ACC 406 Lecture Notes - Lecture 3: Activity-Based Costing

Document Summary

Get access

Related Documents

Related Questions

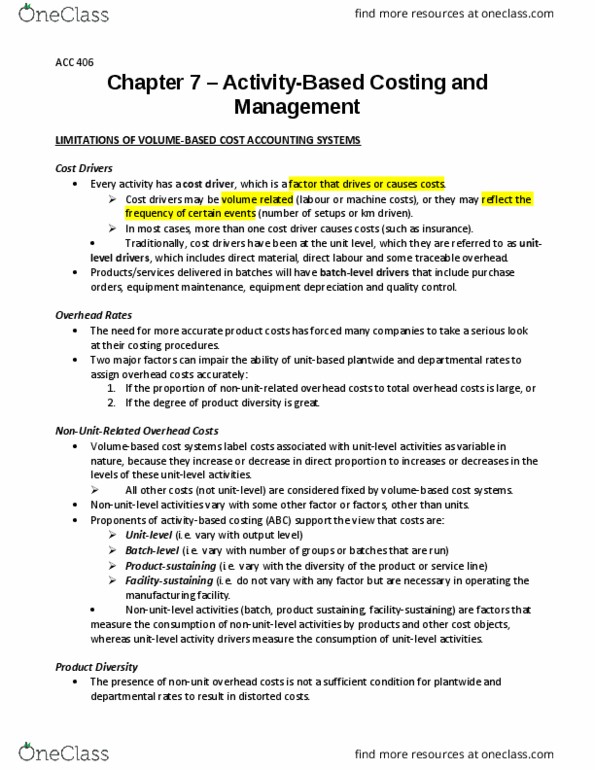

Citra bhd manufacturers two types of components, C1 and C2 andabsorbs overheads on the basis of direct labour hours. Anticipatedoverheads for the upcoming accounting period is RM 972500,information about the company products is as follows

C1 | C2 | |

Expected production volume (units) | 3000 | 12000 |

Diect material costs | RM 32 PER UNIT | RM 40 PER UNIT |

Direct labour /unit (rm 15/hour) | RM 30 | RM 60 |

The overheads od citra bhd of RM 972500 can be identified withthree main activities as follows

Order processing | Rm 180000 |

Machine processing | Rm 650000 |

Product inspection | Rm 142500 |

These activities are driven by number of orders processed ,machine hours worked and insoection hours respectively. Datarelevant to these activities are as follows

C1 | C2 | |

Order processed | 380 | 220 |

Machine hours worked | 22000 | 28000 |

Inspection hours | 3000 | 12000 |

Q1A â Assuming the use of direct labour hours to apply overheadsto production, compute the unit manufacturing costs of products C1and C2 if the expected manufacturing volume is attained

Q1B - compute the absorption rates that would be used for orderprocessing, machine processing and product inspection

Q1C â assuming the use of activity based costing compute theunit manufacturing costs of products C1 and C2 if the expectedmanufacturing volume is attained

Q1D â comparing the unit product costs calculated under the twocosts calculated under the two costing systems state which productis overcost and which product is undercost, and how much?Additionally calculate the amount of the cost distortion for eachproduct.

Looking to achieve the highest grade possible, please see below. Please indicate if this answer is correct. IF I have left a calcuation out, please include.

Thank you,

| The Big Bus Company manufactures two products, Product 1 and Product 2. Product 2 was developed as an attempt to enter a market closely related to that of Product 1. Product 2 is the more complex of the two products, requiring three hours of direct labour time per unit to manufacture compared to one and one-half hours of direct labour time for Product 1. Product 2 is produced on an automated production line. Overhead is currently assigned to the products on the basis of direct labour-hours. The company estimated it would incur a total of $396,000 in manufacturing overhead costs and produce 5,500 units of Product 2 and 22,000 units of Product 1 during the current year. Unit costs for materials and direct labour are: | ||||||||||||

| Product 1 | Product 2 | |||||||||||

| Direct Labour | $7 | $15 | ||||||||||

| Direct material | $9 | $20 | ||||||||||

| Required: | ||||||||||||

| a. Compute the predetermined overhead rate under the current method of allocation and determine the unit product cost of each product for the current year. (5 marks) | ||||||||||||

| Product 1 | Product 2 | Total | Allocation | |||||||||

| Direct Labour hour / unit | 1.5 | 3 | 396,000 / 49,500 | |||||||||

| units produced | 22,000 | 5,500 | 8 | |||||||||

| total labour hour | 33,000 | 16,500 | 49,500 | |||||||||

| overhead/unit | 12 | 24 | overhead/unit is calculated by direct LH x 8 | |||||||||

| Product 1 | Product 2 | |||||||||||

| Direct material | 9 | 20 | ||||||||||

| Direct labour | 7 | 15 | ||||||||||

| overhead/unit | 16 | 35 | ||||||||||

| cost/unit | 32 | 70 | ||||||||||

| b. The company's overhead costs can be attributed to four major activities. These activities and the amount of overhead cost attributable to each for the current year are given below: (5 marks) | ||||||||||||

| Expected Activity | ||||||||||||

| Activity Costs Pools | Estimated Overhead Costs | Product 1 | Product 2 | Total | ||||||||

| Machine set-ups required | $170,000 | 700 | 1,000 | 1,700 | ||||||||

| Purchase orders issued | 37,000 | 300 | 200 | 500 | ||||||||

| Machine-hours required | 91,000 | 4,000 | 9,000 | 13,000 | ||||||||

| Maintenance requests issued | 98,000 | 400 | 600 | 1,000 | ||||||||

| $396,000 | ||||||||||||

| Using the data above and an activity-based costing approach, determine the unit product cost of each product for the current year. | ||||||||||||

| Total Cost | Product A | Product B | ||||||||||

| Machine Setups | 170,000 | 70,000 | 100,000 | |||||||||

| purchase order | 37,000 | 22,200 | 14,800 | |||||||||

| machine hours | 91,000 | 28,000 | 63,000 | |||||||||

| maintenance requests | 98,000 | 39,200 | 58,800 | |||||||||

| Total | 396,000 | 159,400 | 236,600 | |||||||||

| 22,000 | 5,500 | |||||||||||

| overhead /cost | 7..25 | 43..02 | ||||||||||

| product 1 | product 2 | |||||||||||

| Direct Labour | 9 | 20 | ||||||||||

| direct material | 7 | 15 | ||||||||||

| overhead / unit | 7..25 | 43.02. | ||||||||||

| Unit/ cost | 23..25 | 78.020. | ||||||||||