COMM 353 Lecture Notes - Lecture 6: Income Statement, Total Absorption Costing, Earnings Management

Document Summary

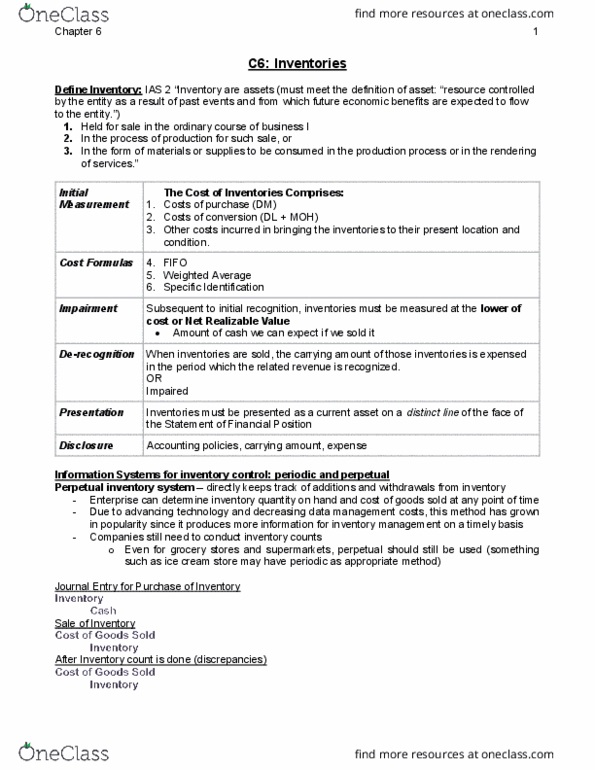

Definition: directly keep track of additions to and withdrawals from inventory. Can determine the inventory quantity on hand and cogs from the accounting records at any point in time. Produces more information for management of inventory on a timely basis. The company will still need to conduct an inventory count because the perpetual records may not correctly represent actual inventory quantities: periodic system. Definition: do not keep track of additions to and withdrawals from inventory. On the financial statement date, the enterprise conducts an inventory count to determine the ending inventory quantity and applies product costs to these quantities to determine the cost of ending inventory. With the value of beginning inventory and the amount purchased in the period to calculate cogs: comparison and illustration. Inventory at beginning of the year: ,000. Choose perpetual or periodic does not affect the ultimate result.