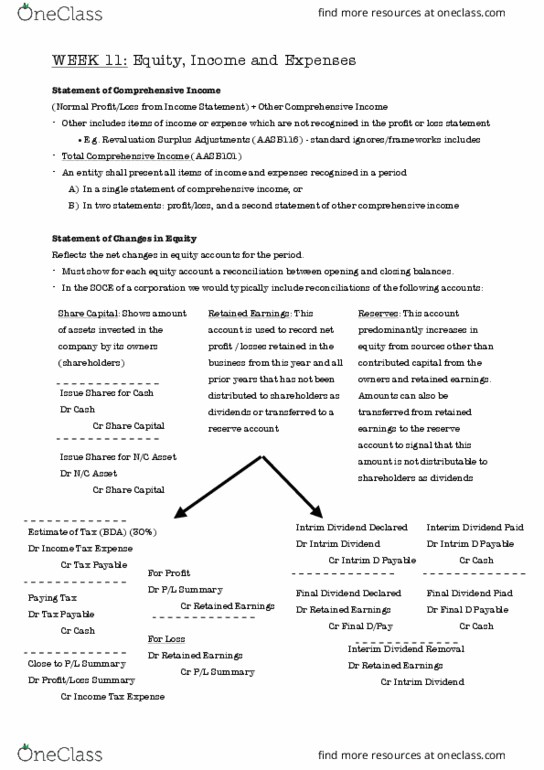

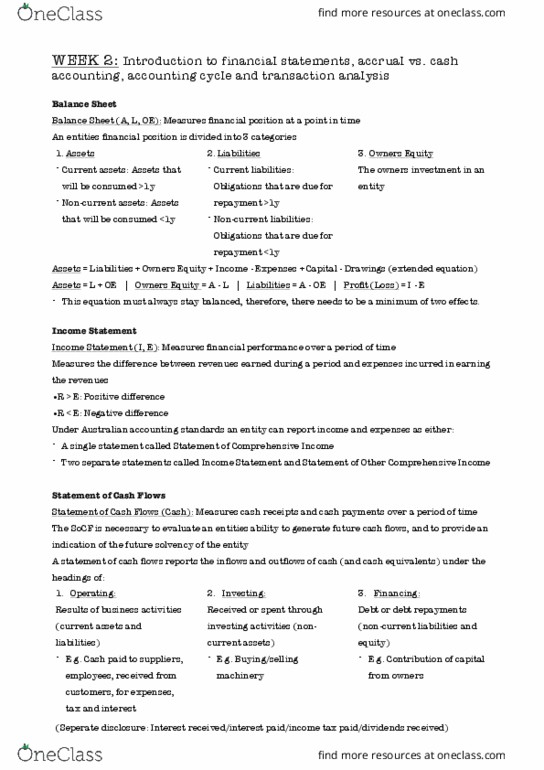

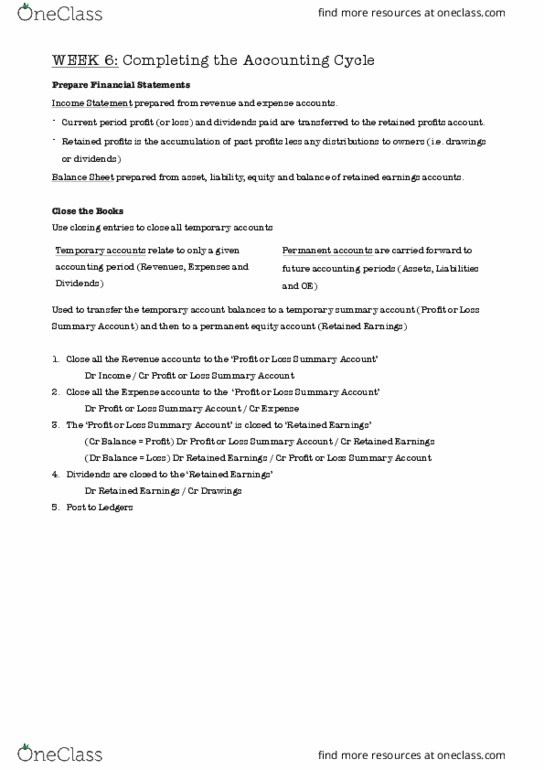

ACC1100 Lecture Notes - Lecture 11: Comprehensive Income, Retained Earnings, Share Capital

