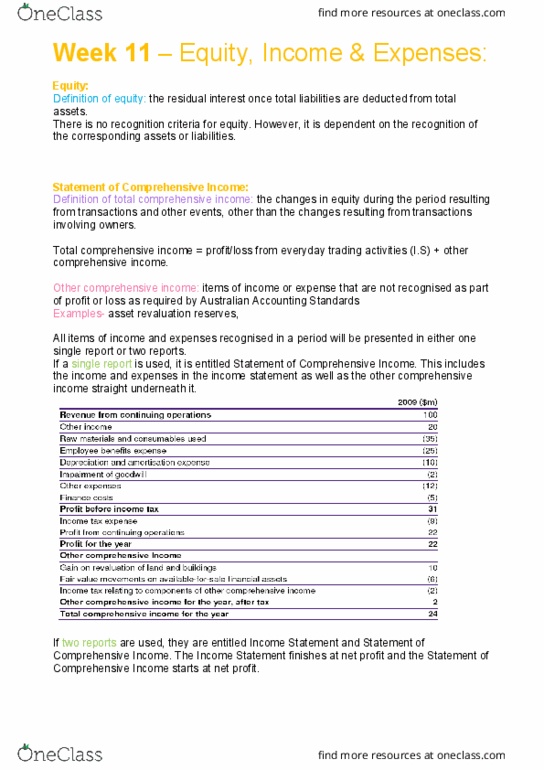

ACC1100 Lecture Notes - Lecture 11: Retained Earnings, Share Capital, Income Statement

Document Summary

Get access

Related Documents

Related Questions

QUESTION 1 30 MARKS

The following information represents the abridged financial statements of Mega Ltd and its subsidiary Ultra Ltd:

| Statement of financial position as at 31 December 2018 | ||||||

| Mega Ltd | Ultra Ltd | |||||

| ASSETS | ||||||

| Property, plant and equipment | 270 000 | 340 000 | ||||

| Investment in Ultra Ltd: 48 000 shares at fair value | 350 000 | - | ||||

| (cost: N$ 330 000) | ||||||

| Trade receivables | 80 000 | 23 500 | ||||

| Inventories | 350 000 | 218 000 | ||||

| Bank | 65 000 | - | ||||

| Total assets | 1 115 000 | 581 500 | ||||

| EQUITY AND LIABILITIES | ||||||

| Share capital | 400 000 | 240 000 | ||||

| Mark-to-market reserve | 20 000 | 10 000 | ||||

| Retained earnings | 375 000 | 240 000 | ||||

| Long-term borrowings | 43 000 | 21 000 | ||||

| Trade and other payables | 277 000 | 23 500 | ||||

| Bank overdraft | - | 47 000 | ||||

| Total equity and liabilities | 1 115 000 | 581 500 | ||||

| Statement of profit or loss and other comprehensive income for the year ended | ||||||

| 31 December 2018 | ||||||

| Mega Ltd | Ultra Ltd | |||||

| Revenue | 927 000 | 1 628 000 | ||||

| Cost of sales | -472 000 | -725 000 | ||||

| Gross profit | 455 000 | 903 000 | ||||

| Other expenses | -287 100 | -472 000 | ||||

| Dividend received from Ultra Ltd | 94 000 | - | ||||

| Profit before tax | 261 900 | 431 000 | ||||

| Income tax expense | -198 000 | -128 000 | ||||

| Profit for the year | 63 900 | 303 000 | ||||

| Other comprehensive income | ||||||

| Items that will not be reclassified to profit or loss | ||||||

| Mark-to-market reserve | 4 000 | 1 000 | ||||

| TOTAL COMPREHENSIVE INCOME FOR THE YEAR | 67 900 | 304 000 | ||||

| Extract from the Statement of changes in equity for the year ended 31 December 2018 | ||||

| Mark-to-market reserve | Retained earnings | |||

| Mega Ltd | Ultra Ltd | Mega Ltd | Ultra Ltd | |

| Balance at 1 Jan 2018 | 15 000 | 8 000 | 215 000 | 170 000 |

| Changes in equity for 2018 | ||||

| Total comprehensive income for the year: | ||||

| Profit for the year | 63 900 | 303 000 | ||

| Other comprehensive income for the year | 4 000 | 1 000 | ||

| Dividends | -108 000 | -120 000 | ||

| Balance at 31 December 2018 | 19 000 | 9 000 | 170 900 | 353 000 |

Additional information:

On 1 January 2018, the date on which Ultra Ltd acquired the interest in Mega Ltd, the equity of Mega Ltd consisted of:

Share capital N$ 260 000

Mark-to-market reserve N$ 3 000

Revaluation reserve N$ 7 000

Retained earnings N$ 135 000

Ultra Ltd elected to measure non-controlling interests at fair value at the acquisition date. On 1 January 2018, the fair value of each non-controlling interestâs share was N$8,50 per share, based on market prices.

Ultra Ltd classified the investment in Ultra Ltd under IFRS 9 in its separate financial statements and recognised fair value adjustments in a mark-to-market reserve (other comprehensive income). Ignore tax implications.

REQUIRED

Prepare consolidated financial statements for the Mega Ltd Group for the reporting period ended 31 December 2018. (30 marks