ECON101 Lecture Notes - Lecture 21: Average Variable Cost, Marginal Cost, Variable Cost

22 Oct 2018

School

Department

Course

Professor

ECON101 verified notes

21/41View all

Document Summary

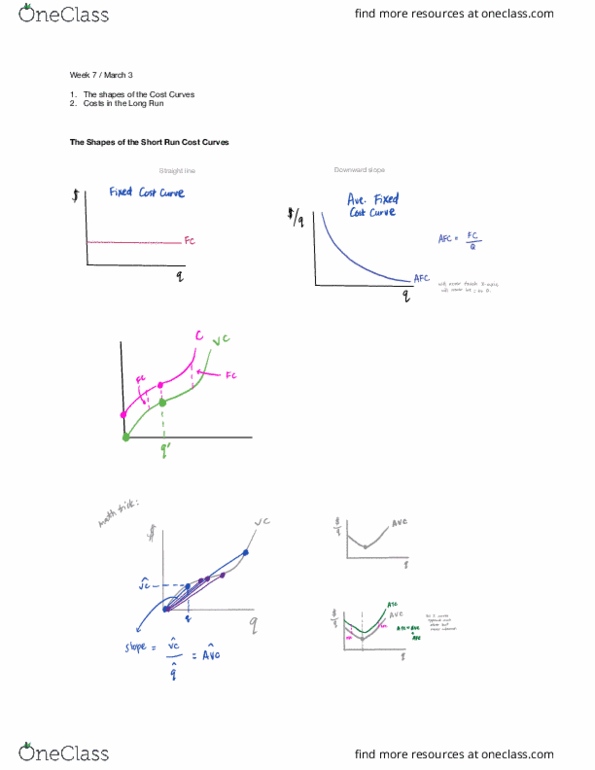

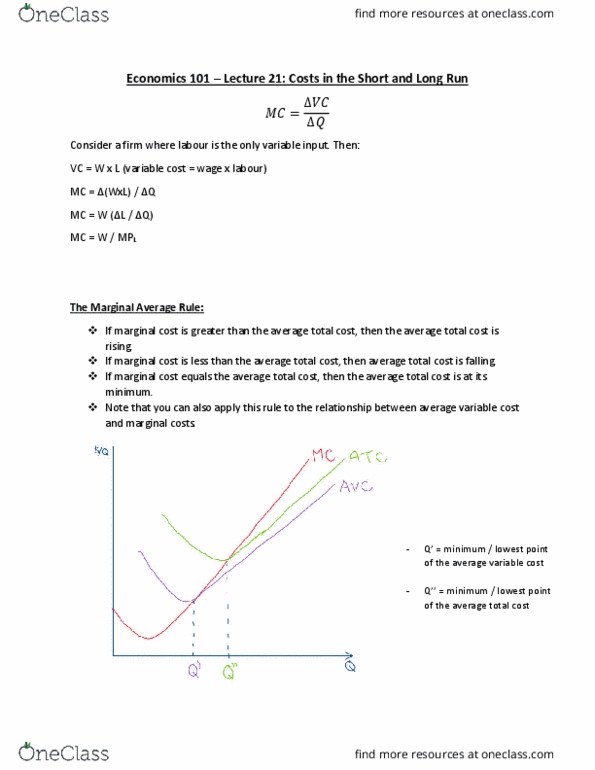

Economics 101 lecture 21: costs in the short and long run. Consider a firm where labour is the only variable input. Vc = w x l (variable cost = wage x labour) If marginal cost is greater than the average total cost, then the average total cost is rising. If marginal cost is less than the average total cost, then average total cost is falling. If marginal cost equals the average total cost, then the average total cost is at its minimum. Note that you can also apply this rule to the relationship between average variable cost and marginal costs. Q" = (cid:373)i(cid:374)i(cid:373)u(cid:373) / lowest poi(cid:374)t of the average variable cost. Q"" = (cid:373)i(cid:374)i(cid:373)u(cid:373) / lowest poi(cid:374)t of the average total cost. All costs are variable: there is no difference between average total cost (avc) and average total cost (atc) because there is no fixed costs therefore avc and atc are the same.