Document Summary

Get access

Related Documents

Related Questions

QUESTION 1 30 MARKS

The following information represents the abridged financial statements of Mega Ltd and its subsidiary Ultra Ltd:

| Statement of financial position as at 31 December 2018 | ||||||

| Mega Ltd | Ultra Ltd | |||||

| ASSETS | ||||||

| Property, plant and equipment | 270 000 | 340 000 | ||||

| Investment in Ultra Ltd: 48 000 shares at fair value | 350 000 | - | ||||

| (cost: N$ 330 000) | ||||||

| Trade receivables | 80 000 | 23 500 | ||||

| Inventories | 350 000 | 218 000 | ||||

| Bank | 65 000 | - | ||||

| Total assets | 1 115 000 | 581 500 | ||||

| EQUITY AND LIABILITIES | ||||||

| Share capital | 400 000 | 240 000 | ||||

| Mark-to-market reserve | 20 000 | 10 000 | ||||

| Retained earnings | 375 000 | 240 000 | ||||

| Long-term borrowings | 43 000 | 21 000 | ||||

| Trade and other payables | 277 000 | 23 500 | ||||

| Bank overdraft | - | 47 000 | ||||

| Total equity and liabilities | 1 115 000 | 581 500 | ||||

| Statement of profit or loss and other comprehensive income for the year ended | ||||||

| 31 December 2018 | ||||||

| Mega Ltd | Ultra Ltd | |||||

| Revenue | 927 000 | 1 628 000 | ||||

| Cost of sales | -472 000 | -725 000 | ||||

| Gross profit | 455 000 | 903 000 | ||||

| Other expenses | -287 100 | -472 000 | ||||

| Dividend received from Ultra Ltd | 94 000 | - | ||||

| Profit before tax | 261 900 | 431 000 | ||||

| Income tax expense | -198 000 | -128 000 | ||||

| Profit for the year | 63 900 | 303 000 | ||||

| Other comprehensive income | ||||||

| Items that will not be reclassified to profit or loss | ||||||

| Mark-to-market reserve | 4 000 | 1 000 | ||||

| TOTAL COMPREHENSIVE INCOME FOR THE YEAR | 67 900 | 304 000 | ||||

| Extract from the Statement of changes in equity for the year ended 31 December 2018 | ||||

| Mark-to-market reserve | Retained earnings | |||

| Mega Ltd | Ultra Ltd | Mega Ltd | Ultra Ltd | |

| Balance at 1 Jan 2018 | 15 000 | 8 000 | 215 000 | 170 000 |

| Changes in equity for 2018 | ||||

| Total comprehensive income for the year: | ||||

| Profit for the year | 63 900 | 303 000 | ||

| Other comprehensive income for the year | 4 000 | 1 000 | ||

| Dividends | -108 000 | -120 000 | ||

| Balance at 31 December 2018 | 19 000 | 9 000 | 170 900 | 353 000 |

Additional information:

On 1 January 2018, the date on which Ultra Ltd acquired the interest in Mega Ltd, the equity of Mega Ltd consisted of:

Share capital N$ 260 000

Mark-to-market reserve N$ 3 000

Revaluation reserve N$ 7 000

Retained earnings N$ 135 000

Ultra Ltd elected to measure non-controlling interests at fair value at the acquisition date. On 1 January 2018, the fair value of each non-controlling interestâs share was N$8,50 per share, based on market prices.

Ultra Ltd classified the investment in Ultra Ltd under IFRS 9 in its separate financial statements and recognised fair value adjustments in a mark-to-market reserve (other comprehensive income). Ignore tax implications.

