both; but mostly it is one or the other. Main reason is that they are not subject to pension standards legislation such as: Employer: no plan to be registered with authorities (although they still have to be registered) Employee: no locking-in of contributions (employee can withdraw money at any time (taxed) Employer: more flexibility in establishing eligibility conditions (employer can be nice) Employer: more flexibility to vary employer contributions among plan members. Employee: no restriction on beneficiary designation (unlike rrsp) Employer: employer contributions are immediately vested (whereas for an rpp there is a maximum of 2 years for full vesting) Employee: employer contributions are considered salary to the employee. This means any employer contributions to the group rrsp must be added to the employee"s income after which it is subject to income tax.