ACTG 1P91 Lecture 5: Internal Control and Cash

30 Oct 2018

School

Department

Course

Professor

ACTG 1P91 verified notes

5/26View all

Internal Control and Cash

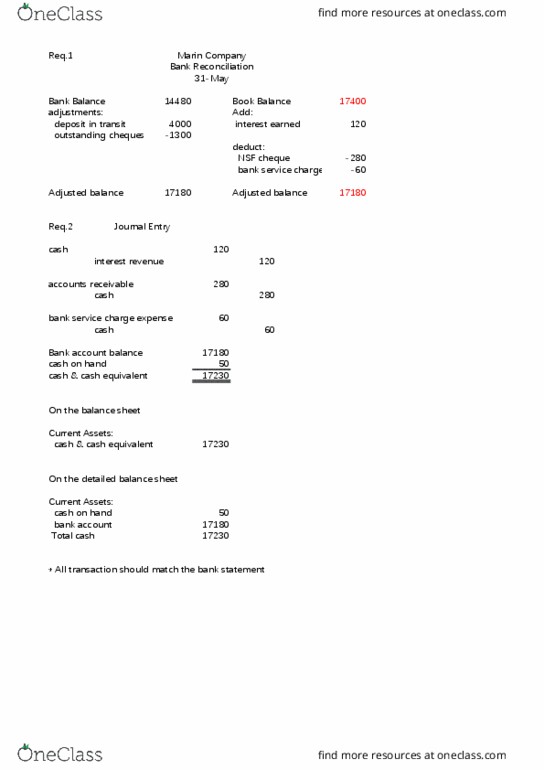

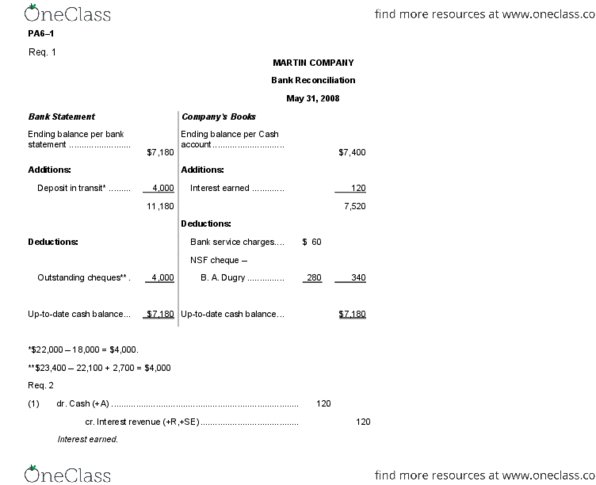

● Bank reconciliation: a process of matching a company’s cash records to the cash

balance on a bank statement. This is a good internal control over cash.

● Internal Control: it is a process designed to help an organization achieve reliable

financial reporting, effective and efficient operations, and compliance w/relevant laws

and regulations.

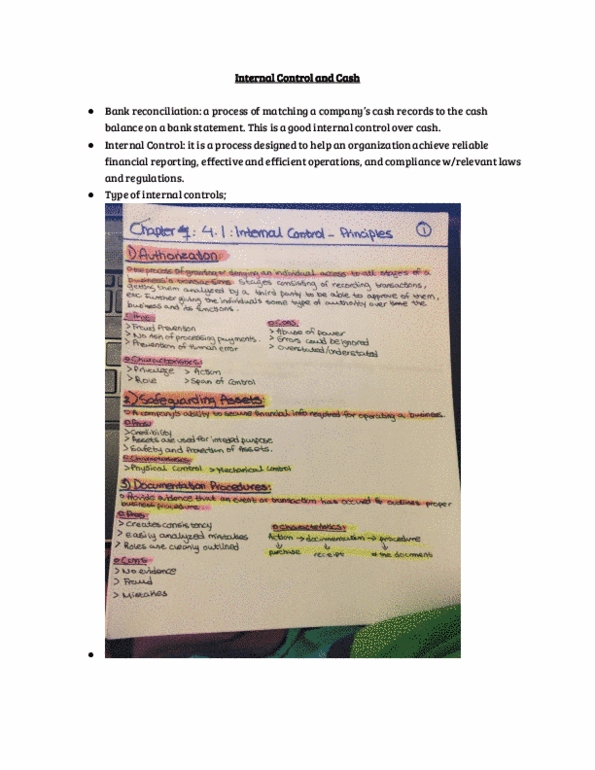

● Type of internal controls;

●

●

● Limitations of internal control: human errors, resource limitation, cost effectiveness.

Checking out check:

● Party who issues checks:

- Issue date not same as clearance date

- Cash balance goes down on issue date (credit cash) but bank balance will go

down on clearance date.

● Outstanding checks:

Document Summary

Bank reconciliation: a process of matching a company"s cash records to the cash balance on a bank statement. This is a good internal control over cash. Internal control: it is a process designed to help an organization achieve reliable financial reporting, effective and efficient operations, and compliance w/relevant laws and regulations. Limitations of internal control: human errors, resource limitation, cost effectiveness. Cash balance goes down on issue date (credit cash) but bank balance will go down on clearance date. Checks that are issued but not yet cleared as of bank statement date. When there are outstanding checks, book cash balance is lower than bank balance at the bank statement date. Cash balance goes up on the day checks are received but bank balance will go up once checks are deposited. Mostly the same day but possibly next day or later days.