REQUIRED

Prepare consolidated financial statements for the Mega Ltd Group for the reporting period ended 31 December 2018. (30 marks

Using the information below, discuss both the positive andnegative trends presented in the company

Suncor Energy Inc.

Income Statement Horizontal Analysis

For the years ending December X, 2012

And December X, 2013 ($ millions)

2013 | 2012 | Amount | Variance % Change 2013 from 2012 | |

Revenues and Other Income | ||||

Operating revenues, net of royalties | 39,593 | 38,107 | ||

Other Income | 704 | 419 | ||

40,297 | 38,526 | 1,771 | 4.60 | |

Expenses | ||||

Purchases of crude oil and products | 17,293 | 17,047 | ||

Operating, selling and general | 9,447 | 8,897 | ||

Transportation | 845 | 685 | ||

Depreciation, depletion, amortization and impairment | 4,892 | 6,446 | ||

Exploration | 332 | 309 | ||

Gain on disposal of assets | (137) | (44) | ||

Project start-up costs | 15 | 60 | ||

Voyageur upgrader project charges | 82 | - | ||

Financing expenses | 1,162 | 142 | ||

33,921 | 33,542 | |||

Earnings before Income Taxes | 6,376 | 4,984 | 1,392 | 27,93 |

Income Taxes | ||||

Current | 2,083 | 1,515 | ||

Deferred | 382 | 729 | ||

2,465 | 2,244 | |||

Net earnings | 3,911 | 2,740 | 1,171 | 42,74 |

Other Comprehensive Income (loss) | ||||

Items that may be subsequently reclassified to Profit orLoss: | ||||

| Foreign currency translation adjustment | 325 | (16) | ||

| Cash flow hedges reclassified to net earning | - | (1) | ||

| Items That will not be reclassified to profit or loss: | ||||

| Actuarial gain (loss) on employee retirement benefit plans, net of income taxes. | 579 | (134) | ||

Other comprehensive Income (loss) | 904 | (151) | ||

Total Comprehensive Income | 4,815 | 2,589 | 2,226 | 85.98 |

Per Common share | ||||

Net earnings-basic | 2.61 | 1.77 | ||

Net earning-diluted | 2.60 | 1.76 | ||

Cash dividends | 0.73 | 0.50 |

Suncor Energy Inc.

Balance Sheet Horizontal Analysis

For the years ending December X, 2012

And December X, 2013

2013 | 2012 | Amount | Variance % Change 2013 from 2012 | |

Assets | ||||

Current assets | ||||

Cash and cash equivalents | 5,202 | 4,385 | ||

Accounts receivable | 5,254 | 5,201 | ||

Inventories | 3,944 | 3,697 | ||

Income taxes receivable | 294 | 799 | ||

Total current assets | 14,694 | 14,082 | ||

Property, plant and equipment, net | 57,270 | 55,434 | ||

Exploration and evaluation | 2,772 | 3,284 | ||

Other assets | 422 | 419 | ||

Goodwill & other intangible assets | 3,092 | 3,104 | ||

Deferred income taxes | 65 | 78 | ||

Total assets | 78,315 | 76,401 | 1,914 | 2.50 |

Liabilities and Shareholdersâ Equity | ||||

Current liabilities | ||||

Short-term debt | 798 | 775 | ||

Current portion of long-term debt | 457 | 311 | ||

| Accounts payable and accrued liabilities | 7,090 | 6,446 | ||

Current portion of provisions | 998 | 856 | ||

Income taxes payable | 1,263 | 1,165 | ||

Total current liabilities | 10,606 | 9,553 | ||

Long-term debt | 10,203 | 9,938 | ||

Other long-term liabilities | 1,464 | 2,319 | ||

Provisions | 4,078 | 4,932 | ||

Deferred income taxes | 10,784 | 10,444 | ||

Total liabilities | 37,135 | 37,186 | -51 | -0.14 |

Stockholderâs equity | 41,180 | 39,215 | 1,965 | 5.01 |

Total liabilities and equity | 78,315 | 76,401 | 1,915 | 2.50 See More from Todd Young |