ECO101H1 Lecture Notes - Lecture 14: Market Power, Perfect Competition, Demand Curve

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

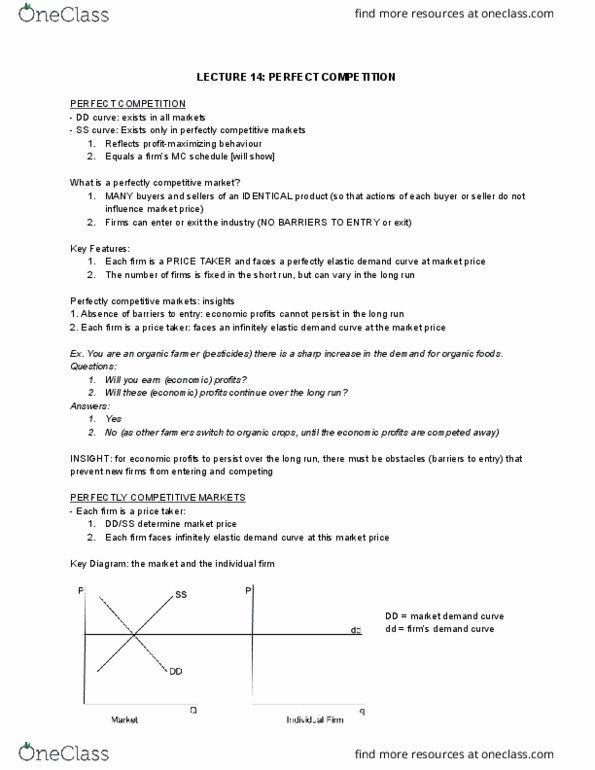

2) equals a firm"s mc schedule (will show) 1) many buyers and sellers of an identical product (so that actions of each buyer or seller do not influence market price: firms can enter or exit industry (no barriers to enter or exit) Key features: each firm is a price taker and faces a perfectly elastic demand curve at market price, the number of firms is fixed in the short run but can vary in the long run. 1) absence of barriers to entry: economic profits cannot persist in the long run. 2) each firm is a price taker: faces an infinitely elastic demand curve at market price. You are an organic farmer (no pesticides) There is a sharp increase in the demand for organic foods. Questions: will you earn (economic) profits, will these(economic) profits continue over the long run. Answers: yes, no (as other farmers switch to organic crops, until the economic profits are competed away)